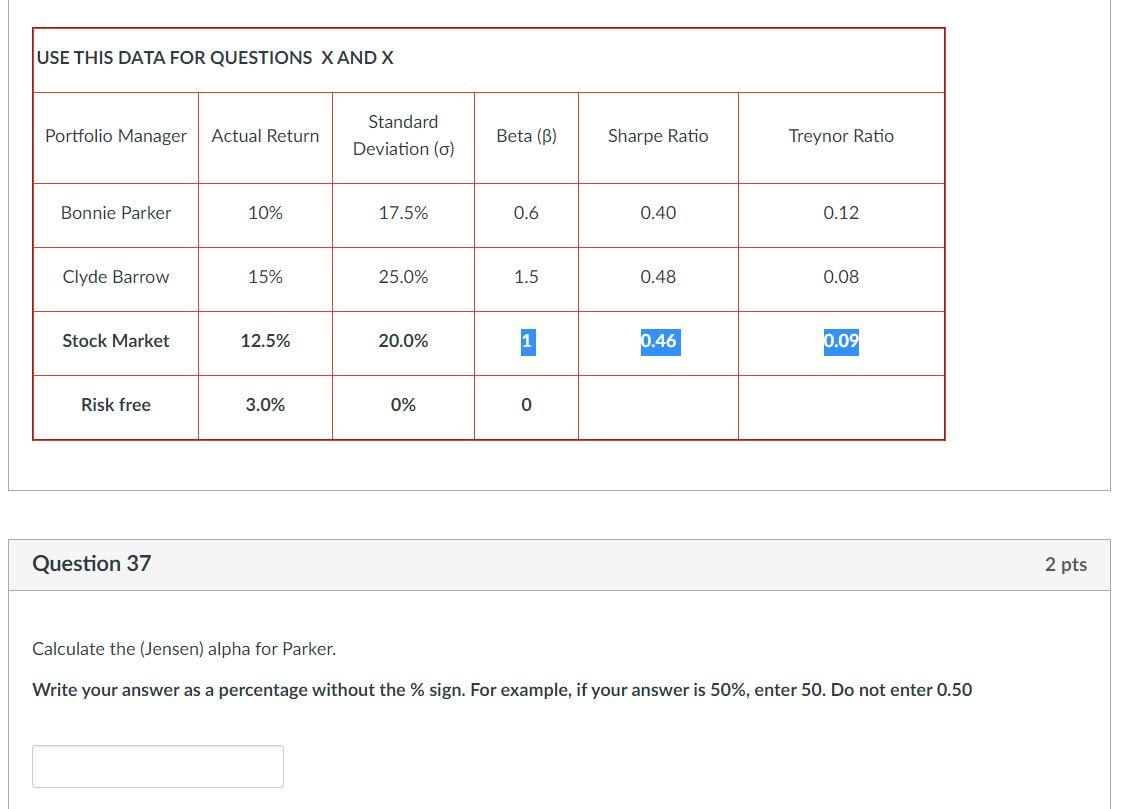

Question: USE THIS DATA FOR QUESTIONS X AND X Portfolio Manager Actual Return Standard Deviation (0) Beta (B) Sharpe Ratio Treynor Ratio Bonnie Parker 10% 17.5%

USE THIS DATA FOR QUESTIONS X AND X Portfolio Manager Actual Return Standard Deviation (0) Beta (B) Sharpe Ratio Treynor Ratio Bonnie Parker 10% 17.5% 0.6 0.40 0.12 Clyde Barrow 15% 25.0% 1.5 0.48 0.08 Stock Market 12.5% 20.0% 0.46 0.09 Risk free 3.0% 0% 0 Question 37 2 pts Calculate the (Jensen) alpha for Parker. Write your answer as a percentage without the % sign. For example, if your answer is 50%, enter 50. Do not enter 0.50

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock