Question: Unless otherwise specified you should assume that r(t) and (t) are constant. Answers needed for each part with step by step solution thanks :) With

Unless otherwise specified you should assume that r(t) and (t) are constant.

Answers needed for each part with step by step solution thanks :)

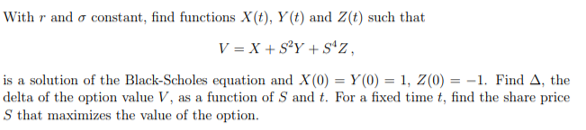

With r and o constant, find functions X(t), y(t) and Z(t) such that V = X + SPY+S4z, is a solution of the Black-Scholes equation and X(0) = Y(0) = 1, 20) = -1. Find A, the delta of the option value V, as a function of S and t. For a fixed time t, find the share price S that maximizes the value of the option. With r and o constant, find functions X(t), y(t) and Z(t) such that V = X + SPY+S4z, is a solution of the Black-Scholes equation and X(0) = Y(0) = 1, 20) = -1. Find A, the delta of the option value V, as a function of S and t. For a fixed time t, find the share price S that maximizes the value of the option

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts