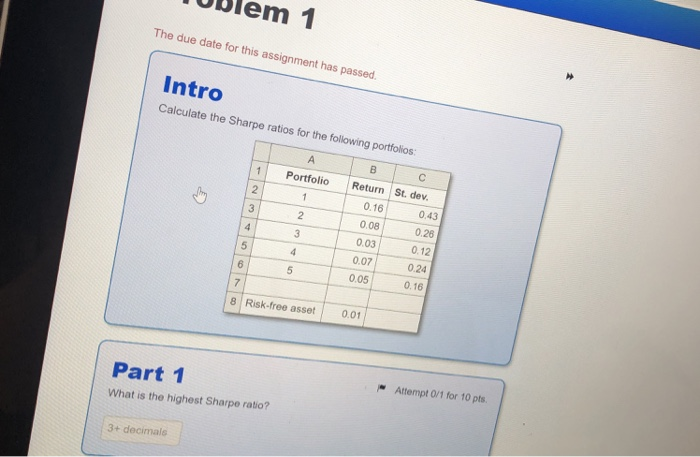

Question: UBlem 1 The due date for this assignment has passed. Intro Calculate the Sharpe ratios for the following portfolios: 1Portfolio Return St. dev 2 3

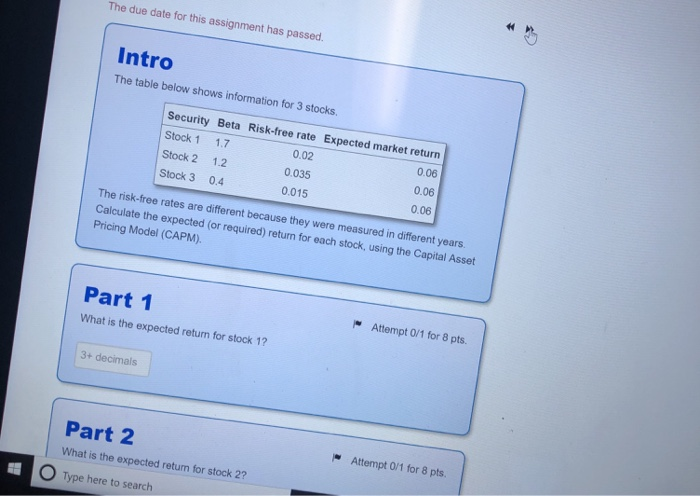

UBlem 1 The due date for this assignment has passed. Intro Calculate the Sharpe ratios for the following portfolios: 1Portfolio Return St. dev 2 3 0.16 0.08 0.03 0.07 0.05 0,43 0.26 0.12 0.24 0.16 2 8 Risk-free asset 0.01 Attempt 0/1 for 10 pts Part 1 What is the highest Sharpe ratio? 3+ decimals The due date for this assignment has passed. Intro The table below shows information for 3 stocks. Security Beta Risk-free rate Expected market return Stock 1 1.7 Stock 2 1.2 Stock 3 0.4 0.02 0.035 0.015 0.06 0.06 0.06 The risk-free rates are different because they were measured Calcu Pricing Model(CAPM). in different years late the expected (or required) return for each stock, using the Capital Asset Attempt 0/1 for 8 pts Part 1 What is the expected return for stock 1? 3+ decimals Attempt 0/1 for 8 pts Part 2 What is the expected return for stock 2? Type here to search

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts