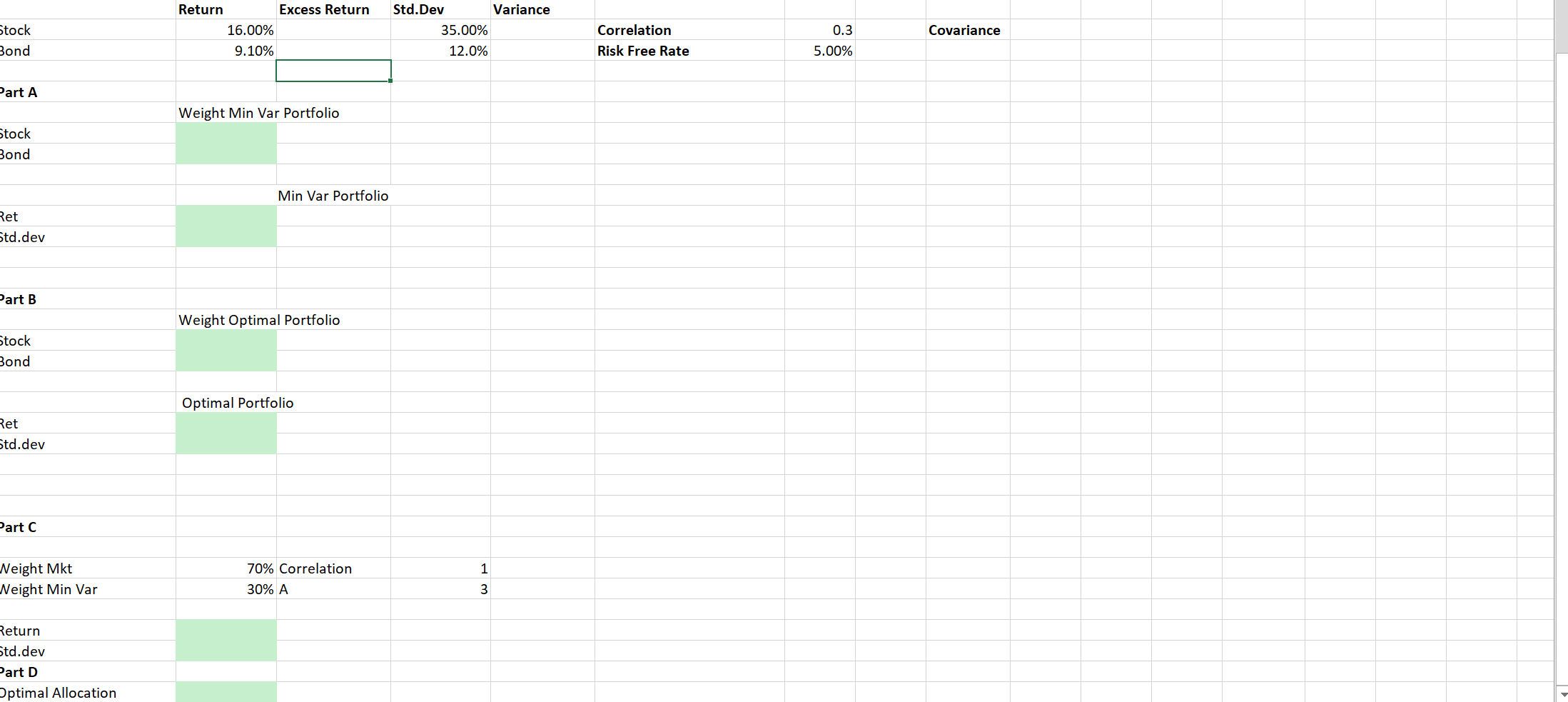

Question: Use the attached spreadsheet to answer the following question and the following information. All data will be given on the sheet. MAKE SURE TO ENTER

Use the attached spreadsheet to answer the following question and the following information. All data will be given on the sheet. MAKE SURE TO ENTER YOUR STUDENT NUMBER IN CELL B2. When uploading your completed file, add you first and last name to the file name. a) What are the weights of the stock and bond fund in the minimum variance portfolio. b) What are the weights of the stock and bond fund in the market portfolio. c) What is the expected return and standard deviation of a portfolio that is invested 70% in the market portfolio and 30% in the minimum variance portfolio, assume they are perfectly positively correlated. d) If an investors risk aversion coefficient is 3, what is their optimal allocation to the market portfolio. Return Excess Return 16.00% 9.10% Std.Dev Variance 35.00% 12.0% Stock Bond 0.3 Covariance Correlation Risk Free Rate 5.00% Part A Weight Min Var Portfolio Stock Bond Min Var Portfolio Ret Std.dev Part B Weight Optimal Portfolio Stock Bond Optimal Portfolio Ret Std.dev Part C 1 Neight Mkt Neight Min Var 70% Correlation 30% A 3 Return Std.dev Part D Optimal Allocation Use the attached spreadsheet to answer the following question and the following information. All data will be given on the sheet. MAKE SURE TO ENTER YOUR STUDENT NUMBER IN CELL B2. When uploading your completed file, add you first and last name to the file name. a) What are the weights of the stock and bond fund in the minimum variance portfolio. b) What are the weights of the stock and bond fund in the market portfolio. c) What is the expected return and standard deviation of a portfolio that is invested 70% in the market portfolio and 30% in the minimum variance portfolio, assume they are perfectly positively correlated. d) If an investors risk aversion coefficient is 3, what is their optimal allocation to the market portfolio. Return Excess Return 16.00% 9.10% Std.Dev Variance 35.00% 12.0% Stock Bond 0.3 Covariance Correlation Risk Free Rate 5.00% Part A Weight Min Var Portfolio Stock Bond Min Var Portfolio Ret Std.dev Part B Weight Optimal Portfolio Stock Bond Optimal Portfolio Ret Std.dev Part C 1 Neight Mkt Neight Min Var 70% Correlation 30% A 3 Return Std.dev Part D Optimal Allocation

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts