Question: Using the bond data Round to two decimals what is the effective duration of the bond assuming a 1% increase in current interest rates?

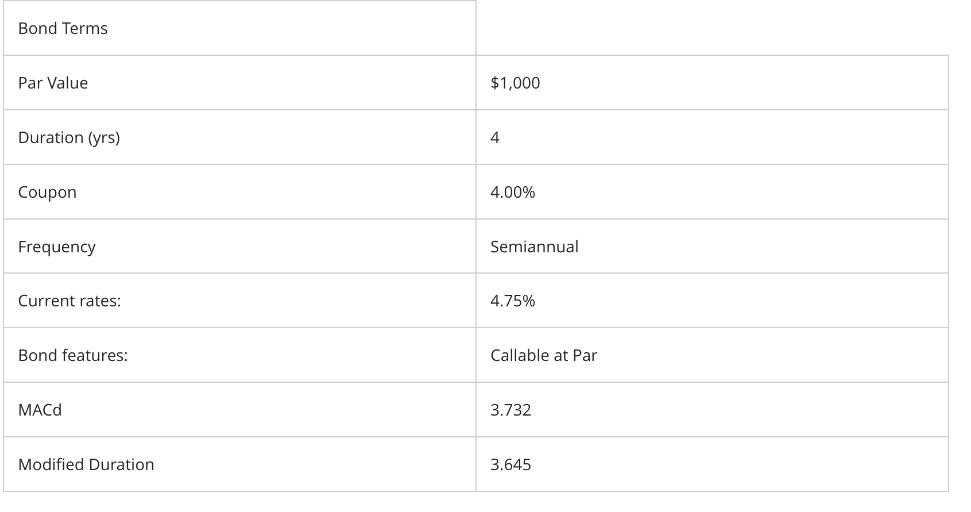

Using the bond data Round to two decimals what is the effective duration of the bond assuming a 1% increase in current interest rates? Bond Terms Par Value Duration (yrs) Coupon Frequency Current rates: Bond features: MACD Modified Duration $1,000 4 4.00% Semiannual 4.75% Callable at Par 3.732 3.645

Step by Step Solution

★★★★★

3.39 Rating (155 Votes )

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

The effective duration of a bond measures its sensitivi... View full answer

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock