A-One Chicken grows and processes chickens. Each chicken is disassembled into five main parts. A-OneChicken is computing

Question:

A-One Chicken grows and processes chickens. Each chicken is disassembled into five main parts.

A-OneChicken is computing the ending inventory values for its July 31,2014,

statement of financial position. Ending inventory amounts on July 31 are 15 kilograms of breasts,

4 kilograms of wings,7kilograms of thighs,9kilograms of bones, and 2 kilograms of feathers. A-One Chicken's management wants to use the sales value at splitoff method. However, it wants you to explore the effect on ending inventory values of classifying one or more products as a byproduct rather than a joint product.

Requirement 1. Assume

A-One

Chicken classifies all five products as joint products. What are the ending inventory values of each product on July 31,

2014?

(Round your answers to the nearest cent. Enter an amount for each product, including zero balances.)

Product | Ending Inventory Value |

Breasts | |

Wings | |

Thighs | |

Bones | |

Feathers | |

Total |

Requirement 2. Assume

A-One

Chicken uses the production method of accounting for byproducts. What are the ending inventory values for each joint product on July 31,

2014,

assuming breasts and thighs are the joint products and wings, bones, and feathers are byproducts?

Begin by selecting the formula to calculate the joint costs to be allocated. Then enter the amounts and determine the amount.(NRV = Net realizable value. Round all amounts to the nearest cent.)

- | = | Joint costs to be allocated |

- | = |

Now use the table below to calculate the allocated costs per kilogram for the breasts and thighs. (Round the weights to three decimal places, the joint costs to the nearest cent, and the allocated costs per kilogram to four decimal places.)

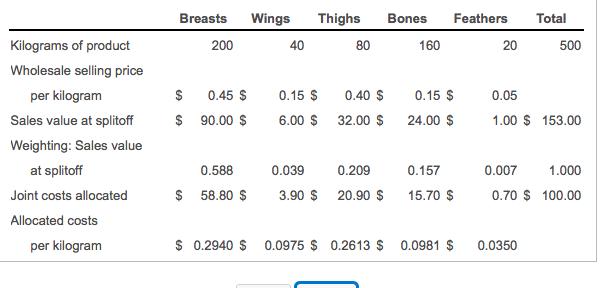

Breasts | Thighs | Total | |

Kilograms of product | 200 | 80 | |

Wholesale selling price | |||

per kilogram | $0.45 | $0.40 | |

Sales value at splitoff | $90.00 | $32.00 | |

Weighting: Sales value | |||

at splitoff | |||

Joint costs allocated | |||

Allocated costs | |||

per kilogram |

What are the ending inventory values for each joint product on July 31,

2014,

assuming breasts and thighs are the joint products and wings, bones, and feathers arebyproducts? (Round all amounts to the nearest cent. Enter an amount for each product, including zero balances.)

Product | Ending Inventory Value |

Breasts | |

Wings | |

Thighs | |

Bones | |

Feathers | |

Total |

Requirement 3. Comment on differences in the results in requirements 1 and 2.

A.

In requirement 1, each product is allocated joint costs since each product is a joint product. In requirement 2, only breasts and thighs are allocated joint costs since the remaining products are byproducts.

B.

Requirements 1 and 2 result in the same ending inventory value since there is no difference in allocating costs when there are byproducts.

C.

In requirement 1, joint costs are allocated to only the most profitable joint products. In requirement 2, all products, including byproducts, are allocated joint costs.

D.

None of the above is true.

Expert Answer:

Financial Accounting an introduction to concepts, methods and uses

ISBN: 978-0324789003

13th Edition

Authors: Clyde P. Stickney, Roman L. Weil, Katherine Schipper, Jennifer Francis