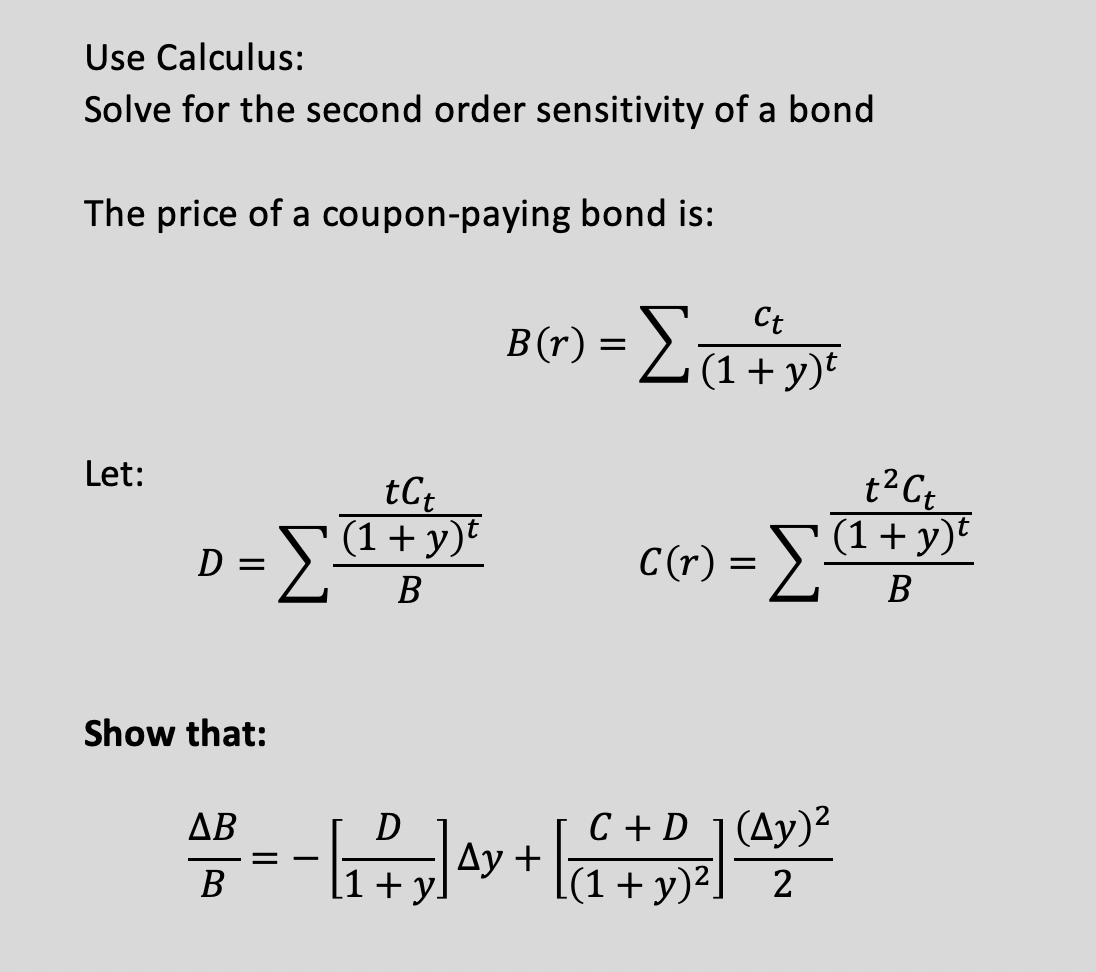

Question: Use Calculus: Solve for the second order sensitivity of a bond The price of a coupon-paying bond is: Let: D: = Show that: tCt

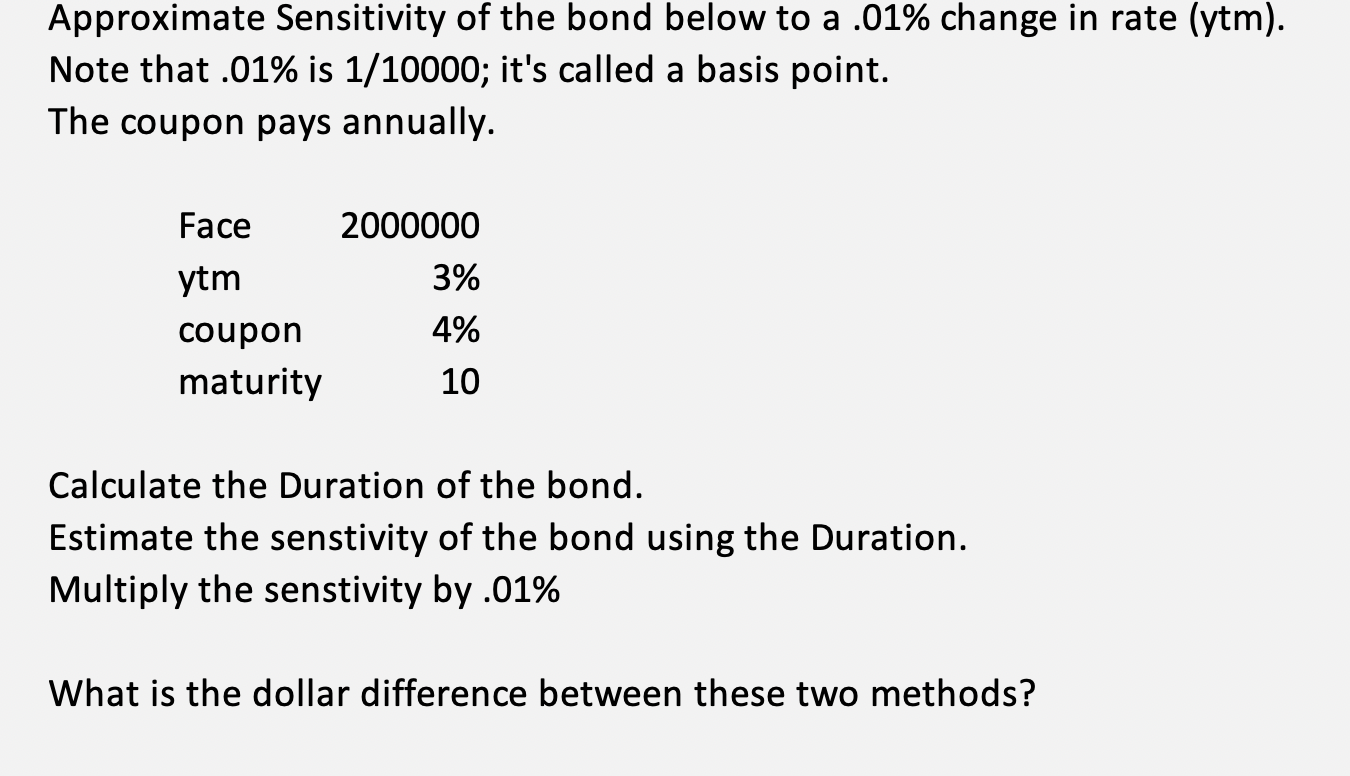

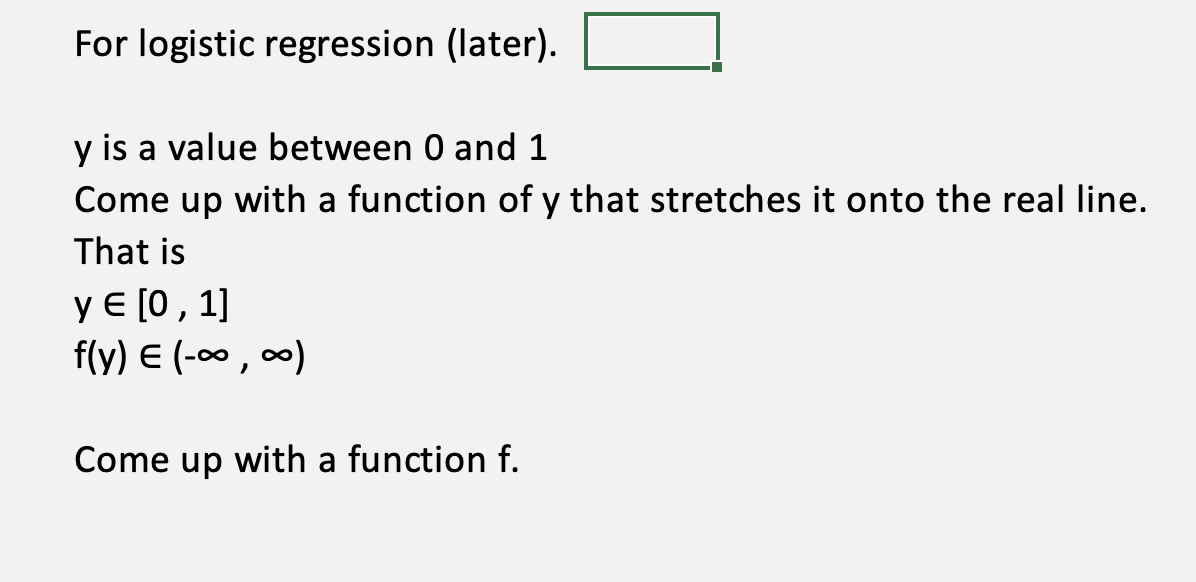

Use Calculus: Solve for the second order sensitivity of a bond The price of a coupon-paying bond is: Let: D: = Show that: tCt (1+ y)t B Ct B(r) = (1 + y)t tCt C (r) = (1 + y) t AB = | Dy | Ay + [ C+D)2] (Ay) - + yl (1 y). 2 B Approximate Sensitivity of the bond below to a .01% change in rate (ytm). Note that .01% is 1/10000; it's called a basis point. The coupon pays annually. Face 2000000 ytm 3% coupon 4% maturity 10 Calculate the Duration of the bond. Estimate the senstivity of the bond using the Duration. Multiply the senstivity by .01% What is the dollar difference between these two methods? For logistic regression (later). y is a value between 0 and 1 Come up with a function of y that stretches it onto the real line. That is y [0, 1] f(y) (-, 0) Come up with a function f.

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts