Question: ttssay type question. Show your work step by step in order to get point. You can either respond by uploading a file and/or by using

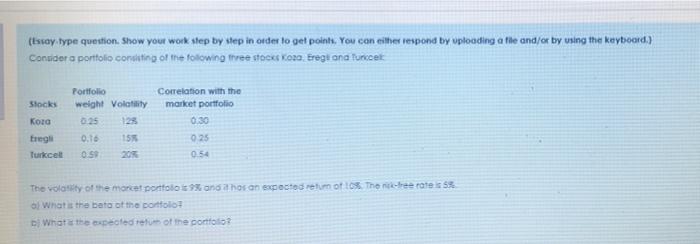

ttssay type question. Show your work step by step in order to get point. You can either respond by uploading a file and/or by using the keyboard) Consider a portfolio conting of the following three stocks Kos. Eregiona funccet Portfolio weight Volatility Correlation with the market portfolio Stocks 0.25 0.30 freg 0.16 15% 0.25 Turkcell 0.5 054 The volaity of the monet portfolio and a hos an expected retum of 105 The rate is What is the bato at the portfolio Dj What the expected return of the portfolio

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock