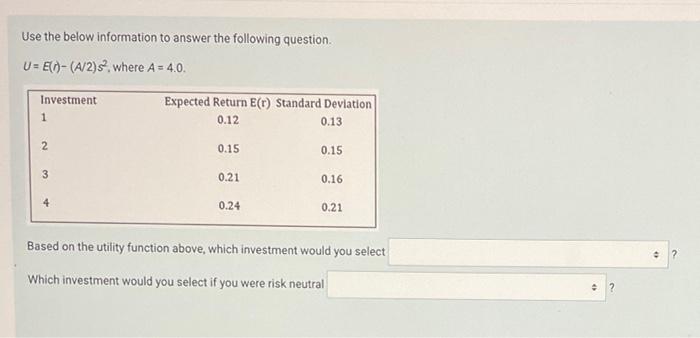

Question: Use the below information to answer the following question. U = E(0)-(A/2)s, where A = 4.0. Investment Expected Return E(r) Standard Deviation 0.12 0.13 1

Use the below information to answer the following question. U = E(0)-(A/2)s", where A = 4.0. Investment Expected Return E(r) Standard Deviation 0.12 0.13 1 2 0.15 0.15 3 0.21 0.16 4 0.24 0.21 Based on the utility function above, which investment would you select : Which investment would you select if you were risk neutral 2

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock