Question: try tto do all please and thnak you 1. Time Series Models (Week 7) Suppose you want to use time series data to estimate oil

try tto do all please and thnak you

try tto do all please and thnak you

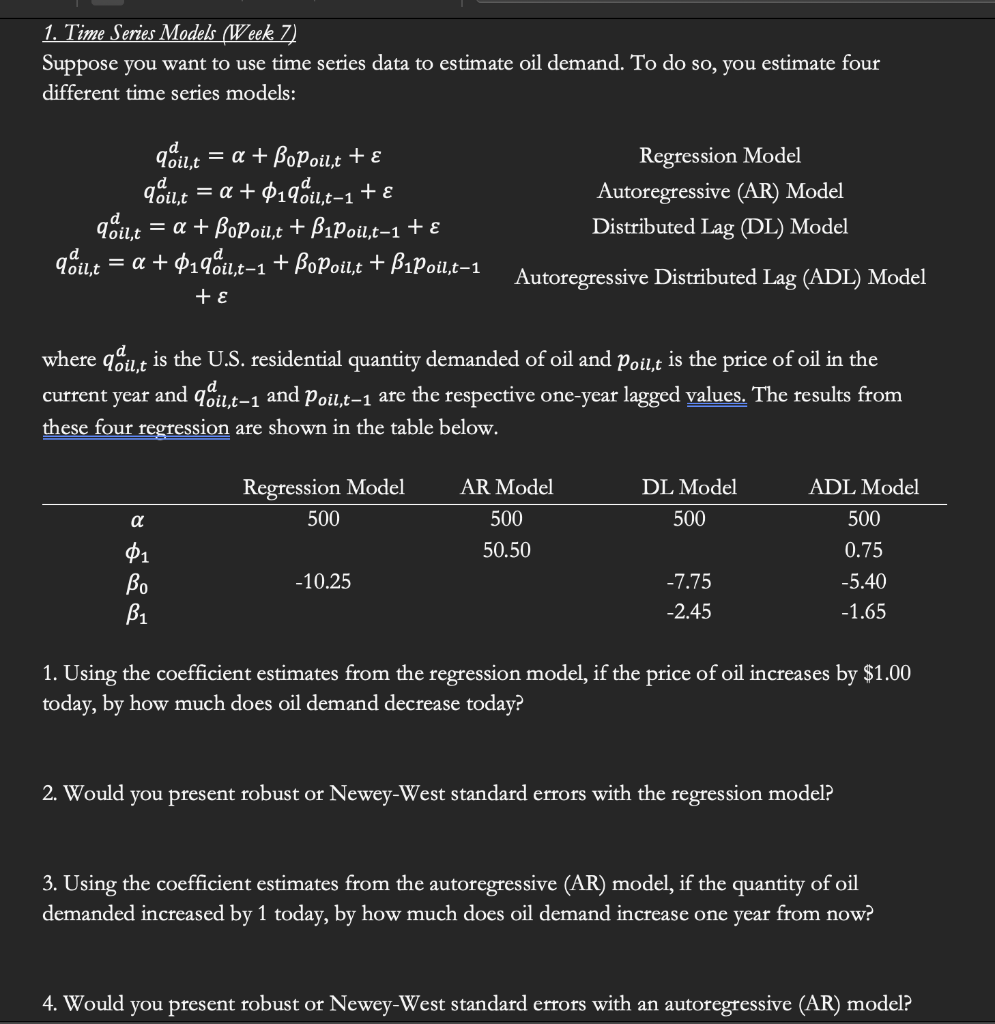

1. Time Series Models (Week 7) Suppose you want to use time series data to estimate oil demand. To do so, you estimate four different time series models: qoil, = a + Bopoil,t + qoil,t = a + 019&il.t-1 + qoil, = a + Bopoil,t + Bipoil,t-1 + gil,t = a + $19.il,t-1 + BoPoil,t + Bipoil.t-1 + Regression Model Autoregressive (AR) Model Distributed Lag (DL) Model Autoregressive Distributed Lag (ADL) Model where qi,t is the U.S. residential quantity demanded of oil and Poil,t is the price of oil in the current year and oil,t-1 and Poil,t-1 are the respective one-year lagged values. The results from these four regression are shown in the table below. AR Model Regression Model 500 DL Model 500 500 50.50 01 Bo Bi ADL Model 500 0.75 -5.40 -1.65 -10.25 -7.75 -2.45 1. Using the coefficient estimates from the regression model, if the price of oil increases by $1.00 today, by how much does oil demand decrease today? 2. Would you present robust or Newey-West standard errors with the regression model? 3. Using the coefficient estimates from the autoregressive (AR) model, if the quantity of oil demanded increased by 1 today, by how much does oil demand increase one year from now? 4. Would you present robust or Newey-West standard errors with an autoregressive (AR) model? 1. Time Series Models (Week 7) Suppose you want to use time series data to estimate oil demand. To do so, you estimate four different time series models: qoil, = a + Bopoil,t + qoil,t = a + 019&il.t-1 + qoil, = a + Bopoil,t + Bipoil,t-1 + gil,t = a + $19.il,t-1 + BoPoil,t + Bipoil.t-1 + Regression Model Autoregressive (AR) Model Distributed Lag (DL) Model Autoregressive Distributed Lag (ADL) Model where qi,t is the U.S. residential quantity demanded of oil and Poil,t is the price of oil in the current year and oil,t-1 and Poil,t-1 are the respective one-year lagged values. The results from these four regression are shown in the table below. AR Model Regression Model 500 DL Model 500 500 50.50 01 Bo Bi ADL Model 500 0.75 -5.40 -1.65 -10.25 -7.75 -2.45 1. Using the coefficient estimates from the regression model, if the price of oil increases by $1.00 today, by how much does oil demand decrease today? 2. Would you present robust or Newey-West standard errors with the regression model? 3. Using the coefficient estimates from the autoregressive (AR) model, if the quantity of oil demanded increased by 1 today, by how much does oil demand increase one year from now? 4. Would you present robust or Newey-West standard errors with an autoregressive (AR) model

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts