Question: Using a discrete time model (t = 0, 1, 2, 3, ...,T), compute the yield, duration and modified duration of the following two bonds. Name

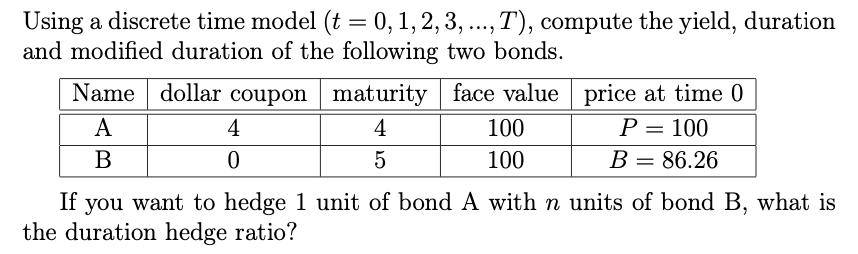

Using a discrete time model (t = 0, 1, 2, 3, ...,T), compute the yield, duration and modified duration of the following two bonds. Name dollar coupon maturity face value price at time 0 A 4 4 100 P= 100 B 0 5 100 B= 86.26 If you want to hedge 1 unit of bond A with n units of bond B, what is the duration hedge ratio? Using a discrete time model (t = 0, 1, 2, 3, ...,T), compute the yield, duration and modified duration of the following two bonds. Name dollar coupon maturity face value price at time 0 A 4 4 100 P= 100 B 0 5 100 B= 86.26 If you want to hedge 1 unit of bond A with n units of bond B, what is the duration hedge ratio

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts