Question: Use the Black Scholes formula to find the value of a European call option based on the following inputs (Do not round Intermediate calculations. Round

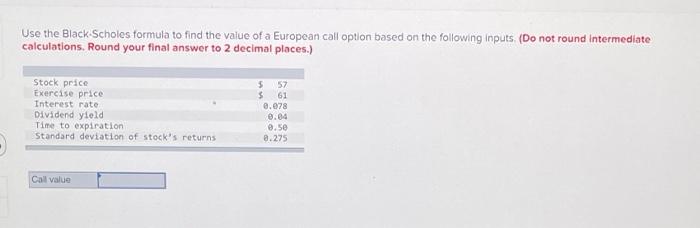

Use the Black Scholes formula to find the value of a European call option based on the following inputs (Do not round Intermediate calculations. Round your final answer to 2 decimal places.) Stock price Exercise price Interest rate Dividend yield Time to expiration Standard deviation of stock's returns $ 57 $ 61 @.078 0.04 8.50 2.275 Call value

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock