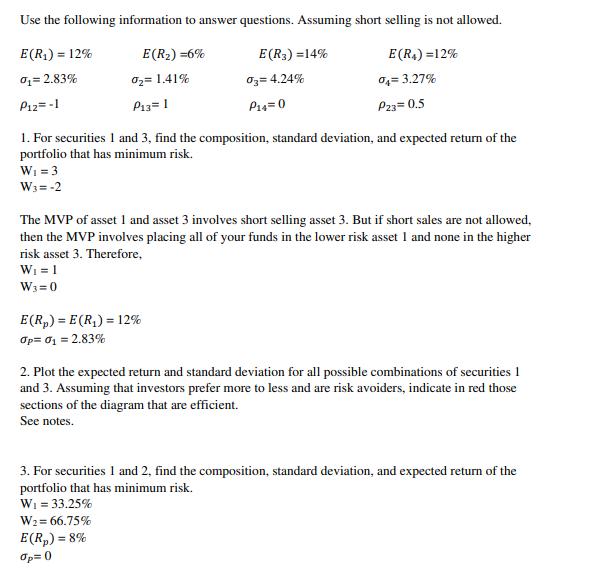

Use the following information to answer questions. Assuming short selling is not allowed. E(R) =6% E...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

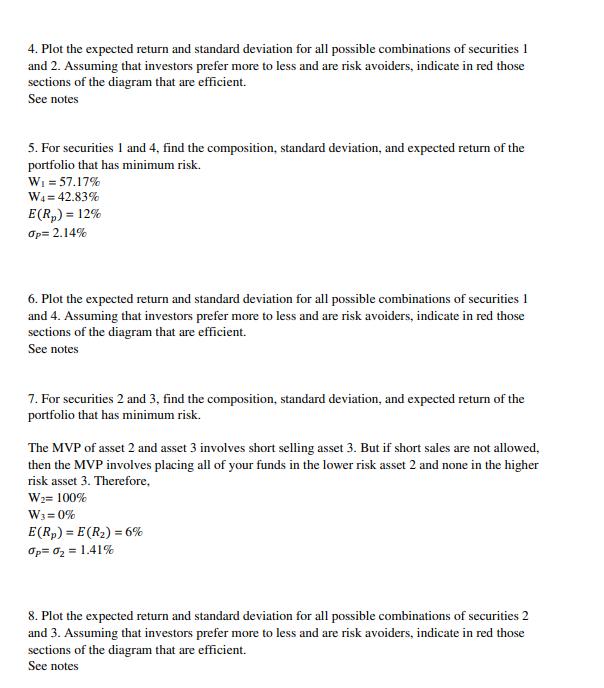

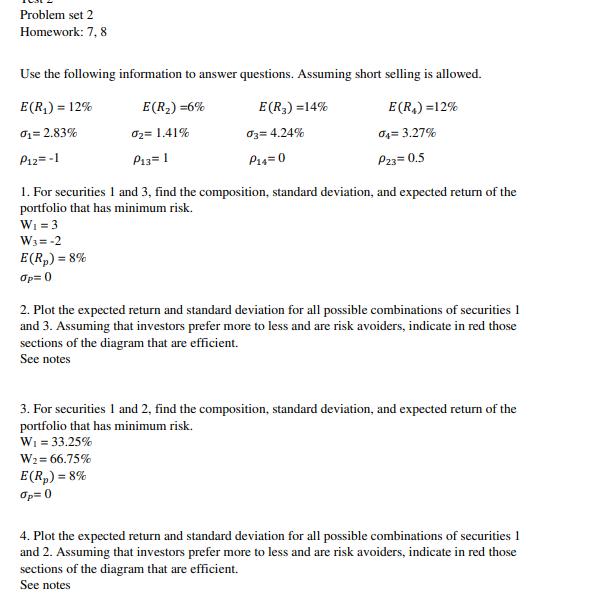

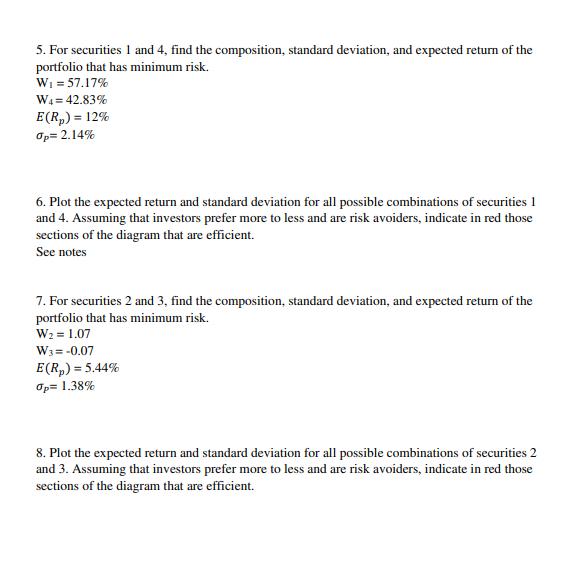

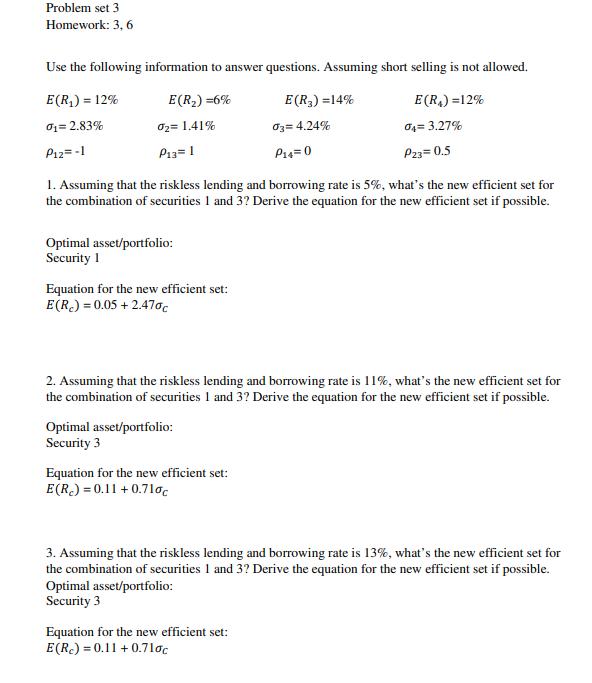

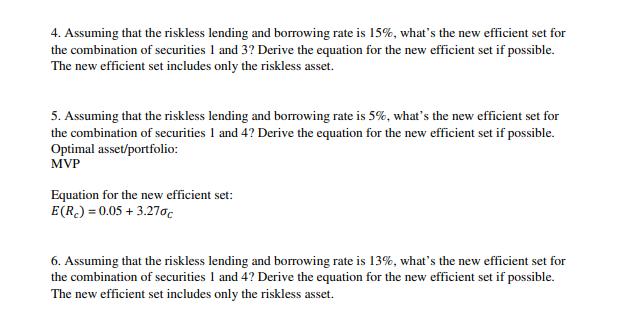

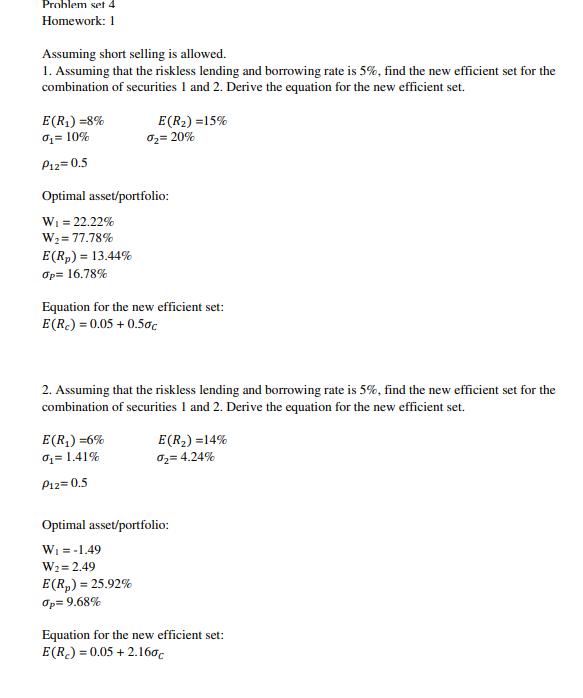

Use the following information to answer questions. Assuming short selling is not allowed. E(R₂) =6% E (R4) =12% E(R₂) = 12% 0₁= 2.83% P12=-1 0₂= 1.41% P13= 1 E (R₂) = 14% 03= 4.24% P14=0 E(R₂) =E(R₂) = 12% Op=0₁ = 2.83% 04= 3.27% P23= 0.5 1. For securities 1 and 3, find the composition, standard deviation, and expected return of the portfolio that has minimum risk. W₁ = 3 W3 = -2 The MVP of asset 1 and asset 3 involves short selling asset 3. But if short sales are not allowed, then the MVP involves placing all of your funds in the lower risk asset 1 and none in the higher risk asset 3. Therefore, W₁ = 1 W₁=0 2. Plot the expected return and standard deviation for all possible combinations of securities 1 and 3. Assuming that investors prefer more to less and are risk avoiders, indicate in red those sections of the diagram that are efficient. See notes. 3. For securities 1 and 2, find the composition, standard deviation, and expected return of the portfolio that has minimum risk. W₁ = 33.25% W₂=66.75% E(R₂) =8% Op=() 4. Plot the expected return and standard deviation for all possible combinations of securities 1 and 2. Assuming that investors prefer more to less and are risk avoiders, indicate in red those sections of the diagram that are efficient. See notes 5. For securities 1 and 4, find the composition, standard deviation, and expected return of the portfolio that has minimum risk. W₁ = 57.17% W4=42.83% E(R₂) = 12% Op= 2.14% 6. Plot the expected return and standard deviation for all possible combinations of securities 1 and 4. Assuming that investors prefer more to less and are risk avoiders, indicate in red those sections of the diagram that are efficient. See notes 7. For securities 2 and 3, find the composition, standard deviation, and expected return of the portfolio that has minimum risk. The MVP of asset 2 and asset 3 involves short selling asset 3. But if short sales are not allowed. then the MVP involves placing all of your funds in the lower risk asset 2 and none in the higher risk asset 3. Therefore, W₂= 100% W3 =0% E(Rp)= E(R₂) = 6% Op=0₂= 1.41% 8. Plot the expected return and standard deviation for all possible combinations of securities 2 and 3. Assuming that investors prefer more to less and are risk avoiders, indicate in red those sections of the diagram that are efficient. See notes Problem set 2 Homework: 7, 8 Use the following information to answer questions. Assuming short selling is allowed. E(R₂) = 12% E(R₂) =6% 01= 2.83% P12 = -1 0₂= 1.41% P13= 1 E(R₂) =14% 03= 4.24% P14 = 0 W₂=66.75% E(Rp) = 8% Op=0) E(R₂) =12% 04= 3.27% P23=0.5 1. For securities 1 and 3, find the composition, standard deviation, and expected return of the portfolio that has minimum risk. W₁ = 3 W3 = -2 E (R₂) =8% Op=0) 2. Plot the expected return and standard deviation for all possible combinations of securities 1 and 3. Assuming that investors prefer more to less and are risk avoiders, indicate in red those sections of the diagram that are efficient. See notes 3. For securities 1 and 2, find the composition, standard deviation, and expected return of the portfolio that has minimum risk. W₁ = 33.25% 4. Plot the expected return and standard deviation for all possible combinations of securities 1 and 2. Assuming that investors prefer more to less and are risk avoiders, indicate in red those sections of the diagram that are efficient. See notes 5. For securities 1 and 4, find the composition, standard deviation, and expected return of the portfolio that has minimum risk. W₁ = 57.17% W4= 42.83% E (R₂) = 12% Op= 2.14% 6. Plot the expected return and standard deviation for all possible combinations of securities 1 and 4. Assuming that investors prefer more to less and are risk avoiders, indicate in red those sections of the diagram that are efficient. See notes 7. For securities 2 and 3, find the composition, standard deviation, and expected return of the portfolio that has minimum risk. W₂ = 1.07 W3 = -0.07 E(R₂) =5.44% Op= 1.38% 8. Plot the expected return and standard deviation for all possible combinations of securities 2 and 3. Assuming that investors prefer more to less and are risk avoiders, indicate in red those sections of the diagram that are efficient. Problem set 3 Homework: 3, 6 Use the following information to answer questions. Assuming short selling is not allowed. E (R₂) = 12% E(R₂) =6% E(R₂) =12% 0₁= 2.83% P12 = -1 0₂= 1.41% P13= 1 Optimal asset/portfolio: Security 1 Equation for the new efficient set: E(R₂) = 0.05 +2.470c 1. Assuming that the riskless lending and borrowing rate is 5%, what's the new efficient set for the combination of securities 1 and 3? Derive the equation for the new efficient set if possible. Optimal asset/portfolio: Security 3 E (R₂) =14% Equation for the new efficient set: E(R)=0.11 +0.71%c 03= 4.24% P14=0 2. Assuming that the riskless lending and borrowing rate is 11%, what's the new efficient set for the combination of securities 1 and 3? Derive the equation for the new efficient set if possible. 