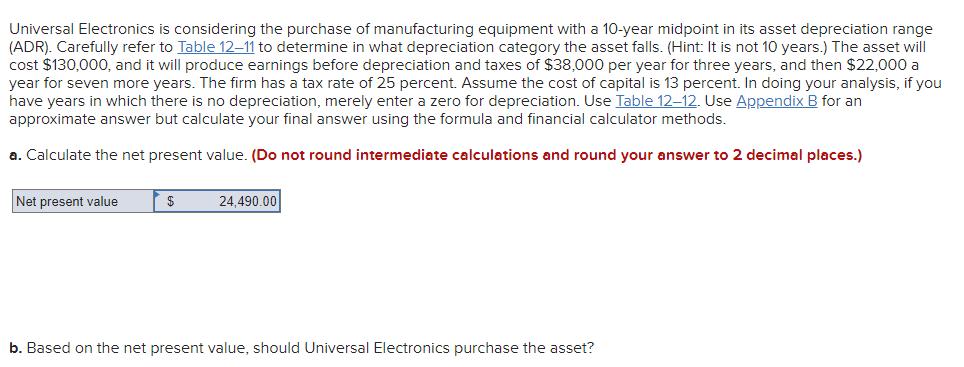

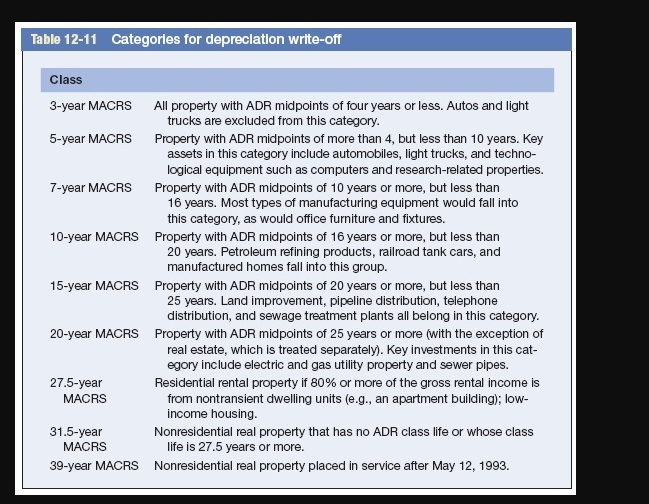

Universal Electronics is considering the purchase of manufacturing equipment with a 10-year midpoint in its asset...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

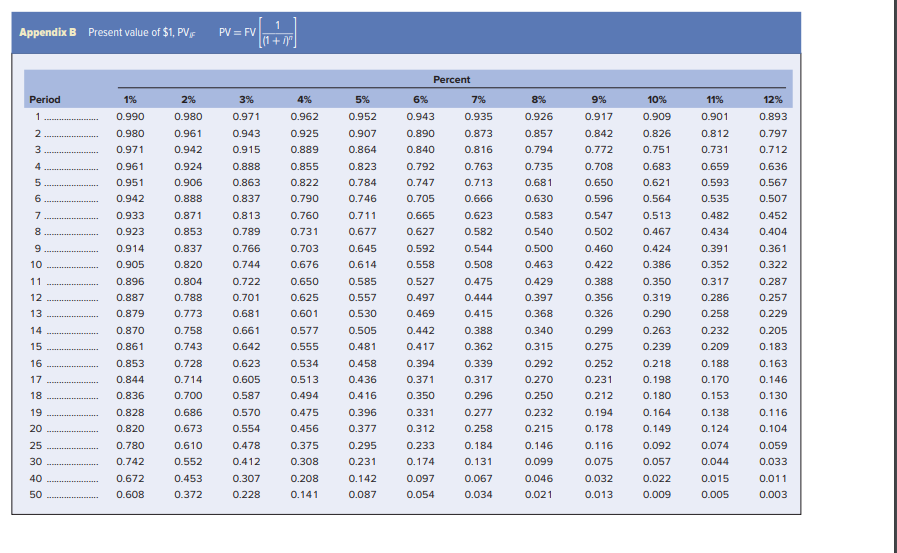

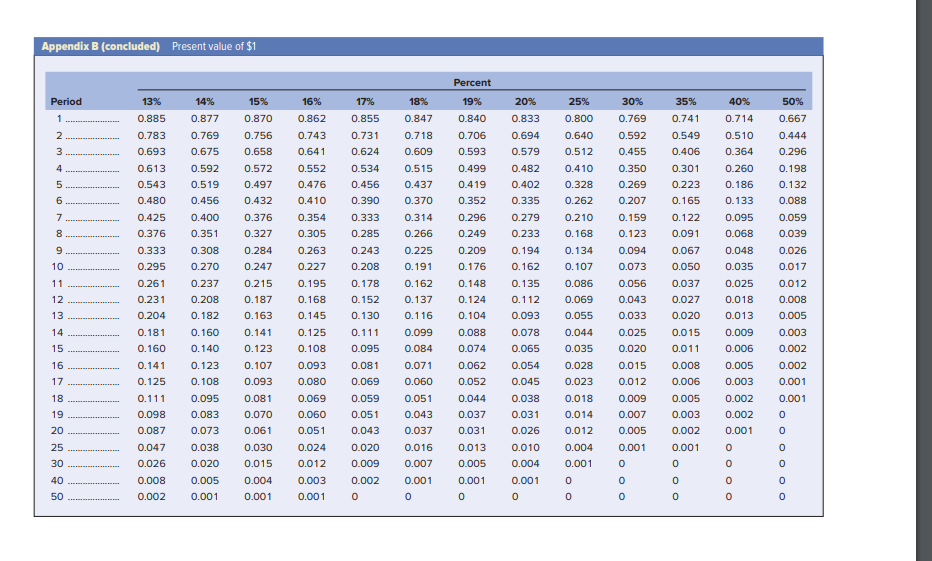

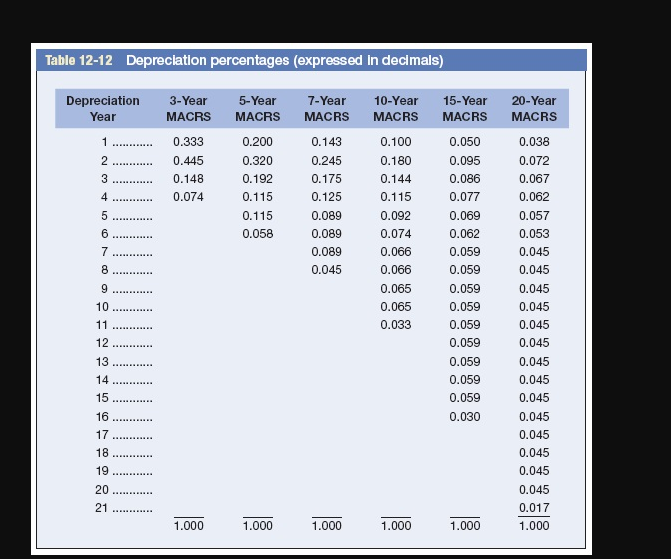

Universal Electronics is considering the purchase of manufacturing equipment with a 10-year midpoint in its asset depreciation range (ADR). Carefully refer to Table 12-11 to determine in what depreciation category the asset falls. (Hint: It is not 10 years.) The asset will cost $130,000, and it will produce earnings before depreciation and taxes of $38,000 per year for three years, and then $22,000 a year for seven more years. The firm has a tax rate of 25 percent. Assume the cost of capital is 13 percent. In doing your analysis, if you have years in which there is no depreciation, merely enter a zero for depreciation. Use Table 12-12. Use Appendix B for an approximate answer but calculate your final answer using the formula and financial calculator methods. a. Calculate the net present value. (Do not round intermediate calculations and round your answer to 2 decimal places.) Net present value $ 24,490.00 b. Based on the net present value, should Universal Electronics purchase the asset? Appendix B Present value of $1, PV 1 PV=FV [(1 + 1)^. Percent Period 1% 2% 3% 4% 5% 6% 7% 8% 9% 10% 11% 12% 1 0.990 0.980 0.971 0.962 0.952 0.943 0.935 0.926 0.917 0.909 0.901 0.893 2 0.980 0.961 0.943 0.925 0.907 0.890 0.873 0.857 0.842 0.826 0.812 0.797 3 0.971 0.942 0.915 0.889 0.864 0.840 0.816 0.794 0.772 0.751 0.731 0.712 4 0.961 0.924 0.888 0.855 0.823 0.792 0.763 0.735 0.708 0.683 0.659 0.636 5 0.951 0.906 0.863 0.822 0.784 0.747 0.713 0.681 0.650 0.621 0.593 0.567 6 0.942 0.888 0.837 0.790 0.746 0.705 0.666 0.630 0.596 0.564 0.535 0.507 7 0.933 0.871 0.813 0.760 0.711 0.665 0.623 0.583 0.547 0.513 0.482 0.452 8 0.923 0.853 0.789 0.731 0.677 0.627 0.582 0.540 0.502 0.467 0.434 0.404 9 0.914 0.837 0.766 0.703 0.645 0.592 0.544 0.500 0.460 0.424 0.391 0.361 10 0.905 0.820 0.744 0.676 0.614 0.558 0.508 0.463 0.422 0.386 0.352 0.322 11 0.896 0.804 0.722 0.650 0.585 0.527 0.475 0.429 0.388 0.350 0.317 0.287 12 13 JN 0.887 0.788 0.701 0.625 0.557 0.497 0.444 0.397 0.356 0.319 0.286 0.257 0.879 0.773 0.681 0.601 0.530 0.469 0.415 0.368 0.326 0.290 0.258 0.229 14 0.870 0.758 0.661 0.577 0.505 0.442 0.388 0.340 0.299 0.263 0.232 0.205 15 0.861 0.743 0.642 0.555 0.481 0.417 0.362 0.315 0.275 0.239 0.209 0.183 16 0.853 0.728 0.623 0.534 0.458 0.394 0.339 0.292 0.252 0.218 0.188 0.163 17 0.844 0.714 0.605 0.513 0.436 0.371 0.317 0.270 0.231 0.198 0.170 0.146 18 0.836 0.700 0.587 0.494 0.416 0.350 0.296 0.250 0.212 0.180 0.153 0.130 19 0.828 0.686 0.570 0.475 0.396 0.331 0.277 0.232 0.194 0.164 0.138 0.116 20 0.820 0.673 0.554 0.456 0.377 0.312 0.258 0.215 0.178 0.149 0.124 0.104 25 0.780 0.610 0.478 0.375 0.295 0.233 0.184 0.146 0.116 0.092 0.074 0.059 30 0.742 0.552 0.412 0.308 0.231 0.174 0.131 0.099 0.075 0.057 0.044 0.033 40 0.672 0.453 0.307 0.208 0.142 0.097 0.067 0.046 0.032 0.022 0.015 0.011 50 0.608 0.372 0.228 0.141 0.087 0.054 0.034 0.021 0.013 0.009 0.005 0.003 Appendix B (concluded) Present value of $1 Percent Period 13% 14% 15% 16% 17% 18% 19% 20% 25% 30% 35% 40% 50% 1 0.885 0.877 0.870 0.862 0.855 0.847 0.840 0.833 0.800 0.769 0.741 0.714 0.667 2 0.783 0.769 0.756 0.743 0.731 0.718 0.706 0.694 0.640 0.592 0.549 0.510 0.444 3 0.693 0.675 0.658 0.641 0.624 0.609 0.593 0.579 0.512 0.455 0.406 0.364 0.296 4 0.613 0.592 0.572 0.552 0.534 0.515 0.499 0.482 0.410 0.350 0.301 0.260 0.198 5 0.543 0.519 0.497 0.476 0.456 0.437 0.419 0.402 0.328 0.269 0.223 0.186 0.132 6 0.480 0.456 0.432 0.410 0.390 0.370 0.352 0.335 0.262 0.207 0.165 0.133 0.088 7 0.425 0.400 0.376 0.354 0.333 0.314 0.296 0.279 0.210 0.159 0.122 0.095 0.059 8 0.376 0.351 0.327 0.305 0.285 0.266 0.249 0.233 0.168 0.123 0.091 0.068 0.039 9 0.333 0.308 0.284 0.263 0.243 0.225 0.209 0.194 0.134 0.094 0.067 0.048 0.026 10 0.295 0.270 0.247 0.227 0.208 0.191 0.176 0.162 0.107 0.073 0.050 0.035 0.017 11 0.261 0.237 0.215 0.195 0.178 0.162 0.148 0.135 0.086 0.056 0.037 0.025 0.012 12 0.231 0.208 0.187 0.168 0.152 0.137 0.124 0.112 0.069 0.043 0.027 0.018 0.008 13 0.204 0.182 0.163 0.145 0.130 0.116 0.104 0.093 0.055 0.033 0.020 0.013 0.005 14 0.181 0.160 0.141 0.125 0.111 0.099 0.088 0.078 0.044 0.025 0.015 0.009 0.003 15 0.160 0.140 0.123 0.108 0.095 0.084 0.074 0.065 0.035 0.020 0.011 0.006 0.002 16 0.141 0.123 0.107 0.093 0.081 0.071 0.062 0.054 0.028 0.015 0.008 0.005 0.002 17 0.125 0.108 0.093 0.080 0.069 0.060 0.052 0.045 0.023 0.012 0.006 0.003 0.001 18 0.111 0.095 0.081 0.069 0.059 0.051 0.044 0.038 0.018 0.009 0.005 0.002 0.001 19 0.098 0.083 0.070 0.060 0.051 0.043 0.037 0.031 0.014 0.007 0.003 0.002 20 0.087 0.073 0.061 0.051 0.043 0.037 0.031 0.026 0.012 0.005 0.002 0.001 25 0.047 0.038 0.030 0.024 0.020 0.016 0.013 0.010 0.004 0.001 0.001 0 30 0.026 0.020 0.015 0.012 0.009 0.007 0.005 0.004 0.001 40 0.008 0.005 0.004 0.003 0.002 0.001 0.001 0.001 0 50 0.002 0.001 0.001 0.001 0 0 0 0 0 000 0 0 0 0 oooooo Table 12-12 Depreciation percentages (expressed in decimals) Depreciation 3-Year 5-Year 7-Year Year MACRS MACRS MACRS 10-Year 15-Year MACRS MACRS 20-Year MACRS 1 ...... 0.333 0.200 0.143 0.100 0.050 0.038 234 2 0.445 0.320 0.245 0.180 0.095 0.072 3 0.148 0.192 0.175 0.144 0.086 0.067 4 0.074 0.115 0.125 0.115 0.077 0.062 6698 5 0.115 0.089 0.092 0.069 0.057 0.058 0.089 0.074 0.062 0.053 7 0.089 0.066 0.059 0.045 0.045 0.066 0.059 0.045 9 10 11 12 13 14 0.065 0.059 0.045 0.065 0.059 0.045 0.033 0.059 0.045 0.059 0.045 0.059 0.045 0.059 0.045 15 16 5 0.059 0.045 0.030 0.045 17 0.045 18 0.045 19 0.045 20 0.045 21 0.017 1.000 1.000 1.000 1.000 1.000 1.000 Table 12-11 Categories for depreciation write-off Class 3-year MACRS 5-year MACRS 7-year MACRS All property with ADR midpoints of four years or less. Autos and light trucks are excluded from this category. Property with ADR midpoints of more than 4, but less than 10 years. Key assets in this category include automobiles, light trucks, and techno- logical equipment such as computers and research-related properties. Property with ADR midpoints of 10 years or more, but less than 16 years. Most types of manufacturing equipment would fall into this category, as would office furniture and fixtures. 10-year MACRS Property with ADR midpoints of 16 years or more, but less than 20 years. Petroleum refining products, railroad tank cars, and manufactured homes fall into this group. 15-year MACRS Property with ADR midpoints of 20 years or more, but less than 25 years. Land improvement, pipeline distribution, telephone distribution, and sewage treatment plants all belong in this category. 20-year MACRS Property with ADR midpoints of 25 years or more (with the exception of real estate, which is treated separately). Key investments in this cat- egory include electric and gas utility property and sewer pipes. Residential rental property if 80% or more of the gross rental income is from nontransient dwelling units (e.g., an apartment building); low- income housing. 27.5-year MACRS 31.5-year MACRS Nonresidential real property that has no ADR class life or whose class life is 27.5 years or more. 39-year MACRS Nonresidential real property placed in service after May 12, 1993. Universal Electronics is considering the purchase of manufacturing equipment with a 10-year midpoint in its asset depreciation range (ADR). Carefully refer to Table 12-11 to determine in what depreciation category the asset falls. (Hint: It is not 10 years.) The asset will cost $130,000, and it will produce earnings before depreciation and taxes of $38,000 per year for three years, and then $22,000 a year for seven more years. The firm has a tax rate of 25 percent. Assume the cost of capital is 13 percent. In doing your analysis, if you have years in which there is no depreciation, merely enter a zero for depreciation. Use Table 12-12. Use Appendix B for an approximate answer but calculate your final answer using the formula and financial calculator methods. a. Calculate the net present value. (Do not round intermediate calculations and round your answer to 2 decimal places.) Net present value $ 24,490.00 b. Based on the net present value, should Universal Electronics purchase the asset? Appendix B Present value of $1, PV 1 PV=FV [(1 + 1)^. Percent Period 1% 2% 3% 4% 5% 6% 7% 8% 9% 10% 11% 12% 1 0.990 0.980 0.971 0.962 0.952 0.943 0.935 0.926 0.917 0.909 0.901 0.893 2 0.980 0.961 0.943 0.925 0.907 0.890 0.873 0.857 0.842 0.826 0.812 0.797 3 0.971 0.942 0.915 0.889 0.864 0.840 0.816 0.794 0.772 0.751 0.731 0.712 4 0.961 0.924 0.888 0.855 0.823 0.792 0.763 0.735 0.708 0.683 0.659 0.636 5 0.951 0.906 0.863 0.822 0.784 0.747 0.713 0.681 0.650 0.621 0.593 0.567 6 0.942 0.888 0.837 0.790 0.746 0.705 0.666 0.630 0.596 0.564 0.535 0.507 7 0.933 0.871 0.813 0.760 0.711 0.665 0.623 0.583 0.547 0.513 0.482 0.452 8 0.923 0.853 0.789 0.731 0.677 0.627 0.582 0.540 0.502 0.467 0.434 0.404 9 0.914 0.837 0.766 0.703 0.645 0.592 0.544 0.500 0.460 0.424 0.391 0.361 10 0.905 0.820 0.744 0.676 0.614 0.558 0.508 0.463 0.422 0.386 0.352 0.322 11 0.896 0.804 0.722 0.650 0.585 0.527 0.475 0.429 0.388 0.350 0.317 0.287 12 13 JN 0.887 0.788 0.701 0.625 0.557 0.497 0.444 0.397 0.356 0.319 0.286 0.257 0.879 0.773 0.681 0.601 0.530 0.469 0.415 0.368 0.326 0.290 0.258 0.229 14 0.870 0.758 0.661 0.577 0.505 0.442 0.388 0.340 0.299 0.263 0.232 0.205 15 0.861 0.743 0.642 0.555 0.481 0.417 0.362 0.315 0.275 0.239 0.209 0.183 16 0.853 0.728 0.623 0.534 0.458 0.394 0.339 0.292 0.252 0.218 0.188 0.163 17 0.844 0.714 0.605 0.513 0.436 0.371 0.317 0.270 0.231 0.198 0.170 0.146 18 0.836 0.700 0.587 0.494 0.416 0.350 0.296 0.250 0.212 0.180 0.153 0.130 19 0.828 0.686 0.570 0.475 0.396 0.331 0.277 0.232 0.194 0.164 0.138 0.116 20 0.820 0.673 0.554 0.456 0.377 0.312 0.258 0.215 0.178 0.149 0.124 0.104 25 0.780 0.610 0.478 0.375 0.295 0.233 0.184 0.146 0.116 0.092 0.074 0.059 30 0.742 0.552 0.412 0.308 0.231 0.174 0.131 0.099 0.075 0.057 0.044 0.033 40 0.672 0.453 0.307 0.208 0.142 0.097 0.067 0.046 0.032 0.022 0.015 0.011 50 0.608 0.372 0.228 0.141 0.087 0.054 0.034 0.021 0.013 0.009 0.005 0.003 Appendix B (concluded) Present value of $1 Percent Period 13% 14% 15% 16% 17% 18% 19% 20% 25% 30% 35% 40% 50% 1 0.885 0.877 0.870 0.862 0.855 0.847 0.840 0.833 0.800 0.769 0.741 0.714 0.667 2 0.783 0.769 0.756 0.743 0.731 0.718 0.706 0.694 0.640 0.592 0.549 0.510 0.444 3 0.693 0.675 0.658 0.641 0.624 0.609 0.593 0.579 0.512 0.455 0.406 0.364 0.296 4 0.613 0.592 0.572 0.552 0.534 0.515 0.499 0.482 0.410 0.350 0.301 0.260 0.198 5 0.543 0.519 0.497 0.476 0.456 0.437 0.419 0.402 0.328 0.269 0.223 0.186 0.132 6 0.480 0.456 0.432 0.410 0.390 0.370 0.352 0.335 0.262 0.207 0.165 0.133 0.088 7 0.425 0.400 0.376 0.354 0.333 0.314 0.296 0.279 0.210 0.159 0.122 0.095 0.059 8 0.376 0.351 0.327 0.305 0.285 0.266 0.249 0.233 0.168 0.123 0.091 0.068 0.039 9 0.333 0.308 0.284 0.263 0.243 0.225 0.209 0.194 0.134 0.094 0.067 0.048 0.026 10 0.295 0.270 0.247 0.227 0.208 0.191 0.176 0.162 0.107 0.073 0.050 0.035 0.017 11 0.261 0.237 0.215 0.195 0.178 0.162 0.148 0.135 0.086 0.056 0.037 0.025 0.012 12 0.231 0.208 0.187 0.168 0.152 0.137 0.124 0.112 0.069 0.043 0.027 0.018 0.008 13 0.204 0.182 0.163 0.145 0.130 0.116 0.104 0.093 0.055 0.033 0.020 0.013 0.005 14 0.181 0.160 0.141 0.125 0.111 0.099 0.088 0.078 0.044 0.025 0.015 0.009 0.003 15 0.160 0.140 0.123 0.108 0.095 0.084 0.074 0.065 0.035 0.020 0.011 0.006 0.002 16 0.141 0.123 0.107 0.093 0.081 0.071 0.062 0.054 0.028 0.015 0.008 0.005 0.002 17 0.125 0.108 0.093 0.080 0.069 0.060 0.052 0.045 0.023 0.012 0.006 0.003 0.001 18 0.111 0.095 0.081 0.069 0.059 0.051 0.044 0.038 0.018 0.009 0.005 0.002 0.001 19 0.098 0.083 0.070 0.060 0.051 0.043 0.037 0.031 0.014 0.007 0.003 0.002 20 0.087 0.073 0.061 0.051 0.043 0.037 0.031 0.026 0.012 0.005 0.002 0.001 25 0.047 0.038 0.030 0.024 0.020 0.016 0.013 0.010 0.004 0.001 0.001 0 30 0.026 0.020 0.015 0.012 0.009 0.007 0.005 0.004 0.001 40 0.008 0.005 0.004 0.003 0.002 0.001 0.001 0.001 0 50 0.002 0.001 0.001 0.001 0 0 0 0 0 000 0 0 0 0 oooooo Table 12-12 Depreciation percentages (expressed in decimals) Depreciation 3-Year 5-Year 7-Year Year MACRS MACRS MACRS 10-Year 15-Year MACRS MACRS 20-Year MACRS 1 ...... 0.333 0.200 0.143 0.100 0.050 0.038 234 2 0.445 0.320 0.245 0.180 0.095 0.072 3 0.148 0.192 0.175 0.144 0.086 0.067 4 0.074 0.115 0.125 0.115 0.077 0.062 6698 5 0.115 0.089 0.092 0.069 0.057 0.058 0.089 0.074 0.062 0.053 7 0.089 0.066 0.059 0.045 0.045 0.066 0.059 0.045 9 10 11 12 13 14 0.065 0.059 0.045 0.065 0.059 0.045 0.033 0.059 0.045 0.059 0.045 0.059 0.045 0.059 0.045 15 16 5 0.059 0.045 0.030 0.045 17 0.045 18 0.045 19 0.045 20 0.045 21 0.017 1.000 1.000 1.000 1.000 1.000 1.000 Table 12-11 Categories for depreciation write-off Class 3-year MACRS 5-year MACRS 7-year MACRS All property with ADR midpoints of four years or less. Autos and light trucks are excluded from this category. Property with ADR midpoints of more than 4, but less than 10 years. Key assets in this category include automobiles, light trucks, and techno- logical equipment such as computers and research-related properties. Property with ADR midpoints of 10 years or more, but less than 16 years. Most types of manufacturing equipment would fall into this category, as would office furniture and fixtures. 10-year MACRS Property with ADR midpoints of 16 years or more, but less than 20 years. Petroleum refining products, railroad tank cars, and manufactured homes fall into this group. 15-year MACRS Property with ADR midpoints of 20 years or more, but less than 25 years. Land improvement, pipeline distribution, telephone distribution, and sewage treatment plants all belong in this category. 20-year MACRS Property with ADR midpoints of 25 years or more (with the exception of real estate, which is treated separately). Key investments in this cat- egory include electric and gas utility property and sewer pipes. Residential rental property if 80% or more of the gross rental income is from nontransient dwelling units (e.g., an apartment building); low- income housing. 27.5-year MACRS 31.5-year MACRS Nonresidential real property that has no ADR class life or whose class life is 27.5 years or more. 39-year MACRS Nonresidential real property placed in service after May 12, 1993.

Expert Answer:

Posted Date:

Students also viewed these finance questions

-

Universal Electronics is considering the purchase of manufacturing equipment with a 10-year midpoint in its asset depreciation range (ADR). Carefully refer to Table 1211 to determine in what...

-

Universal Electronics is considering the purchase of manufacturing equipment with a 10-year midpoint in its asset depreciation range (ADR). Carefully refer to Table 12-11 to determine in what...

-

Starting with the general linear form (16.2.1), verify the interpolation relations (16.2.4) and (16.2.5). Equation 16.2.1 Equation 16.2.4 Equation 16.2.5 u(x,y) = C+Ccx + c3y

-

Assume the United States can produce Toyotas at the cost of $18,000 per car and Chevrolets at $16,000 per car. In Japan, Toyotas can be produced at 1,000,000 yen and Chevrolets at 500,000 yen. a. In...

-

Show that the [4 + 2] Diels-Alder reaction is photochemically forbidden

-

What control procedures should be prescribed and followed for proper custody over assets pertaining to payroll transactions?

-

Kathy Myers frequently purchases stocks and bonds, but she is uncertain how to determine the rate of return that she is earning. For example, three years ago she paid $13,000 for 200 shares of Malti...

-

What is h'(x) when h(x) = log7 8z+4 2672

-

Describe the investment banking process. What is an investment banker? What role do they play in the stages of raising capital? How do they get compensated? What's the role of the investment banker...

-

Some think of organizations as big information systems. According to that idea, the only function and responsibility of a hospitality organization is getting the right information to the right person...

-

Think about a restaurant you go to frequently. The server probably listened to you place your order and then wrote the information down on a pad or entered it into a POS terminal. What decisions and...

-

1. Briefly introduce your selected company and describe the industry. I don't need a history of the company or a discussion of strategies at this stage. This should be no longer than a few...

-

1) Last week, your cafe sold 3,000 cups of coffee. Demand is expected to decrease by 10% for every 5% increase in price. Your current price is $2.80 and you are considering raising your price to...

-

Describe the business and operational challenges facing Bergerac Systems. Should Bergerac Systems integrate backwards into the manufacture of injection-molded parts for its cartridges? What are the...

-

1) Discuss the importance of planning an audit. 2) Explain where 'planning the audit' fits into the audit process.

-

Which internal control principle is especially diffi cult for small organizations to implement? Why?

-

Describe the quick return motion mechanism for a shaper.

-

What is the purpose of a drilling machine ? Explain its working principle.

-

How drilling machines are classified?

Study smarter with the SolutionInn App