Question: Using the calibrated binomial tree in Exhibit 18-12, answer the following two questions: a.What is the value of a 3% bond that matures in 3

Using the calibrated binomial tree in Exhibit 18-12, answer the following two questions:

a.What is the value of a 3% bond that matures in 3 years and is callable in year 1 at 102% of face amount and callable in year 2 at 101% of face amount?

b.What is the value of a 5% bond that matures in 3 years and is not callable but is putable in year 2 at 99% of face amount?

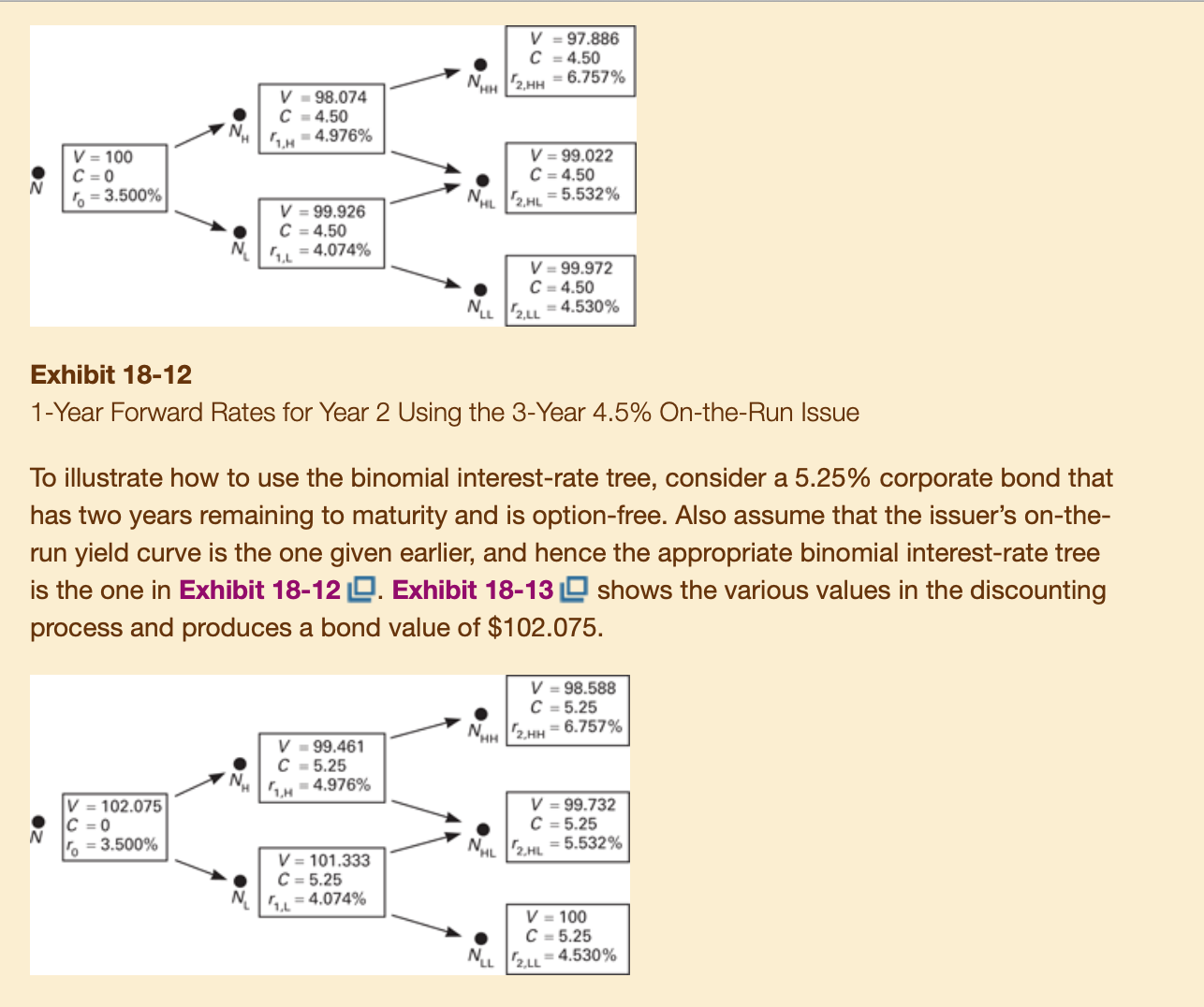

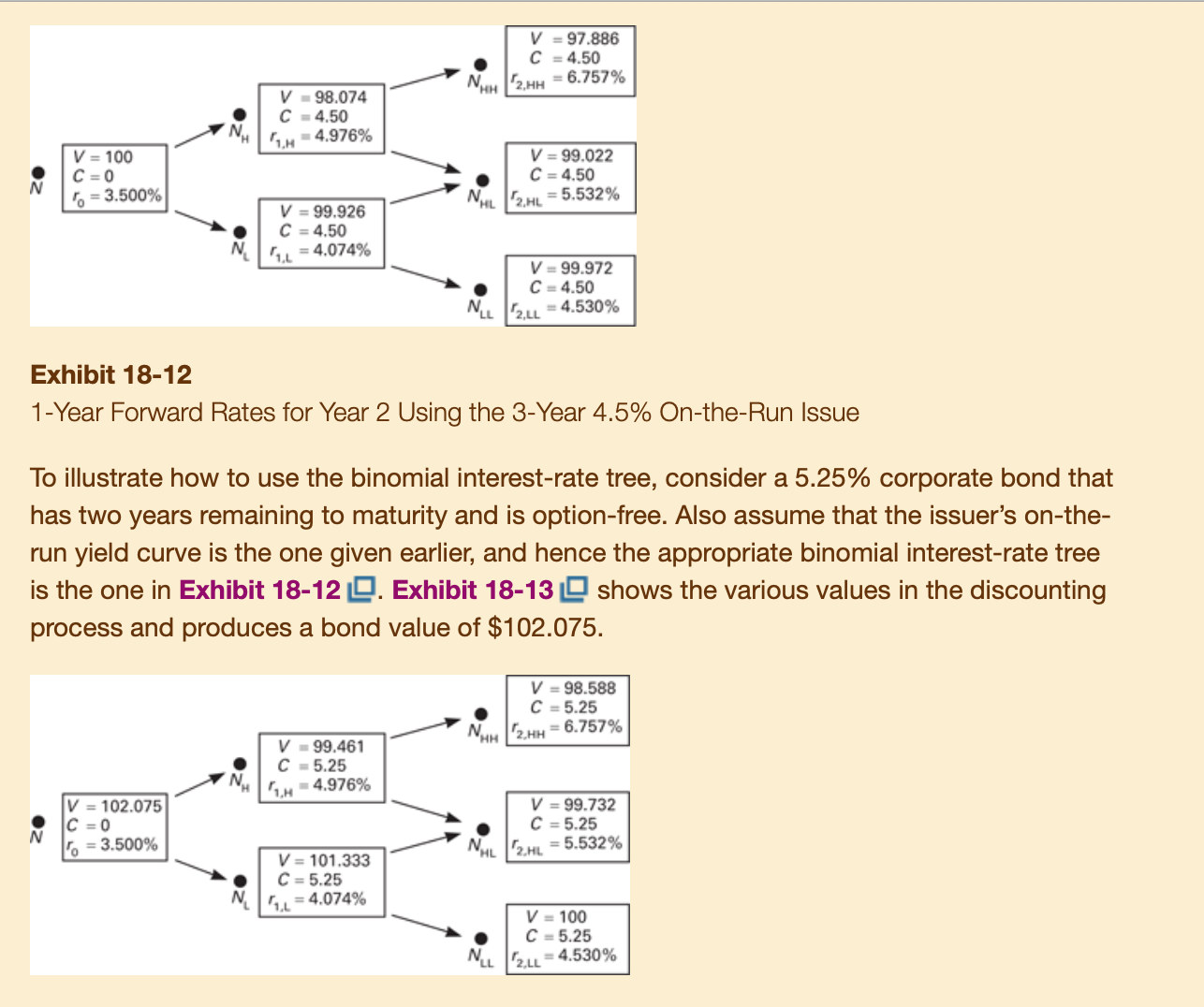

V = 97.886 C = 4.50 V - 98.074 NUH 2.HH = 6.757% C = 4.50 1.H - 4.976% V = 100 V = 99.022 C=0 C = 4.50 TO = 3.500% V = 99.926 NHL 2.HL = 5.532% C = 4.50 1 = 4.074% V = 99.972 C = 4.50 NIL "2.LL = 4.530% Exhibit 18-12 1-Year Forward Rates for Year 2 Using the 3-Year 4.5% On-the-Run Issue To illustrate how to use the binomial interest-rate tree, consider a 5.25% corporate bond that has two years remaining to maturity and is option-free. Also assume that the issuer's on-the- run yield curve is the one given earlier, and hence the appropriate binomial interest-rate tree is the one in Exhibit 18-12 Q. Exhibit 18-13 shows the various values in the discounting process and produces a bond value of $102.075. V = 98.588 C = 5.25 V - 99.461 2.HH = 6.757% C - 5.25 1.H - 4.976% V = 102.075 V = 99.732 C =0 C = 5.25 To = 3.500% V = 101.333 NHL 2.HL = 5.532% C = 5.25 1.L = 4.074% V = 100 C = 5.25 2.LL = 4.530%

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts