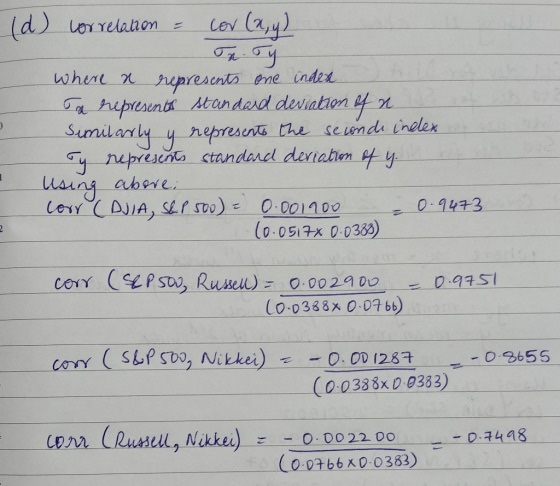

Question: u (d) correlation = cor (x,y) Troy where a represents one index Ca representa standard deviation of a Similarly y represents the seconde index y

u (d) correlation = cor (x,y) Troy where a represents one index Ca representa standard deviation of a Similarly y represents the seconde index y represents Standard deviation of y. : corr (DJIA, S&P 500) = 0.001900 0.9473 (0.0517x 0.0388) 1 Using above 2 corr (sepsoo, Russell) = 0.002900 10.0388x 0. 0766) =0.9751 corr (S&P500, Nikkei) 0.8655 -0.001287 (0.0388%0.0383) corr (Russell, Nikkei) -0.7498 0.002200 (0.0766X0-0383) u (d) correlation = cor (x,y) Troy where a represents one index Ca representa standard deviation of a Similarly y represents the seconde index y represents Standard deviation of y. : corr (DJIA, S&P 500) = 0.001900 0.9473 (0.0517x 0.0388) 1 Using above 2 corr (sepsoo, Russell) = 0.002900 10.0388x 0. 0766) =0.9751 corr (S&P500, Nikkei) 0.8655 -0.001287 (0.0388%0.0383) corr (Russell, Nikkei) -0.7498 0.002200 (0.0766X0-0383)

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts