Question: Treasury zero rates for various maturities are given below (with semiannual compounding): What is the 6-month forward rate (with continuous compounding) from 1.5 to 2

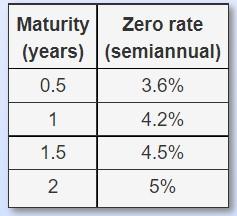

Treasury zero rates for various maturities are given below (with semiannual compounding):

What is the 6-month forward rate (with continuous compounding) from 1.5 to 2 years?

What is the 6-month forward rate (with semiannual compounding) from 1.5 to 2 years?

What is the value of an FRA with a principal of $110 million where the holder receives LIBOR and pays 4.3% (semiannually compounded) for a six-month period beginning in 1.5 years (in $ million)?

\begin{tabular}{|c|c|} \hline Maturity (years) & Zero rate (semiannual) \\ \hline 0.5 & 3.6% \\ \hline 1 & 4.2% \\ \hline 1.5 & 4.5% \\ \hline 2 & 5% \\ \hline \end{tabular}

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock