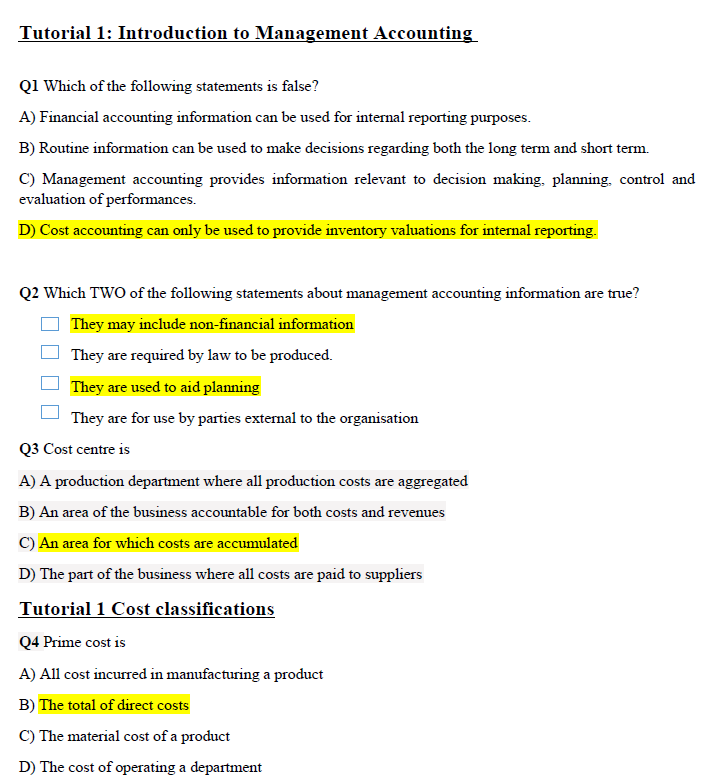

Question: Tutorial 1: Introduction to Management Accounting Q1 Which of the following statements is false? A) Financial accounting information can be used for internal reporting purposes.

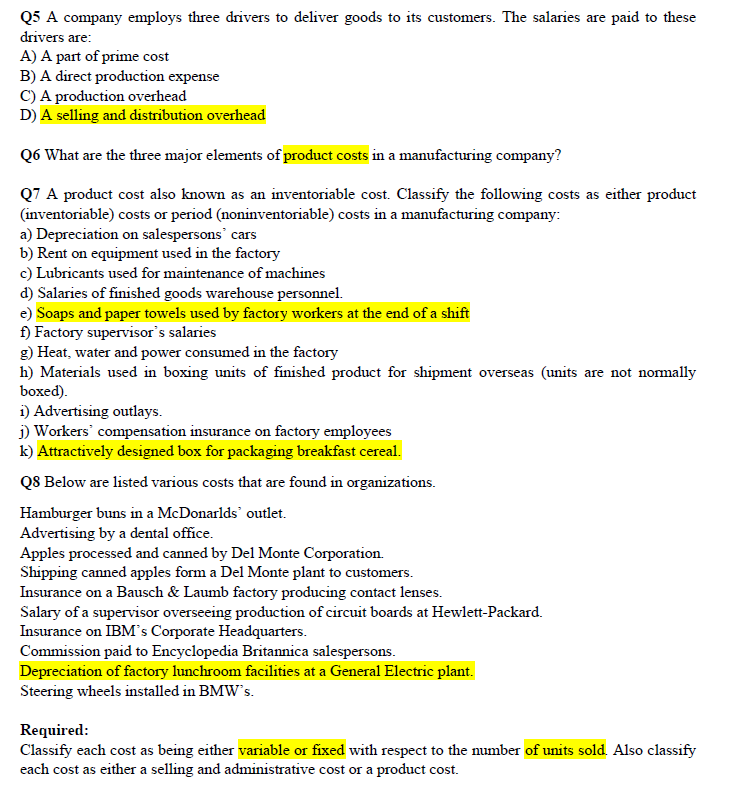

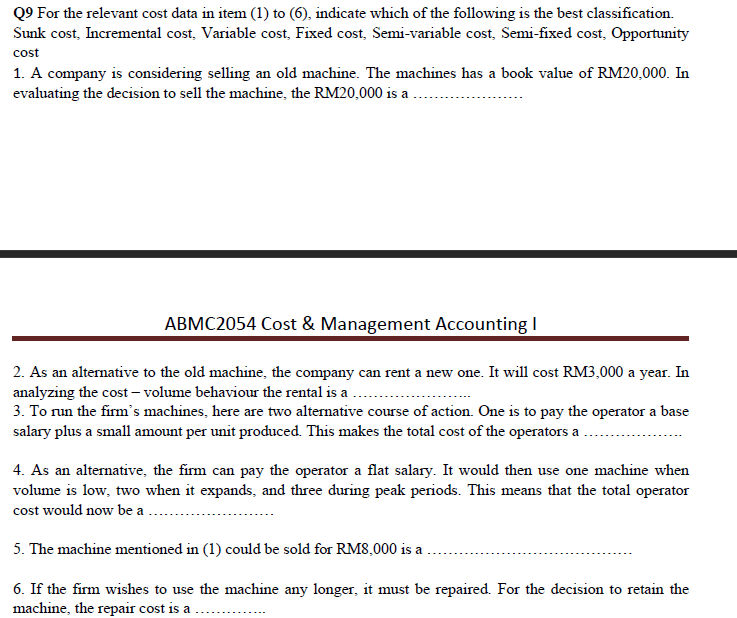

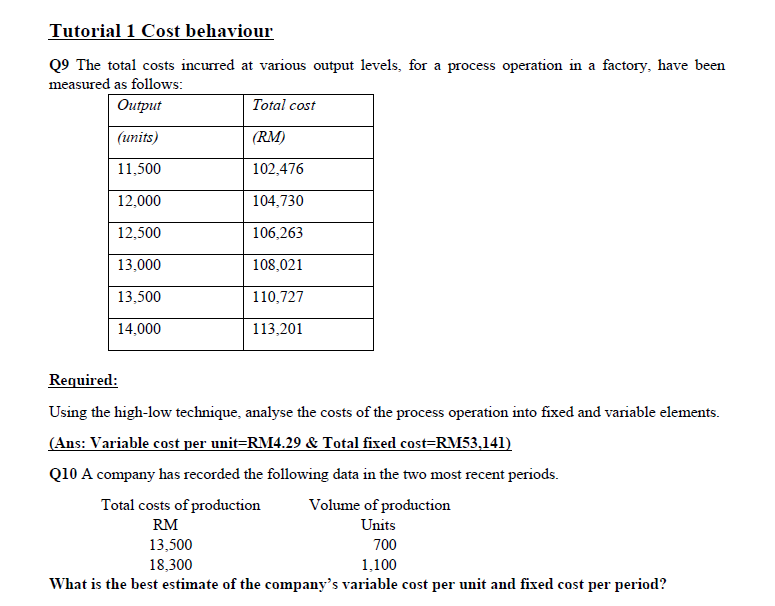

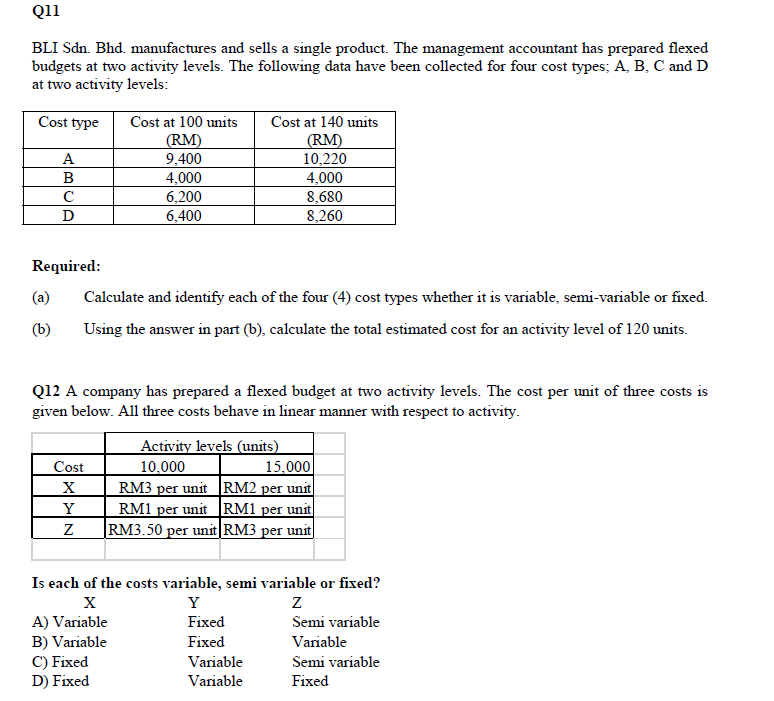

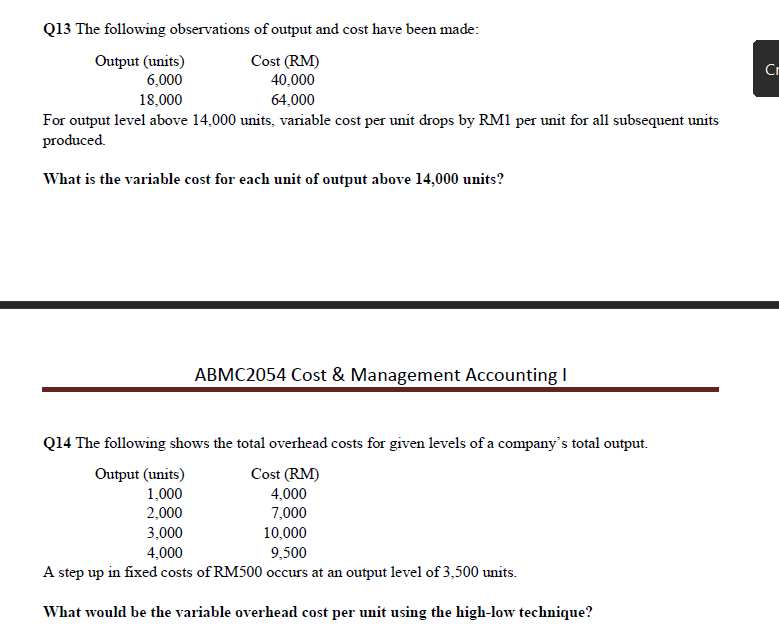

Tutorial 1: Introduction to Management Accounting Q1 Which of the following statements is false? A) Financial accounting information can be used for internal reporting purposes. B) Routine information can be used to make decisions regarding both the long term and short term. () Management accounting provides information relevant to decision making, planning, control and evaluation of performances. D) Cost accounting can only be used to provide inventory valuations for internal reporting. Q2 Which TWO of the following statements about management accounting information are true? They may include non-financial information They are required by law to be produced. They are used to aid planning They are for use by parties external to the organisation Q3 Cost centre is A) A production department where all production costs are aggregated B) An area of the business accountable for both costs and revenues C) An area for which costs are accumulated D) The part of the business where all costs are paid to suppliers Tutorial 1 Cost classifications Q4 Prime cost is A) All cost incurred in manufacturing a product B) The total of direct costs C) The material cost of a product D) The cost of operating a departmentQ5 A company employs three drivers to deliver goods to its customers. The salaries are paid to these drivers are: A) A part of prime cost B) A direct production expense C) A production overhead D) A selling and distribution overhead Q6 What are the three major elements of product costs in a manufacturing company? Q7 A product cost also known as an inventoriable cost. Classify the following costs as either product (inventoriable) costs or period (noninventoriable) costs in a manufacturing company: a) Depreciation on salespersons' cars b) Rent on equipment used in the factory c) Lubricants used for maintenance of machines d) Salaries of finished goods warehouse personnel. e) Soaps and paper towels used by factory workers at the end of a shift f) Factory supervisor's salaries g) Heat, water and power consumed in the factory h) Materials used in boxing units of finished product for shipment overseas (units are not normally boxed). i) Advertising outlays. j) Workers' compensation insurance on factory employees k) Attractively designed box for packaging breakfast cereal. Q8 Below are listed various costs that are found in organizations. Hamburger buns in a McDonarlds' outlet. Advertising by a dental office. Apples processed and canned by Del Monte Corporation. Shipping canned apples form a Del Monte plant to customers. Insurance on a Bausch & Laumb factory producing contact lenses. Salary of a supervisor overseeing production of circuit boards at Hewlett-packard. Insurance on IBM's Corporate Headquarters. Commission paid to Encyclopedia Britannica salespersons. Depreciation of factory lunchroom facilities at a General Electric plant. Steering wheels installed in BMW's. Required: Classify each cost as being either variable or fixed with respect to the number of units sold Also classify each cost as either a selling and administrative cost or a product cost.Q9 For the relevant cost data in item (1) to (6), indicate which of the following is the best classification. Sunk cost, Incremental cost, Variable cost, Fixed cost, Semi-variable cost, Semi-fixed cost, Opportunity cost 1. A company is considering selling an old machine. The machines has a book value of RM20,000. In evaluating the decision to sell the machine, the RM20,000 is a ABMC2054 Cost & Management Accounting I 2. As an alternative to the old machine, the company can rent a new one. It will cost RM3,000 a year. In analyzing the cost - volume behaviour the rental is a 3. To run the firm's machines, here are two alternative course of action. One is to pay the operator a base salary plus a small amount per unit produced. This makes the total cost of the operators a 4. As an alternative, the firm can pay the operator a flat salary. It would then use one machine when volume is low, two when it expands, and three during peak periods. This means that the total operator cost would now be a 5. The machine mentioned in (1) could be sold for RM8,000 is a 6. If the firm wishes to use the machine any longer, it must be repaired. For the decision to retain the machine, the repair cost is a .......Tutorial 1 Cost behaviour Q9 The total costs incurred at various output levels, for a process operation in a factory, have been measured as follows: Output Total cost (units) (RM) 11,500 102,476 12,000 104,730 12,500 106,263 13,000 108,021 13,500 110,727 14,000 113,201 Required: Using the high-low technique, analyse the costs of the process operation into fixed and variable elements. (Ans: Variable cost per unit=RM4.29 & Total fixed cost=RM53,141) Q10 A company has recorded the following data in the two most recent periods. Total costs of production Volume of production RM Units 13,500 700 18,300 1,100 What is the best estimate of the company's variable cost per unit and fixed cost per period?Q11 BLI San. Bhd. manufactures and sells a single product. The management accountant has prepared flexed budgets at two activity levels. The following data have been collected for four cost types; A, B, C and D at two activity levels: Cost type Cost at 100 units Cost at 140 units (RM) (RM) A 9.400 10,220 B 4,000 4,000 C 6,200 8,680 D 5.400 8,260 Required: (a) Calculate and identify each of the four (4) cost types whether it is variable, semi-variable or fixed. (b ) Using the answer in part (b), calculate the total estimated cost for an activity level of 120 units. Q12 A company has prepared a flexed budget at two activity levels. The cost per unit of three costs is given below. All three costs behave in linear manner with respect to activity. Activity levels (units) Cost 10,000 15,000 X RM3 per unit RM2 per unit Y RM1 per unit RM1 per unit Z |RM3.50 per unit RM3 per unit Is each of the costs variable, semi variable or fixed? X Y Z A) Variable Fixed Semi variable B) Variable Fixed Variable C) Fixed Variable Semi variable D) Fixed Variable FixedQ13 The following observations of output and cost have been made: Output (units) Cost (RM) C 6,000 40,000 18,000 64,000 For output level above 14,000 units, variable cost per unit drops by RM1 per unit for all subsequent units produced. What is the variable cost for each unit of output above 14,000 units? ABMC2054 Cost & Management Accounting I Q14 The following shows the total overhead costs for given levels of a company's total output. Output (units) Cost (RM) 1,000 4,000 2,000 7,000 3,000 10,000 4,000 9,500 A step up in fixed costs of RM500 occurs at an output level of 3,500 units. What would be the variable overhead cost per unit using the high-low technique

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock

Students Have Also Explored These Related Accounting Questions!