Question: Using the data in Table 21.1, compare the price on July 24,2009 , of the following options on JetBlue stock to the price predicted by

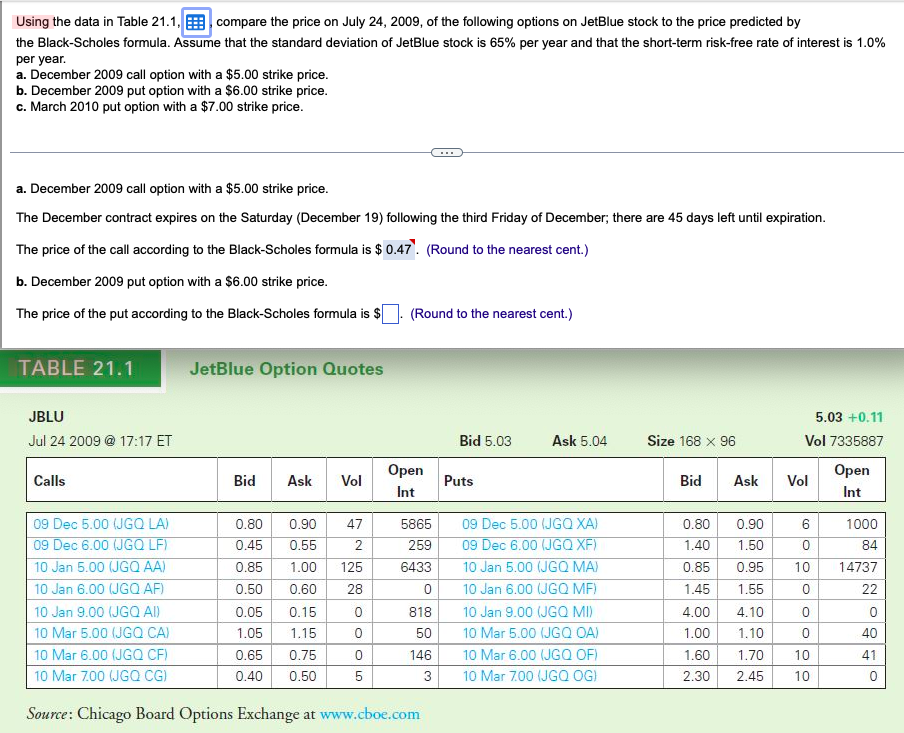

Using the data in Table 21.1, compare the price on July 24,2009 , of the following options on JetBlue stock to the price predicted by the Black-Scholes formula. Assume that the standard deviation of JetBlue stock is 65% per year and that the short-term risk-free rate of interest is 1.0% per year. a. December 2009 call option with a $5.00 strike price. b. December 2009 put option with a $6.00 strike price. c. March 2010 put option with a $7.00 strike price. a. December 2009 call option with a $5.00 strike price. The December contract expires on the Saturday (December 19) following the third Friday of December; there are 45 days left until expiration. The price of the call according to the Black-Scholes formula is 9 (Round to the nearest cent.) b. December 2009 put option with a $6.00 strike price. The price of the put according to the Black-Scholes formula is $ (Round to the nearest cent.) JetBlue Option Quotes Source: Chicago Board Options Exchange at www.cboe.com

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts