Question: Using publicly available information and assigned the role as lead investigator, you are required to answer a number of questions and advise as to the

Using publicly available information and assigned the role as "lead investigator", you are required to answer a number of questions and advise as to the proper allocation of "blame" in the situation.

The company I have chosen is called Tesco PLC. I have done introduction, part a and b so far.

Please give a great explanation to part e ONLY (preferably include the chart as well), "Compile a timeline of events in the company's history from six months prior to the news release of the fraud/earnings management until six months subsequent to the news release (consider using sedar.com for Canadian companies and edgar for U.S. companies). Next, chart the significant fluctuations in the company's share price during this same period (consider using Google Finance to obtain this chart). Did all the news releases correspond to a significant change in share price? Did all the significant share price changes correspond with a news event? Based on your observations, do you think the market is efficient? Why/why not?"

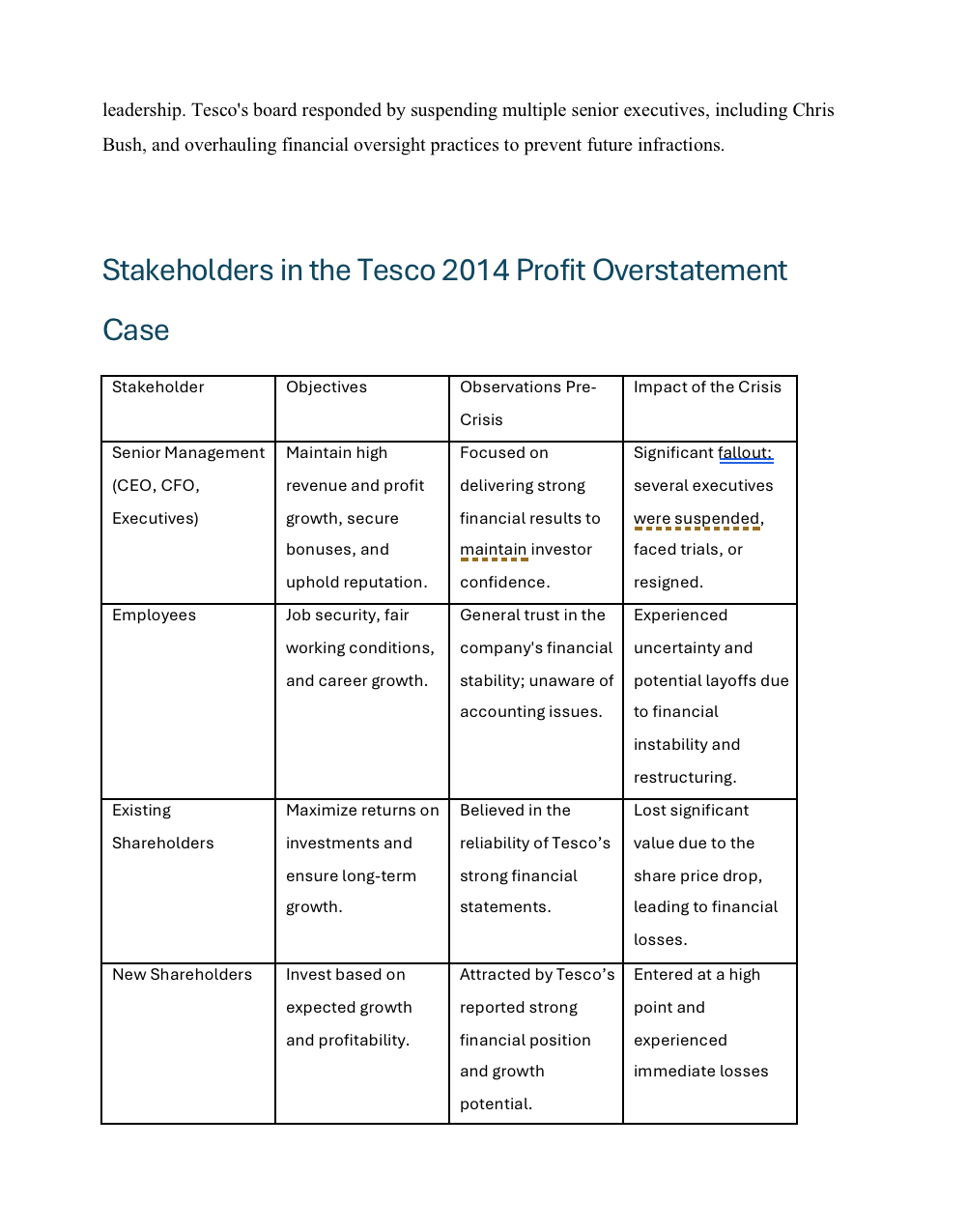

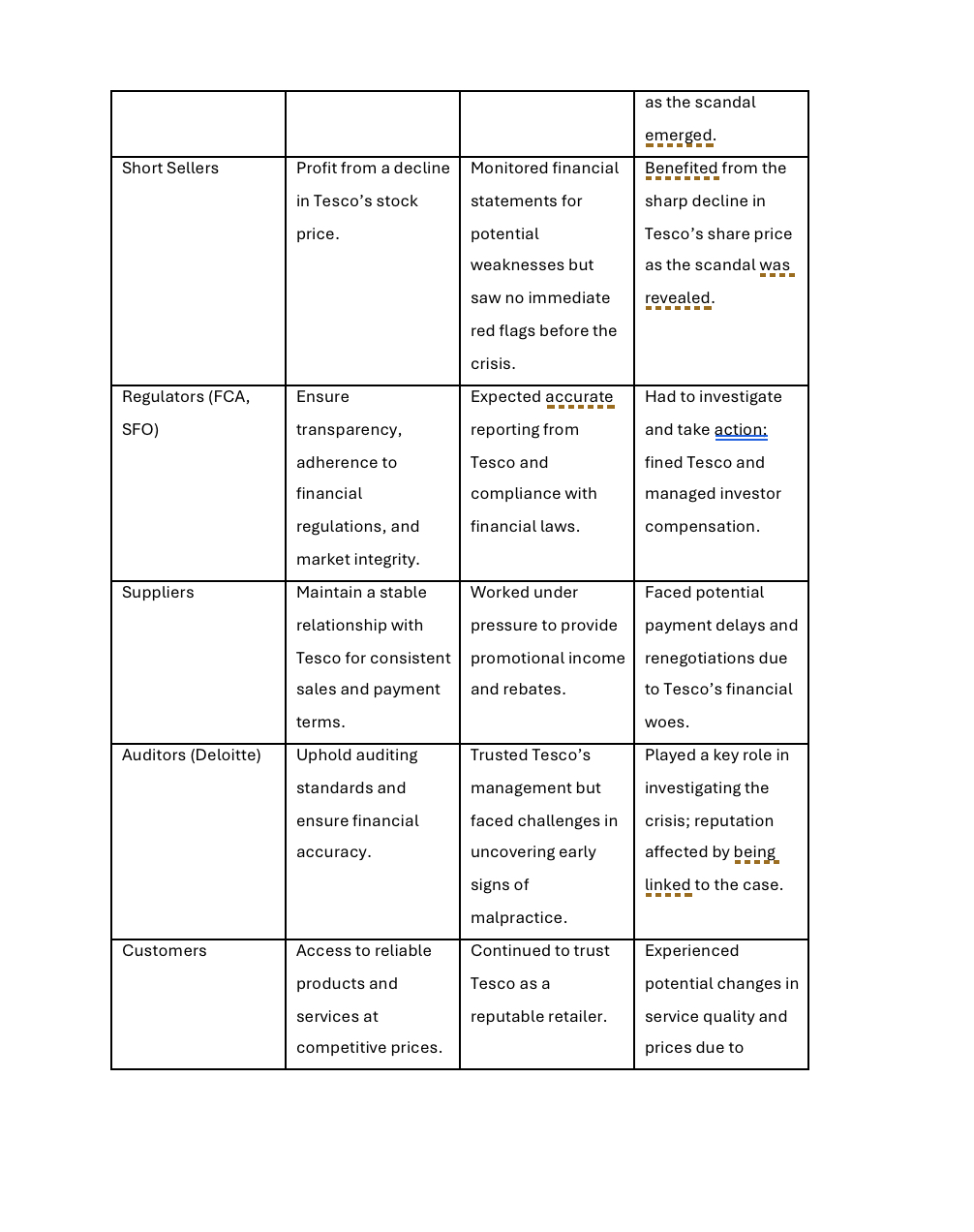

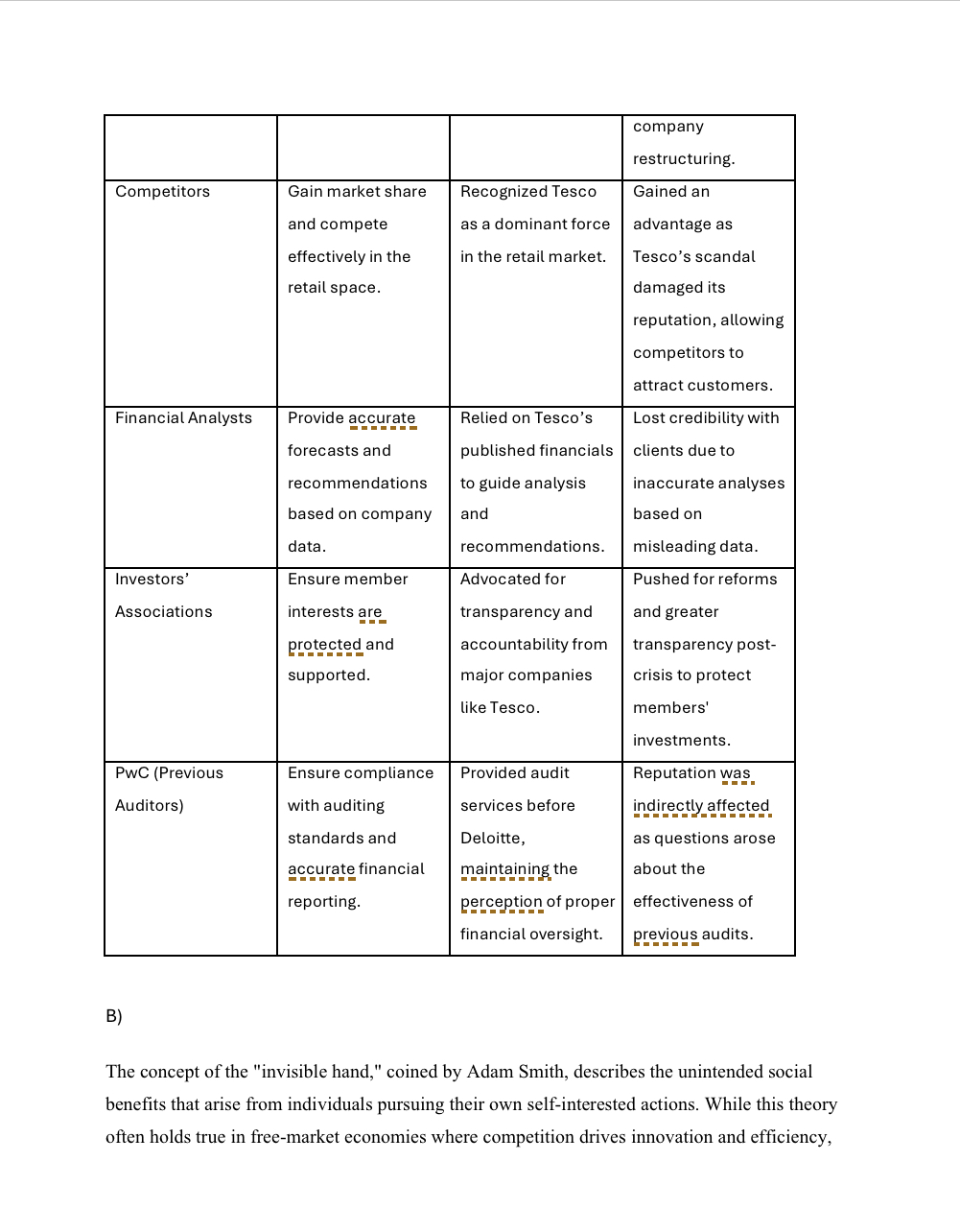

Written Assignment The written portion of the assignment should be a maximum of 15 pages, Times New Roman 12 point font, 1.5 line spacing, excluding tables. Tables can take a maximum of an additional 5 pages. It should include the following details: 1. Introduction provide a summary of the case, including company background, the key \"players\" i.e. CEO/CFO, etc., synopsis of the issue (fraud/earnings management), and the conclusion i.e. jail time/monetary fine, etc. The introduction should be between 1.5 to 2 pages. 2. Body please ensure you address each of the following items (you can include other considerations as well): (7 7 a.ldentify all the stakeholders in the story i.e. employees, senior management, existing shareholders, new shareholders, short sellers, OSC/SEC, other regulators, etc. In a table, list these stakeholders, including their respective objectives and observations pre-crisis. Complete the table by identifying how each of the stakeholders was affected by the crisis. 5 } b. The \"invisible hand\" is a term that was coined by Adam Smith to describe the unintended social benefits of individual self-interested actions. In the context of the company assigned, would you agree or disagree with this statement? Provide robust reasons from your assigned company to support your position. 4;_;:/ c. CSR (corporate social responsibility) is a hot topic. CSR, broadly speaking, ? consists of the following considerations: 1) jal; and 3) corporate governance. Describe the company's CSR policies at the time of the incident. Do you think poor CSR contributed to the incidence of fraud/earnings management? What corrective actions, if any, did the company make after the Sy incident? d. In the aftermath of the disclosure of the fraud/earnings management, how did fmuol financial analysts respond? i.e. changes in earnings/price forecasts. Try to find out announcement which institutions were buyers/sellers of the company's stock at this time. d nte Comment as to how different institutions, each with access to the same information, have such different viewpoints as to the investment thesis for this stock. e. Compile a timeline of events in the company's history from six months prior to the 29/, news release of the fraud/earnings management until six months subsequent to the news release (consider using sedar.com for Canadian companies and edgar for U.S. companies). Next, chart the significant fluctuations in the company's share price during this same period (consider using Google Finance to obtain this chart). Do all the news releases correspond to a significant change in share price? Do all the significant share price changes correspond with a news event? Based on your observations, do you think the market is efficient? Why/why not? 3. Conclusion provide a summary of the case, including a discussion as to your allocation of blame amongst the various stakeholders. Is your allocation of blame consistent with your initial thoughts? Do you think the media provided a fair portrayal of the allocation of blame? What are some of the \"big picture\" reflections you have learned from completing fhis projcet? Introduction Tesco PLC, a British multinational grocery and general merchandise retailer, has long been a household name and one of the largest retailers in the world. Founded in 1919 by Jack Cohen, Tesco expanded rapidly over the decades to gstablish itself as a market leader in the UK and abroad, offering a wide range of products and services. By the early 2010s, it was an essential part of the UK's retail landscape, boasting an extensive network of stores and a significant online presence. However, its reputable image was severely tarnished in 2014 by an accounting scandal that highlighted critical failings in financial governance and corporate oversight. At the center of this crisis were key figures within Tesco's leadership. The company was led by Philip Clarke, who served as CEO until July 2014 when Dave Lewis succeeded him. The Chief Financial Officer (CFO) at the time was Laurie Mcllwee, who had stepped down earlier in 2014 but remained associated with the financial operations during the period in question. Several other senior executives, including Chris Bush, the UK Managing Director, played pivotal roles and were scrutinized during the investigation. The core of the issue revolved around earnings management through the manipulation of commercial income. Specifically, Tesco had overstated its expected profits by approximately 250 million. This misstatement was attributed to improper recognition of supplier income Tesco booked revenue from supplier rebates and promotional payments prematurely while deferring the recognition of related costs. The practice painted an inflated picture of Tesco's financial health, deceiving investors and analysts who relied on these reports for an accurate assessment of the company's performance. The irregularities came to_light in September 2014, just weeks after Dave Lewis took over as CEO. Following the discovery, Tesco promptly launched an internal investigation led by Deloitte, an external auditor, alongside legal advisers from Freshfields Bruckhaus Deringer. The matter caught the attention of the Financial Conduct Authority (FCA) and later the Serious Fraud Office (SFQ), which began their own in-depth inquiries into potential misconduct. The scandal had profound consequences. Tesco's shares plummeted, erasing billions in market value and shaking investor confidence. The company's reputation as a reliable and transparent business was_severely compromised, prompting a major restructuring effort under Lewis's leadership. Tesco's board responded by suspending multiple senior executives, including Chris Bush, and overhauling financial oversight practices to prevent future infractions. Legal outcomes followed over the next few years. In 2017, Tesco agreed to a Deferred Prosecution Agreement (DPA) with the SFO, acknowledging accountability for false accounting practices. This deal included a 129 million fine and a requirement for Tesco to cover the costs of the investigation. Additionally, the Financial Conduct Authority imposed a 85 million compensation package to address losses incurred by investors. Attempts to hold individual executives criminally liable were less straightforward. Though Chris Bush and two other senior executives faced trials related to fraud and false accounting, they were acquitted in 2018 due to insufficient evidence proving their intent to mislead. The fallout, however, did result in significant financial repercussions and public embarrassment for the company. In conclusion, Tesco's 2014 profit overstatement scandal highlighted serious deficiencies in corporate governance and ethical conduct within the company's leadership. While the organization itself faced substantial monetary penalties and reputational damage, the individuals at the center of the scandal did not receive jail time. The case underscored the necessity for strict compliance with financial regulations and reinforced the importance of accurate reporting to maintain trust in the market. The scandal had profound consequences. Tesco's shares plummeted, erasing billions in market value and shaking investor confidence. The company's reputation as a reliable and transparent business was_severely compromised, prompting a major restructuring effort under Lewis's leadership. Tesco's board responded by suspending multiple senior executives, including Chris Bush, and overhauling financial oversight practices to prevent future infractions. Stakeholders in the Tesco 2014 Profit Overstatement Case Stakeholder Senior Management (CEO, CFO, Executives) Employees Existing Shareholders New Shareholders Objectives Maintain high revenue and profit growth, secure bonuses, and uphold reputation. Job security, fair working conditions, and career growth. Maximize returns on investments and ensure long-term growth. Invest based on expected growth and profitability. Observations Pre- Crisis Focused on delivering strong financial results to maintain investor confidence. General trust in the company's financial stability; unaware of accounting issues. Believed in the reliability of Tesco's strong financial statements. Attracted by Tesco's reported strong financial position and growth potential. Impact of the Crisis Significant fallout: several executives were suseended, faced trials, or resigned. Experienced uncertainty and potential layoffs due to financial instability and restructuring. Lost significant value due to the share price drop, leading to financial losses. Entered at a high point and experienced immediate losses Short Sellers Regulators (FCA, SFQ) Suppliers Auditors (Deloitte) Customers Profit from a decline in Tesco's stock price. Ensure transparency, adherence to financial regulations, and market integrity. Maintain a stable relationship with Tesco for consistent sales and payment terms. Uphold auditing standards and ensure financial accuracy. Access to reliable products and services at competitive prices. Monitored financial statements for potential weaknesses but saw no immediate red flags before the crisis. Expected accure reporting from Tesco and compliance with financial laws. Worked under pressure to provide promotionalincome and rebates. Trusted Tesco's management but faced challenges in uncovering early signs of malpractice. Continued to trust Tescoasa reputable retailer. as the scandal emerged. Benefited from the sharp decline in Tesco's share price as the scandal was_ revealed. Had to investigate and take action. fined Tesco and managed investor compensation. Faced potential payment delays and renegotiations due to Tesco's financial woes. Played a key role in investigating the crisis; reputation affected by t_)gi_n__ gr_'nljgclto the case. Experienced potential changes in service quality and prices due to Competitors Financial Analysts Investors' Associations PwC (Previous Auditors) B) Gain market share and compete effectively in the retail space. Provide accurate forecasts and recommendations based on company data. Ensure member interests are protected and supported. Ensure compliance with auditing standards and accurate financial reporting. Recognized Tesco as a dominant force in the retail market. Relied on Tesco's published financials to guide analysis and recommendations. Advocated for transparency and accountability from major companies like Tesco. Provided audit services before Deloitte, maintaining the perception of proper financial oversight. company restructuring. Gained an advantage as Tesco's scandal damaged its reputation, allowing competitors to attract customers. Lost credibility with clients due to inaccurate analyses based on misleading data. Pushed for reforms and greater transparency post- crisis to protect members' investments. Reputation was, indirectly affected, as questions arose about the effectiveness of Erevious audits. The concept of the "invisible hand," coined by Adam Smith, describes the unintended social benefits that arise from individuals pursuing their own self-interested actions. While this theory often holds true in free-market economies where competition drives innovation and efficiency, the applicability of the "invisible hand" to corporate scandals, such as Tesco's 2014 profit overstatement, presents a more complex picture. In this context, the scandal illustrates that the pursuit of self-interest does not always lead to positive outcomes for society at large. The actions of Tesco's senior management, who sought to inflate profits to preserve market confidence and protect their financial interests, contradict the principle that selt-interest inherently benefits the IEEEEEE N e - common good. In 2014, Tesco's leadership, including key figures such as former CEQ Philip Clarke and CFO Laurie Mcllwee, engaged in accounting practices that involved the premature recognition of supplier rebates and promotional income. This manipulation, intended to overstate profits by approximately 250 million, was driven by the desire to project robust financial health to shareholders and maintain stock prices. While this move temporarily preserved the appearance of stability and success, it did not align with the broader societal benefit that the "invisible hand" suggests. Instead, the scandal resulted in severe consequences, including a loss of trust among investors, significant financial penalties, and lasting damage to Tesco's reputation. These outcomes demonsirate that self-serving actions by corporate leaders, when left unchecked, can undermine market integrity and public confidence. The erosion of trust in financial reporting and corporate governance as a_result of Tesco's profit overstatement had wider implications for various stakeholders. Existing shareholders suffered substantial losses as Tesco's stock value plummeted, wiping out billions in market capitalization. New investors, attracted by what appeared to be a thriving company, also faced immediate financial repercussions once the scandal was exposed. The negative impact extended beyond Tesco's shareholders; customers, employees, and suppliers were indirectly affected by the company's resulting financial instability and restructuring efforts. For employees, job security became uncertain, and for suppliers, payment terms and contracts faced potential renegotiation. The shockwave of the scandal underscored that when corporate leaders prioritize their own gain over ethical business practices, the resulting damage extends beyond the confines of the company, affecting the broader economy and public trust. Furthermore, the regulatory response to Tesco's misconduct highlights the divergence between self-interest and societal good. The Financial Conduct Authority (FCA) and the Serious Fraud Office (SFO) launched investigations into Tesco's financial practices, which culminated in a Deferred Prosecution Agreement (DPA) and a substantial fine of 129 million. This regulatory intervention was necessary to hold the company accountable and to reinforce the importance of transparency in financial reporting. While one could argue that regulatory actions and subsequent corporate reforms were beneficial outcomes in the long term, these results were corrective rather than a natural product of the original self-interested behavior. The "invisible hand" principle implies that self-regulating actions should inherently guide the market toward positive outcomes without the need for external intervention. In Tesco's case, it was only through exposure and regulatory pressure that the company and the market were steered toward a more ethical and transparent path. Some proponents of the "invisible hand" might suggest that the scandal's eventual positive effectssuch as strengthened financial oversight and increased awareness of ethical standards align with the theory's broader implications. The exposure of corporate misconduct can lead to improved practices and regulations that enhance market efficiency and protect stakeholders. However, this perspective fails to account for the immediate and significant harm caused by unethical practices. The benefits that emerged after the scandal were not a direct result of the self-serving actions of Tesco's management but rather a consequence of public and regulatory backlash. The notion that self-interest leads to societal benefit breaks down when the actions taken are deceptive and undermine the foundational principles of trust and integrity within the market. In conclusion, the Tesco 2014 profit overstatement scandal exemplifies a case where the pursuit of self-interest failed to align with the "invisible hand" concept as described by Adam Smith. While the company's management acted to protect and bolster their financial standing, their actions ultimately led to adverse outcomes for sharcholders, employees, customers, and the broader public. The scandal necessitated regulatory intervention and caused reputational damage that far outweighed any short-term benefits gained through unethical accounting practices. Although reforms and stronger financial oversight emerged as indirect benefits, they were a reaction to misconduct rather than an inherent result of it. This case underscores that in the absence of ethical standards and accountability, self-interested actions by corporate leaders can lead to outcomes that are detrimental to both the market and society, challenging the universality of the "invisible hand" theory in the context of corporate governance

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock

Students Have Also Explored These Related Finance Questions!