Question: Using a discrete time model (t = 0, 1, 2, 3, ..., T) with the following zero coupon bond prices at time t = 1/2.

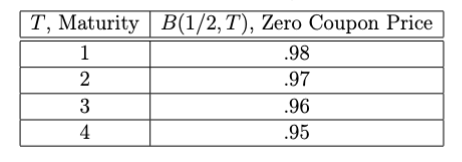

Using a discrete time model (t = 0, 1, 2, 3, ..., T) with the following zero coupon bond prices at time t = 1/2.

The spot rate at time 0 was R(0) = .01. The swap rate at time 0 was i = .02. Consider a 4 year plain vanilla interest rate swap created at time t = 0 with a floating rate equal to the default free spot rate and a notional of $100. What is the value of the swap at time t = 1/2?

T, Maturity B(1/2, T), Zero Coupon Price 1 .98 2 .97 3 .96 4 .95

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock