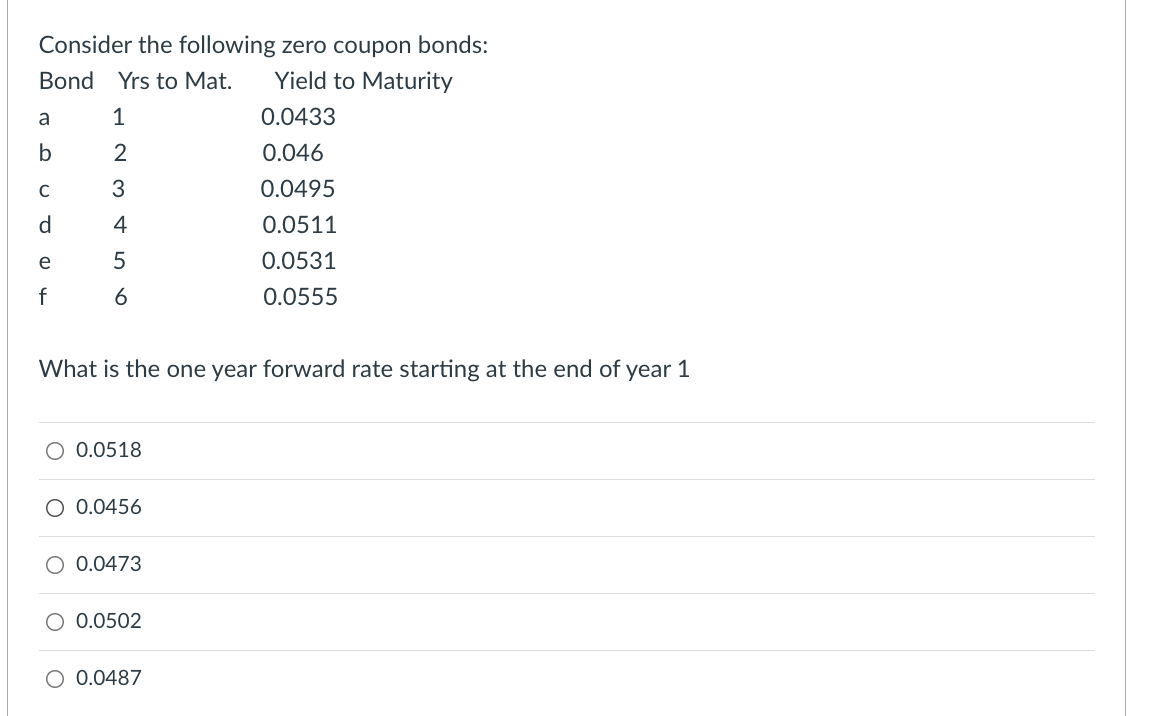

Question: TWO PART QUESTION Consider the following zero coupon bonds: Bond Yrs to Mat. Yield to Maturity 0.0433 0.046 0.0495 0.0511 0.0531 0.0555 TOUJO 4 a

TWO PART QUESTION

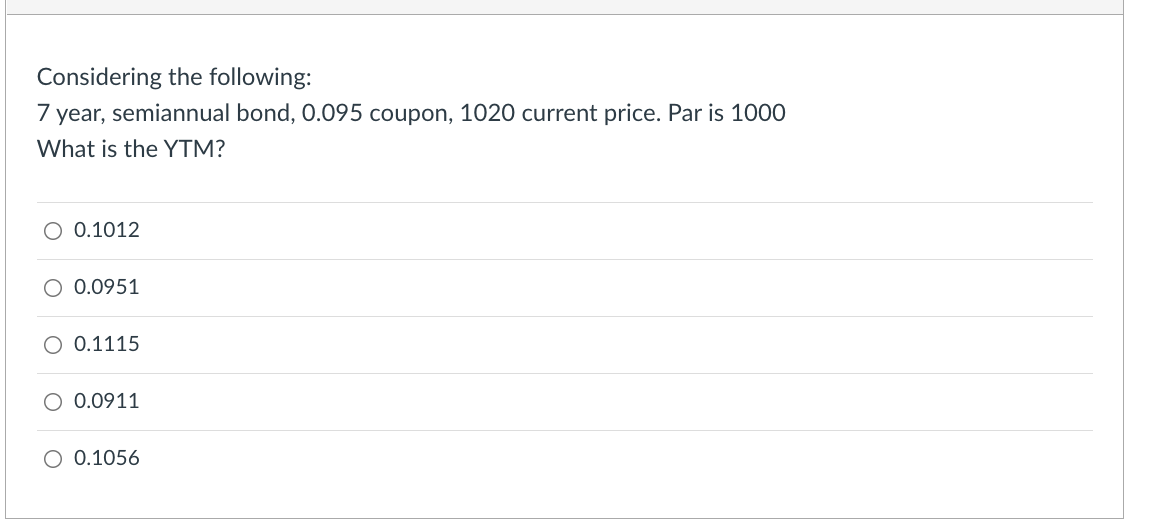

Consider the following zero coupon bonds: Bond Yrs to Mat. Yield to Maturity 0.0433 0.046 0.0495 0.0511 0.0531 0.0555 TOUJO 4 a b C d e f 1 2 3 4 5 6 What is the one year forward rate starting at the end of year 1 0.0518 0.0456 0.0473 0.0502 O 0.0487 Considering the following: 7 year, semiannual bond, 0.095 coupon, 1020 current price. Par is 1000 What is the YTM? O 0.1012 O 0.0951 O 0.1115 O 0.0911 O 0.1056

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock