Question: Treasury Bill Quote: a. Compute the price (as a % of par) that an investor must pay for this T-Bill. b. What is the yield

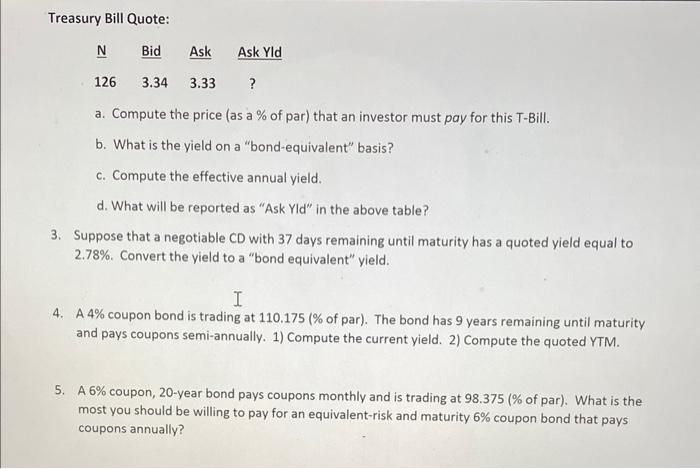

Treasury Bill Quote: a. Compute the price (as a % of par) that an investor must pay for this T-Bill. b. What is the yield on a "bond-equivalent" basis? c. Compute the effective annual yield. d. What will be reported as "Ask YId" in the above table? 3. Suppose that a negotiable CD with 37 days remaining until maturity has a quoted yield equal to 2.78%. Convert the yield to a "bond equivalent" yield. 4. A 4% coupon bond is trading at 110.175 (\% of par). The bond has 9 years remaining until maturity and pays coupons semi-annually. 1) Compute the current yield. 2) Compute the quoted YTM. 5. A 6% coupon, 20-year bond pays coupons monthly and is trading at 98.375 (\% of par). What is the most you should be willing to pay for an equivalent-risk and maturity 6% coupon bond that pays coupons annually? Treasury Bill Quote: a. Compute the price (as a % of par) that an investor must pay for this T-Bill. b. What is the yield on a "bond-equivalent" basis? c. Compute the effective annual yield. d. What will be reported as "Ask YId" in the above table? 3. Suppose that a negotiable CD with 37 days remaining until maturity has a quoted yield equal to 2.78%. Convert the yield to a "bond equivalent" yield. 4. A 4% coupon bond is trading at 110.175 (\% of par). The bond has 9 years remaining until maturity and pays coupons semi-annually. 1) Compute the current yield. 2) Compute the quoted YTM. 5. A 6% coupon, 20-year bond pays coupons monthly and is trading at 98.375 (\% of par). What is the most you should be willing to pay for an equivalent-risk and maturity 6% coupon bond that pays coupons annually

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts