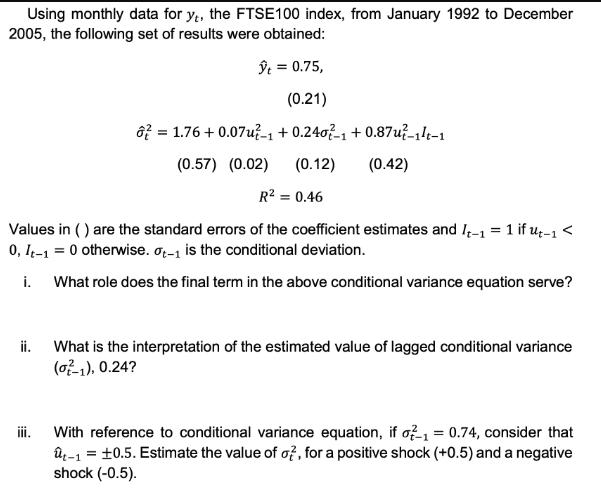

Question: Using monthly data for yt, the FTSE100 index, from January 1992 to December 2005, the following set of results were obtained: t = 0.75,

Using monthly data for yt, the FTSE100 index, from January 1992 to December 2005, the following set of results were obtained: t = 0.75, (0.21) 62 = 1.76 +0.07u-1 +0.2402-1 +0.87u-14-1 (0.57) (0.02) (0.12) (0.42) R = 0.46 Values in () are the standard errors of the coefficient estimates and It-1 = 1 if ut-1 < 0, It-1 = 0 otherwise. Ot-1 is the conditional deviation. i. What role does the final term in the above conditional variance equation serve? ii. What is the interpretation of the estimated value of lagged conditional variance (0-1), 0.24? With reference to conditional variance equation, if oz- = 0.74, consider that t-1 +0.5. Estimate the value of of, for a positive shock (+0.5) and a negative shock (-0.5). =

Step by Step Solution

3.39 Rating (161 Votes )

There are 3 Steps involved in it

The final term in the conditional variance equation serves as a threshold indicator It is denoted as ... View full answer

Get step-by-step solutions from verified subject matter experts