04= 3.27% P23=0.5 Equation for the new efficient set: E(R₂) =0.11 +0.710c 3. Assuming that the riskless lending and borrowing rate is 13%, what's the new efficient set for the combination of securities 1 and 3? Derive the equation for the new efficient set if possible. Optimal asset/portfolio: Security 3 4. Assuming that the riskless lending and borrowing rate is 15%, what's the new efficient set for the combination of securities 1 and 3? Derive the equation for the new efficient set if possible. The new efficient set includes only the riskless asset. 5. Assuming that the riskless lending and borrowing rate is 5%, what's the new efficient set for the combination of securities 1 and 4? Derive the equation for the new efficient set if possible. Optimal asset/portfolio: MVP Equation for the new efficient set: E(R₂) = 0.05 + 3.270c 6. Assuming that the riskless lending and borrowing rate is 13%, what's the new efficient set for the combination of securities 1 and 4? Derive the equation for the new efficient set if possible. The new efficient set includes only the riskless asset. Problem set 4 Homework: 1 Assuming short selling is allowed. 1. Assuming that the riskless lending and borrowing rate is 5%, find the new efficient set for the combination of securities 1 and 2. Derive the equation for the new efficient set. E(R₂) =8% 0₁ = 10% P12=0.5 E(R₂) =15% %₂= 20% Optimal asset/portfolio: W₁ = 22.22% W₂=77.78% E(Rp) = 13.44% Op= 16.78% Equation for the new efficient set: E(R) = 0.05 +0.50c E(R₁) =6% %₁ = 1.41% P12=0.5 2. Assuming that the riskless lending and borrowing rate is 5%, find the new efficient set for the combination of securities 1 and 2. Derive the equation for the new efficient set. E(R₂)=14% 0₂=4.24% Optimal asset/portfolio: W₁ = -1.49 W₂=2.49 E(R₂) = 25.92% Op= 9.68% Equation for the new efficient set: E(R)=0.05 +2.160c Use the following information to answer questions. Assuming short selling is not allowed. E(R₂) =6% E (R4) =12% E(R₂) = 12% 0₁= 2.83% P12=-1 0₂= 1.41% P13= 1 E (R₂) = 14% 03= 4.24% P14=0 E(R₂) =E(R₂) = 12% Op=0₁ = 2.83% 04= 3.27% P23= 0.5 1. For securities 1 and 3, find the composition, standard deviation, and expected return of the portfolio that has minimum risk. W₁ = 3 W3 = -2 The MVP of asset 1 and asset 3 involves short selling asset 3. But if short sales are not allowed, then the MVP involves placing all of your funds in the lower risk asset 1 and none in the higher risk asset 3. Therefore, W₁ = 1 W₁=0 2. Plot the expected return and standard deviation for all possible combinations of securities 1 and 3. Assuming that investors prefer more to less and are risk avoiders, indicate in red those sections of the diagram that are efficient. See notes. 3. For securities 1 and 2, find the composition, standard deviation, and expected return of the portfolio that has minimum risk. W₁ = 33.25% W₂=66.75% E(R₂) =8% Op=() 4. Plot the expected return and standard deviation for all possible combinations of securities 1 and 2. Assuming that investors prefer more to less and are risk avoiders, indicate in red those sections of the diagram that are efficient. See notes 5. For securities 1 and 4, find the composition, standard deviation, and expected return of the portfolio that has minimum risk. W₁ = 57.17% W4=42.83% E(R₂) = 12% Op= 2.14% 6. Plot the expected return and standard deviation for all possible combinations of securities 1 and 4. Assuming that investors prefer more to less and are risk avoiders, indicate in red those sections of the diagram that are efficient. See notes 7. For securities 2 and 3, find the composition, standard deviation, and expected return of the portfolio that has minimum risk. The MVP of asset 2 and asset 3 involves short selling asset 3. But if short sales are not allowed. then the MVP involves placing all of your funds in the lower risk asset 2 and none in the higher risk asset 3. Therefore, W₂= 100% W3 =0% E(Rp)= E(R₂) = 6% Op=0₂= 1.41% 8. Plot the expected return and standard deviation for all possible combinations of securities 2 and 3. Assuming that investors prefer more to less and are risk avoiders, indicate in red those sections of the diagram that are efficient. See notes Problem set 2 Homework: 7, 8 Use the following information to answer questions. Assuming short selling is allowed. E(R₂) = 12% E(R₂) =6% 01= 2.83% P12 = -1 0₂= 1.41% P13= 1 E(R₂) =14% 03= 4.24% P14 = 0 W₂=66.75% E(Rp) = 8% Op=0) E(R₂) =12% 04= 3.27% P23=0.5 1. For securities 1 and 3, find the composition, standard deviation, and expected return of the portfolio that has minimum risk. W₁ = 3 W3 = -2 E (R₂) =8% Op=0) 2. Plot the expected return and standard deviation for all possible combinations of securities 1 and 3. Assuming that investors prefer more to less and are risk avoiders, indicate in red those sections of the diagram that are efficient. See notes 3. For securities 1 and 2, find the composition, standard deviation, and expected return of the portfolio that has minimum risk. W₁ = 33.25% 4. Plot the expected return and standard deviation for all possible combinations of securities 1 and 2. Assuming that investors prefer more to less and are risk avoiders, indicate in red those sections of the diagram that are efficient. See notes 5. For securities 1 and 4, find the composition, standard deviation, and expected return of the portfolio that has minimum risk. W₁ = 57.17% W4= 42.83% E (R₂) = 12% Op= 2.14% 6. Plot the expected return and standard deviation for all possible combinations of securities 1 and 4. Assuming that investors prefer more to less and are risk avoiders, indicate in red those sections of the diagram that are efficient. See notes 7. For securities 2 and 3, find the composition, standard deviation, and expected return of the portfolio that has minimum risk. W₂ = 1.07 W3 = -0.07 E(R₂) =5.44% Op= 1.38% 8. Plot the expected return and standard deviation for all possible combinations of securities 2 and 3. Assuming that investors prefer more to less and are risk avoiders, indicate in red those sections of the diagram that are efficient. Problem set 3 Homework: 3, 6 Use the following information to answer questions. Assuming short selling is not allowed. E (R₂) = 12% E(R₂) =6% E(R₂) =12% 0₁= 2.83% P12 = -1 0₂= 1.41% P13= 1 Optimal asset/portfolio: Security 1 Equation for the new efficient set: E(R₂) = 0.05 +2.470c 1. Assuming that the riskless lending and borrowing rate is 5%, what's the new efficient set for the combination of securities 1 and 3? Derive the equation for the new efficient set if possible. Optimal asset/portfolio: Security 3 E (R₂) =14% Equation for the new efficient set: E(R)=0.11 +0.71%c 03= 4.24% P14=0 2. Assuming that the riskless lending and borrowing rate is 11%, what's the new efficient set for the combination of securities 1 and 3? Derive the equation for the new efficient set if possible. 04= 3.27% P23=0.5 Equation for the new efficient set: E(R₂) =0.11 +0.710c 3. Assuming that the riskless lending and borrowing rate is 13%, what's the new efficient set for the combination of securities 1 and 3? Derive the equation for the new efficient set if possible. Optimal asset/portfolio: Security 3 4. Assuming that the riskless lending and borrowing rate is 15%, what's the new efficient set for the combination of securities 1 and 3? Derive the equation for the new efficient set if possible. The new efficient set includes only the riskless asset. 5. Assuming that the riskless lending and borrowing rate is 5%, what's the new efficient set for the combination of securities 1 and 4? Derive the equation for the new efficient set if possible. Optimal asset/portfolio: MVP Equation for the new efficient set: E(R₂) = 0.05 + 3.270c 6. Assuming that the riskless lending and borrowing rate is 13%, what's the new efficient set for the combination of securities 1 and 4? Derive the equation for the new efficient set if possible. The new efficient set includes only the riskless asset. Problem set 4 Homework: 1 Assuming short selling is allowed. 1. Assuming that the riskless lending and borrowing rate is 5%, find the new efficient set for the combination of securities 1 and 2. Derive the equation for the new efficient set. E(R₂) =8% 0₁ = 10% P12=0.5 E(R₂) =15% %₂= 20% Optimal asset/portfolio: W₁ = 22.22% W₂=77.78% E(Rp) = 13.44% Op= 16.78% Equation for the new efficient set: E(R) = 0.05 +0.50c E(R₁) =6% %₁ = 1.41% P12=0.5 2. Assuming that the riskless lending and borrowing rate is 5%, find the new efficient set for the combination of securities 1 and 2. Derive the equation for the new efficient set. E(R₂)=14% 0₂=4.24% Optimal asset/portfolio: W₁ = -1.49 W₂=2.49 E(R₂) = 25.92% Op= 9.68% Equation for the new efficient set: E(R)=0.05 +2.160c

Expert Answer:

Related Book For

Advanced Accounting

ISBN: 978-1934319307

2nd edition

Authors: Susan S. Hamlen, Ronald J. Huefner, James A. Largay III

Posted Date:

Students also viewed these mathematics questions

-

4 pts USE THE FOLLOWING INFORMATION TO ANSWER QUESTIONS 1 THROUGH 3 A clothing manufacturer monitors the cutting and sewing stage of its men's long-sleeve shirt production process by using mean and...

-

Return to the example presented in Problem 1, Chapter 4. A. Assuming short selling is not allowed: (1) For securities 1 and 2, find the composition, standard deviation, and expected return of the...

-

Use the following information to answer questions 4344 below. lamlen, C MC On November 15, 2016, a US. oompany ssues purchase order to Caadian wel merchandise costing CS1.000,000, On the same date,...

-

The preparation of an organization's budget: a. forces management to look ahead and try to see the future of the organization. b. requires that the entire management team work together to make and...

-

Tannhauser Financial is a banking services company that offers many different types of checking accounts. It has recently adopted an activity-based costing system to assign costs to various types of...

-

DS 16.3.2 contains the sample means i and the sample ranges ri of a variable measurement based upon samples of size n = 5, which are collected at k = 25 points in time. (a) Use this data set to...

-

Great Wall Chinese Cuisine had \($93,000\) of total assets and \($31,000\) of total stock holders equity at May 31,2010. At May 31, 2011, Great Wall Chinese Cuisine had assets totaling \($147,000\)...

-

A company has the following data: net sales, $202,500; cost of goods sold, $110,000; selling expenses, $45,000; general and administrative expense, $30,000; interest expense, $2,000; and interest...

-

A yen futures contract settles one year from today. If spot yen is 97, the one year yen interest rate is 1% and the one year US interest rate is 3%, estimate the futures price you should find on the...

-

Refer to Exercise 4. Find the mean of X. Interpret this value. Exercise 4. Ana is a dedicated Skee Ball player (see photo) who always rolls for the 50-point slot. The probability distribution of Anas...

-

Read the case namely Colman Art Museum. Write a case memo in which you address the following: Introduction overview includes (background, competition, target market, and market mix) SWOT analysis...

-

The Green Chef is an exclusive restaurant in your city. Reservations are difficult to secure and the menu is expensive. The owner, Chef Jorge, is rumored to be running an illegal gambling operation...

-

GDP exceeds NDP by an amount equal to? Explain

-

A not-for-profit hospital reported in 2021 income statement: Revenue 150m Expenses 110m Net Income 40m On their 2021 Statement of Changes in Net Assets they reported: Beginning Net Assets of 110m...

-

What value propositions is ChatGPT a substitute for? What do you think so provide your thoughts?

-

How fast is a 1.5 kg ball traveling when it hits the ground 3.5 meters below its original position, given it starts from rest? Assume zero drag.

-

You set a goal to complete a home renovation project by the end of the month. Which measurement strategy will best help you track and achieve your goal? a.) Survey your friends who have done home...

-

Explain the term global capital markets. This chapter primarily discusses global equity markets. What other types of financial instruments are traded in these markets? How important are global...

-

Northrop Grumman, a global defense contractor and aircraft manufacturer headquartered in Los Angeles, CA, acquired Essex Corporation on January 25, 2007, for $590 million in cash, including...

-

Your accounting firm audits the financial statements of the Sioux Falls Society for the Preservation of Prairie Dogs, a private not-for-profit organization. Your job is to review the format of the...

-

Olean County uses the following capital projects funds for acquisition or construction of capital facilities: Total balances for governmental, enterprise, internal service, and fiduciary funds are:...

-

a. Nonlinearity in mass b. Nonlinearity in damping c. Linear equation d. Nonlinearity in spring \(\ddot{x}+f \frac{\dot{x}}{|\dot{x}|}+\omega_{n}^{2} x=0\)

-

The equation of motion of a nonlinear system is given by \[\ddot{x}+c \dot{x}+k_{1} x+k_{2} x^{2}=a \cos 2 \omega t\] Investigate the subharmonic solution of order 2 for this system.

-

Prove that, for the system considered in Section 13.5.1, the minimum value of \(\omega^{2}\) for which the amplitude of subharmonic oscillations \(A\) will have a real value is given by...

Study smarter with the SolutionInn App