Question: Use Solver and the information below to find the highest Sharpe ratio portfolio (long-only, no short sales allowed). The riskless rate of 0.3. What is

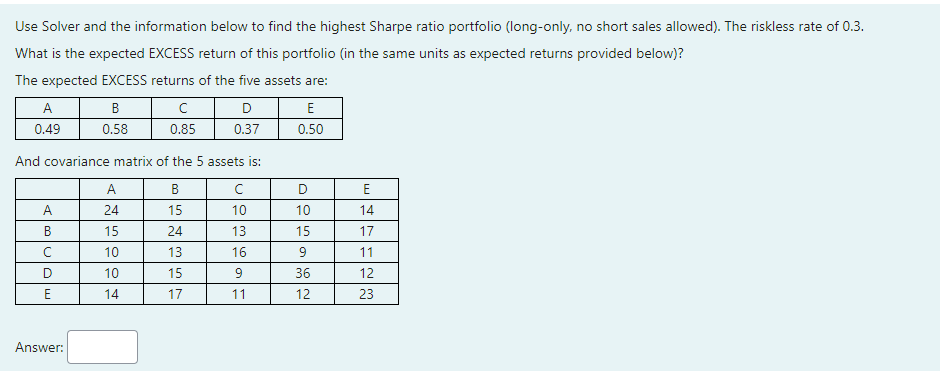

Use Solver and the information below to find the highest Sharpe ratio portfolio (long-only, no short sales allowed). The riskless rate of 0.3. What is the expected EXCESS return of this portfolio (in the same units as expected returns provided below)? The expected EXCESS returns of the five assets are: A B D E 0.49 0.58 0.85 0.37 0.50 And covariance matrix of the 5 assets is: A B D E C 10 A 10 14 B 24 15 10 10 14 15 24 13 15 D 13 16 9 15 9 36 12 17 11 12 23 E E 17 1

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock