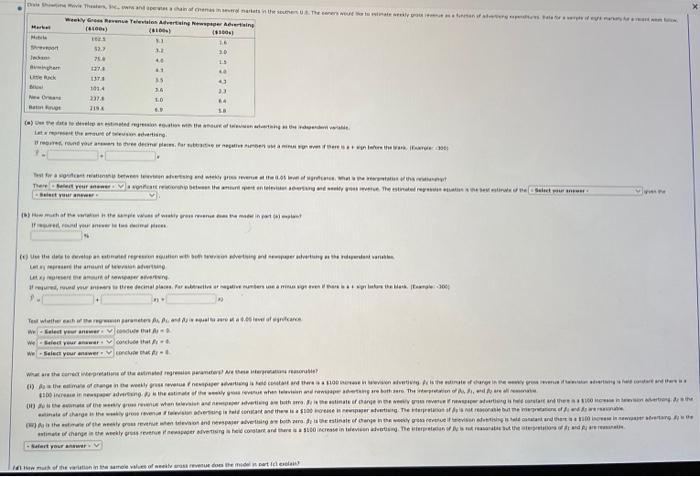

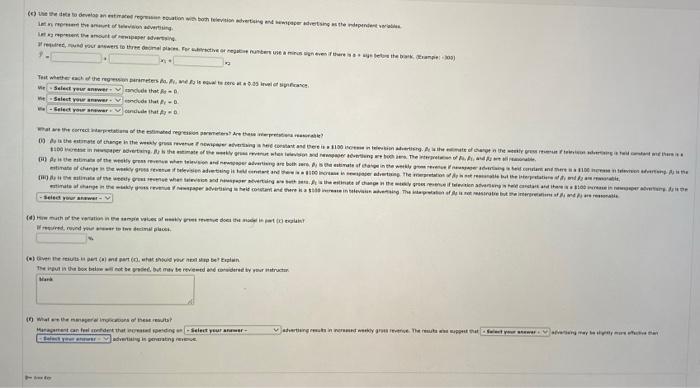

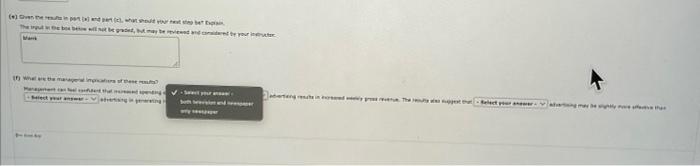

Question: urgent need help on part a-f 1= m) 4) we we w= COSTLT Hat fi =1 corchis reac fu o 4 y= x2=1 Test,whathereach of

1= m) 4) we we w= COSTLT Hat fi =1 corchis reac fu o 4 y= x2=1 Test,whathereach of the reoression parameters 0,1, and 2 is equal to zero at a 0.05 level of significance. What are the correct interpretations of the estimated regression parameters? Are these interpretations reasonable? (i) B0 is the estimate of change in the weekly gross revenue if newspaper advertising is held constant and thern is a tinn inrraasa in talauieinn 1= m) 4) we we w= COSTLT Hat fi =1 corchis reac fu o 4 y= x2=1 Test,whathereach of the reoression parameters 0,1, and 2 is equal to zero at a 0.05 level of significance. What are the correct interpretations of the estimated regression parameters? Are these interpretations reasonable? (i) B0 is the estimate of change in the weekly gross revenue if newspaper advertising is held constant and thern is a tinn inrraasa in talauieinn

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts