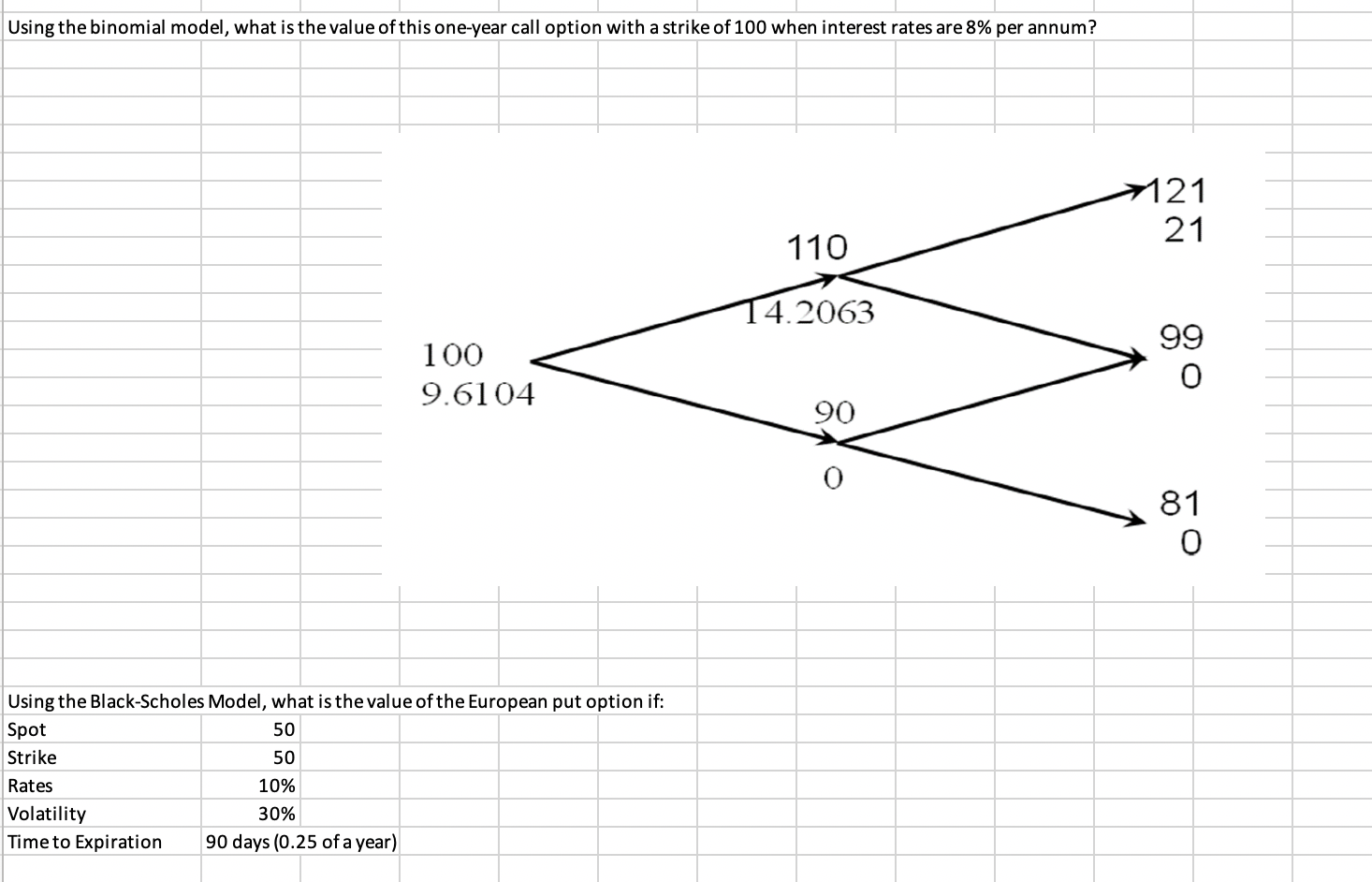

Question: Using the binomial model, what is the value of this one-year call option with a strike of 100 when interest rates are 8% per annum?

Using the binomial model, what is the value of this one-year call option with a strike of 100 when interest rates are 8% per annum? Using the Black-Scholes Model, what is the value of the European put option if: \begin{tabular}{|l|r|l|l|} \hline Using the Black-Scholes Model, what is the value of the European put option if: \\ \hline Spot & 50 & & \\ \hline Strike & 50 & & \\ \hline Rates & 10% & & \\ \hline Volatility & 30% \\ \hline Time to Expiration & 90 days (0.25 of a year) & & \\ \hline \end{tabular}

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock