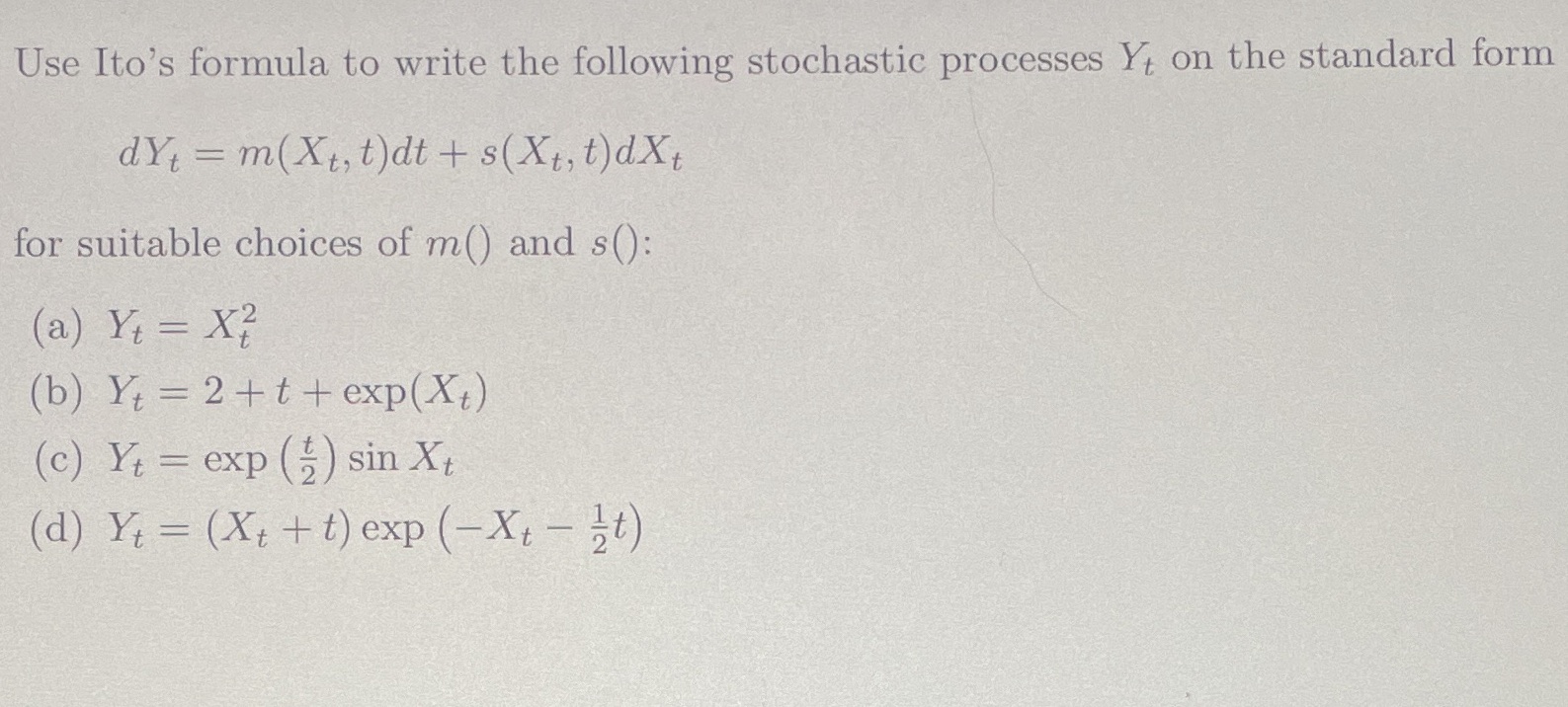

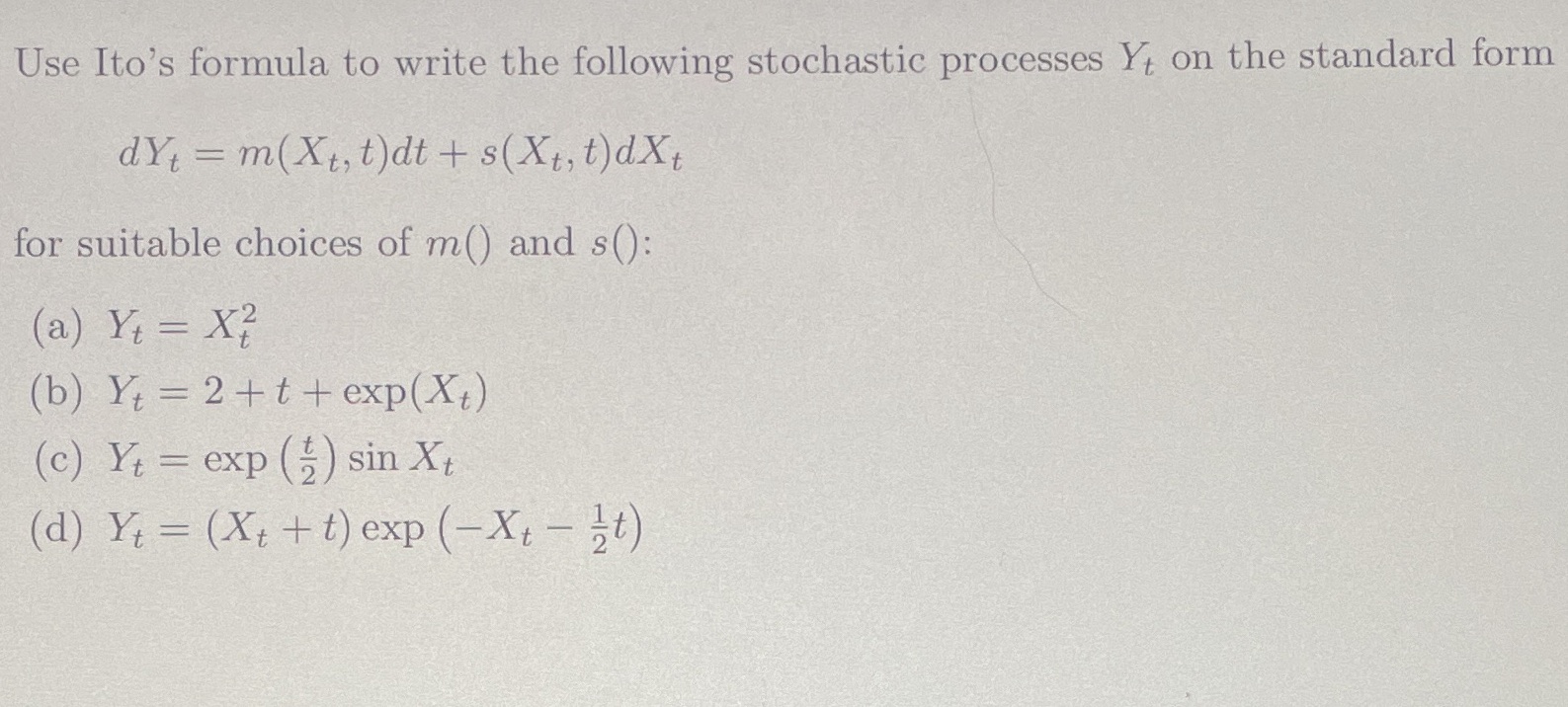

Question: Use Ito's formula to write the following stochastic processes Yt on the standard form dyt = m(Xt, t ) dt + s(Xt, t ) dXt

Use Ito's formula to write the following stochastic processes Yt on the standard form dyt = m(Xt, t ) dt + s(Xt, t ) dXt for suitable choices of m() and s(): (a) Yt = X2 (b) Yt = 2+ t+ exp(Xt) (c) Yt = exp (2) sin Xt (d) Yt = (X+ + t) exp (- Xt - zt)

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock