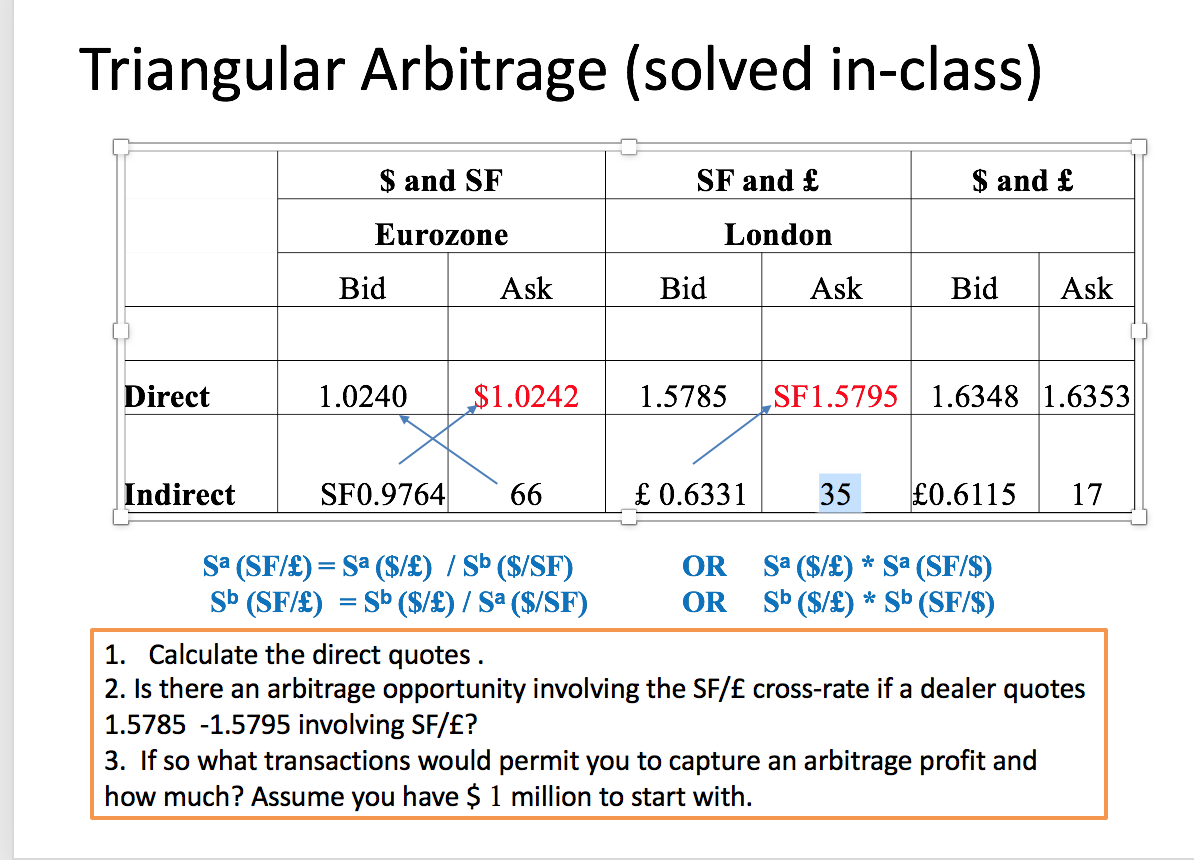

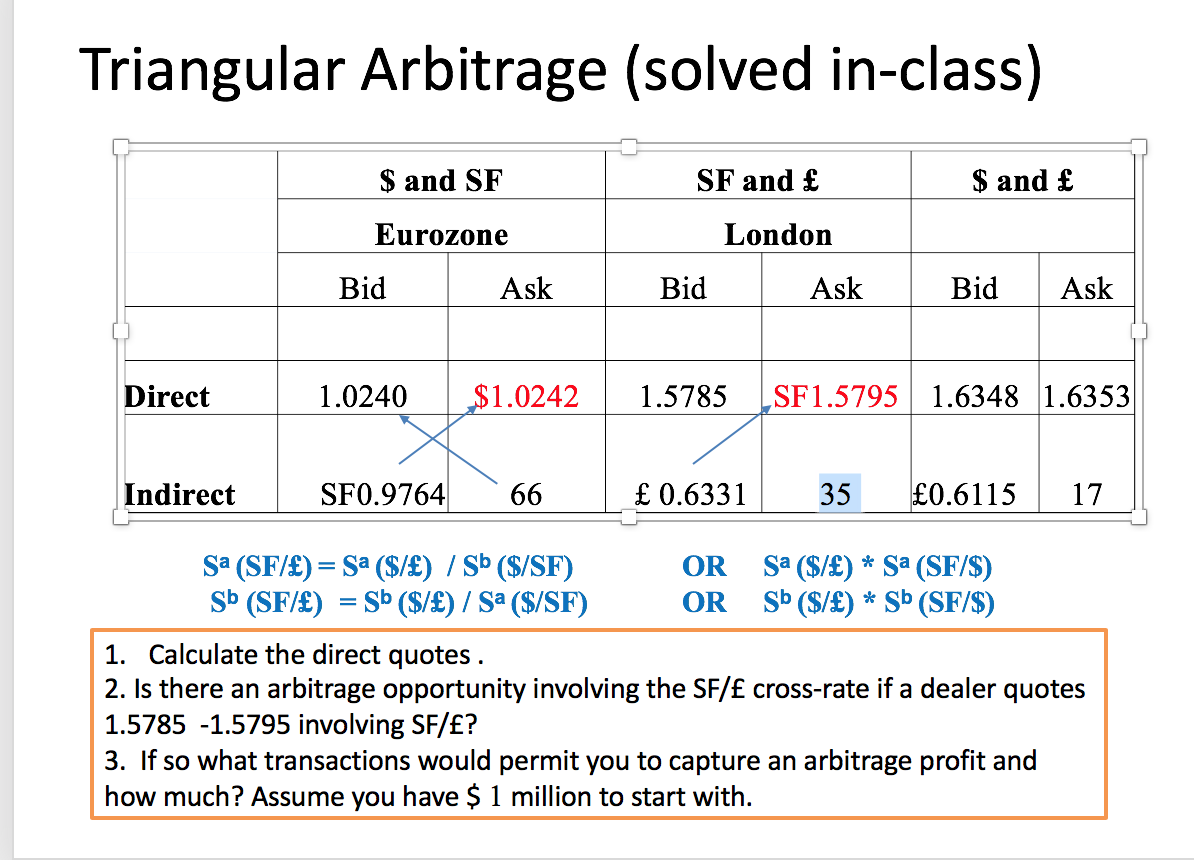

Question: Triangular Arbitrage (solved in-class) $ and SF SF and & $ and f Eurozone London Bid Ask Bid Ask Bid Ask Direct 1.0240 $1.0242 1.5785

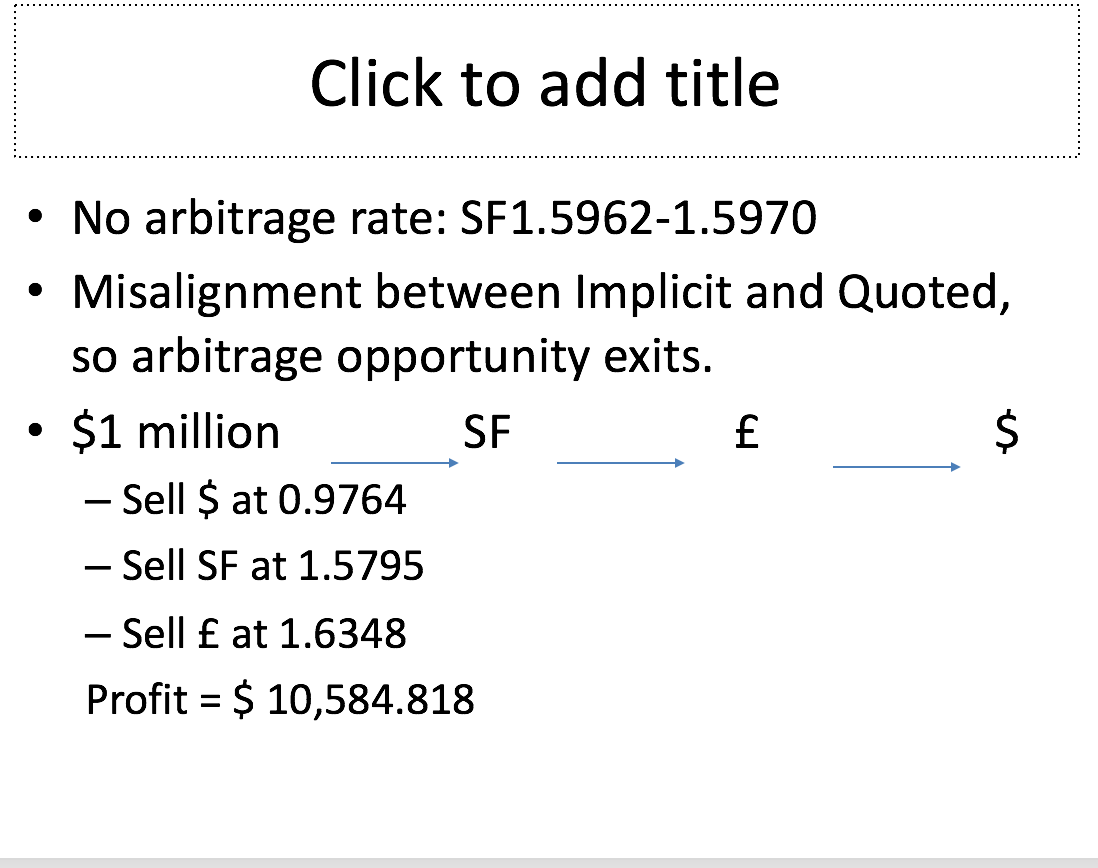

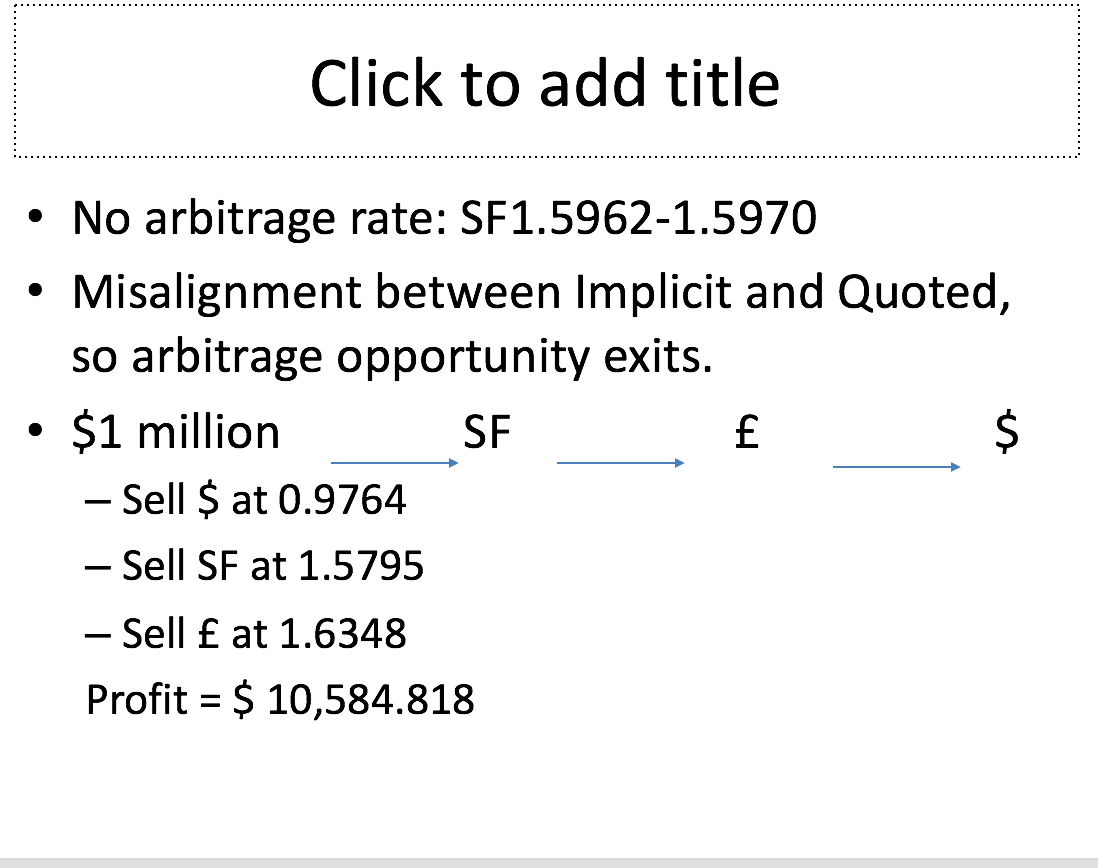

Triangular Arbitrage (solved in-class) $ and SF SF and & $ and f Eurozone London Bid Ask Bid Ask Bid Ask Direct 1.0240 $1.0242 1.5785 SF1.5795 1.6348 1.6353 Indirect SF0.9764 66 E 0.6331 35 10.6115 17 Sa (SF/{) = Sa ($/{) / S ($/SF) OR Sa ($/{) * Sa (SF/$) Sb (SF/{) = Sb ($/{) / Sa ($/SF) OR Sb ($/{) * Sb (SF/$) 1. Calculate the direct quotes . 2. Is there an arbitrage opportunity involving the SF/f cross-rate if a dealer quotes 1.5785 -1.5795 involving SF/f? 3. If so what transactions would permit you to capture an arbitrage profit and how much? Assume you have $ 1 million to start with. No arbitrage rate: SF1.5962-1.5970 Misalignment between Implicit and Quoted, so arbitrage opportunity exits. 0 $1 million SF E S Sell S at 0.9764 Sell SF at 1.5795 Sell E at 1.6348 Profit = S 10,584.818

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts