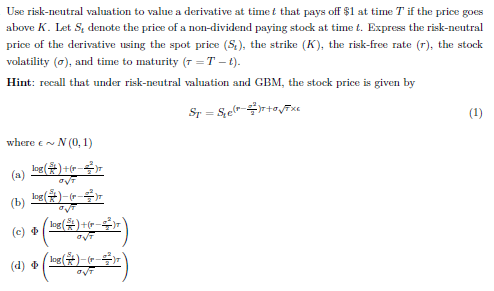

Question: Use risk-neutral valuation to value a derivative at time that pays off $1 at time T if the price goes above K. Let S denote

Use risk-neutral valuation to value a derivative at time that pays off $1 at time T if the price goes above K. Let S denote the price of a non-dividend paying stock at time t. Express the risk-neutral price of the derivative using the spot price (S.), the strike (K), the risk-free rate (r), the stock volatility (), and time to maturity (T=T t). Hint: recall that under risk-neutral valuation and GBM, the stock price is given by S = Sesto Fxe (1) where en (0.1) OVT (a) lng()+(-) ) (b) bel*) (-- > (c) Ing()+(-) (be loc-) (d) OVT (13435) OVT

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock