Question: Two Departments, Journal Entries with Supporting Calculations-Weighted Average Method Patterson Laboratories, Ic., produces one of its products in two successive departments. All materials are added

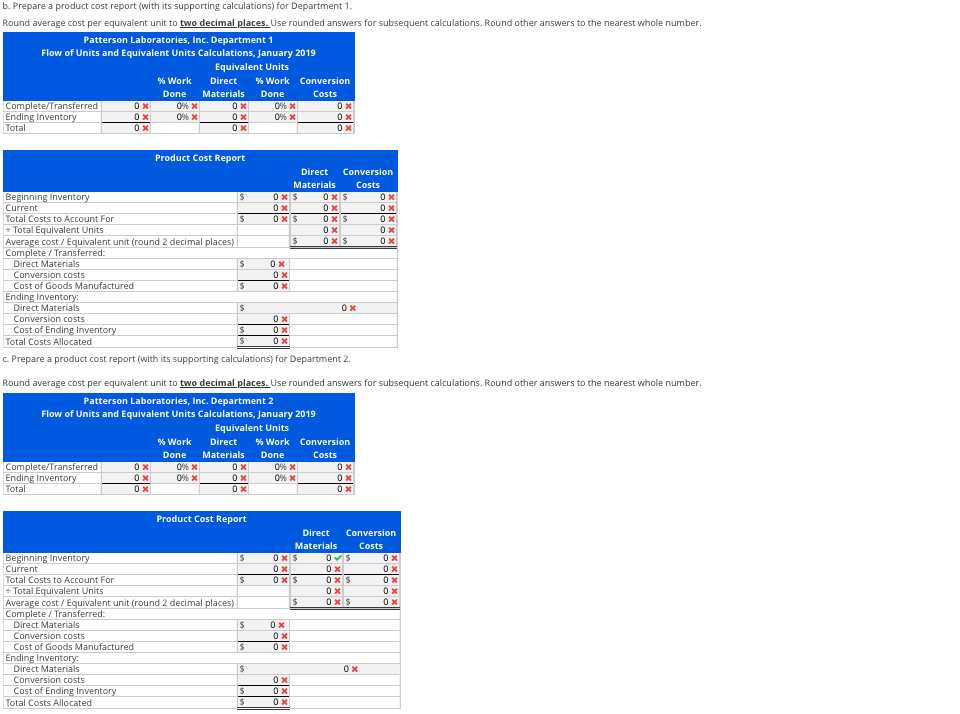

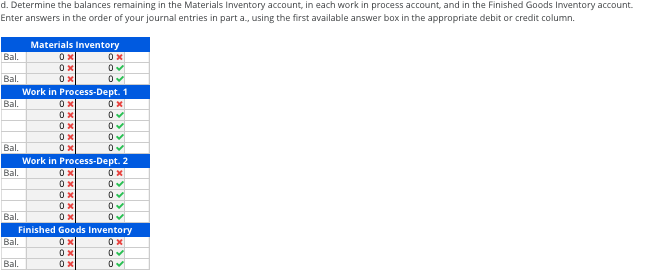

Two Departments, Journal Entries with Supporting Calculations-Weighted Average Method Patterson Laboratories, Ic., produces one of its products in two successive departments. All materials are added at the beginning of the process in Department 1; no materials are used in Department 2. Conversion costs are incurred evenly in both departments. Patterson uses the weighted average method for process costing. January 1, 2019, inventory account balances are as follows: Materials inventory Work in process-Department 1 (3,000 units, 30% complete) Direct material Conversion costs Work in process-Department 2 (3,550 units, 40% complete) 43,439 Finished goods inventory (2,000 units @ $16) $30,000 4,560 10,640 32,000 During January, the following transactions occurred: 1. Purchased material on account, $90,000. 2. Placed $84,000 of material into process in Department 1. This $84,000 represents 24,000 units of materials. 3. Distributed total payroll costs: $108,116 of direct labor to Department 1, $62,700 of direct labor to Department 2, and $51,000 of indirect labor to Manufacturing Overhead. 4. Incurred other actual manufacturing overhead costs, $81,000. (Credit Other Accounts.) 5. Applied overhead to the two processing departments: $88,000 to Department 1 and $43,900 to Department 2. 6. Transferred 25,000 completed units from Department 1 to Department 2. The 2,000 units remaining in Department 1 were 20% completed with respect to conversion costs. 7. Transferred 26,000 completed units from Department 2 to finished goods inventory. The 2,550 units remaining in Department 2 were 70% completed with respect to conversion costs. 8. Sold 20,000 units on account at $27 per unit. Patterson uses weighted average inventory costing procedures for the finished goods inventory. a. Record the January transactions in general journal form for Department 1 and Department 2. Hint: Complete the product cost reports for Departments 1 and 2 before entering journal entries for transactions 6, 7, and 8. General Journal Description Materials inventory Accounts Payable Work in process-Depar :v Materials inventory : 3. Work in process-Department 1 Work in process-Department 2 Manufacturing overhea v Wages payable Manufacturing overhea v Other accounts 5. Work in process-Department 1 Work in process-Depar : v Manufacturing overhe = 6. Work in process-Depar : v Work in process-Depa v Finished goods invento = Work in process-Depa :v Accounts receivable Ref. Debit Credit 90,000 v 1. 90,000 2. 84,000 84,000 108,116 v 62,700 v 51,000 221,816 v 81,000 v 81,000 v 88,000 43,900 v 131,900 v 0x 0x 7. 540,000 8. 540,000v Sales To record sales. Cost of goods sold Finished goods invent To record cost of goods sold. 0x 0x b. Prepare a product cost report (with its supporting calculations) for Department 1. Round average cost per equivalent unit to two decimal places. Use rounded answers for subsequent calculations. Round other answers to the nearest whole number. Patterson Laboratories, Inc. Department 1 Flow of Units and Equivalent Units Calculations, January 2019 Equivalent Units % Work % Work Conversion Direct Materials Done Done Costs Complete/Transferred Ending Inventory Total 0x Product Cost Report Conversion Direct Materials Costs Beginning Inventory Current Total Costs to Account For + Total Equivalent Units Average cost / Equivalent unit (round 2 decimal places) Complete / Transferred: Direct Materials Conversion costs Cost of Goods Manufactured Ending Inventory: Direct Materials Conversion costs Cost of Ending Inventory Total Costs Allocated c. Prepare a product cost report (with its supporting calculations) for Department 2. Round average cost per equivalent unit to two decimal places. Use rounded answers for subsequent calculations. Round other answers to the nearest whole number. Patterson Laboratories, Inc. Department 2 Flow of Units and Equivalent Units Calculations, January 2019 Equivalent Units % Work % Work Conversion Direct Materials Done Done Costs Complete/Transferred Ending Inventory Total 0% x 0% x 0x 0% x Product Cost Report Direct Conversion Materials Costs Beginning Inventory Current Total Costs to Account For + Total Equivalent Units Average cost / Equivalent unit (round 2 decimal places) Complete / Transferred: Direct Materials Conversion costs Cost of Goods Manufactured Ending Inventory: Direct Materials Conversion costs Cost of Ending Inventory Total Costs Allocated %24 d. Determine the balances remaining in the Materials Inventory account, in each work in process account, and in the Finished Goods Inventory account. Enter answers in the order of your journal entries in part a., using the first available answer box in the appropriate debit or credit column. Materials Inventory Bal. Bal. Work in Process-Dept. 1 Bal. Bal. Work in Process-Dept. 2 Bal. 0x Bal. Finished Goods Inventory Bal. Bal

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts