Question: Using the workpapers below please write down the memo using the template below. Oceanview Marine Company 14-3 Audit Program (performance format) OBZ Tests of Controls

Using the workpapers below please write down the memo using the template below.

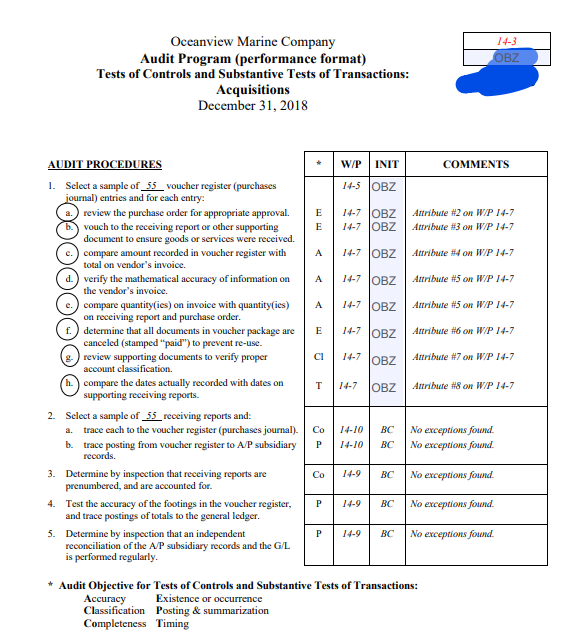

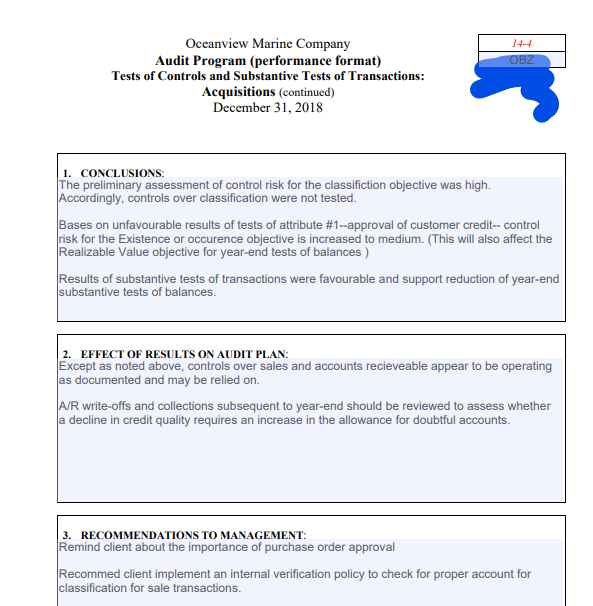

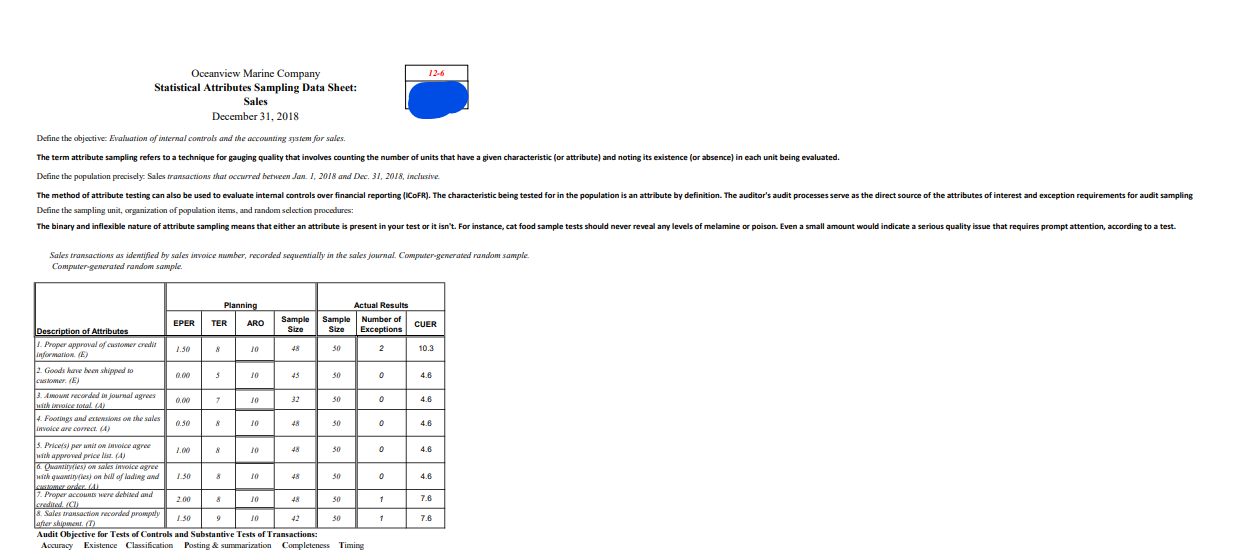

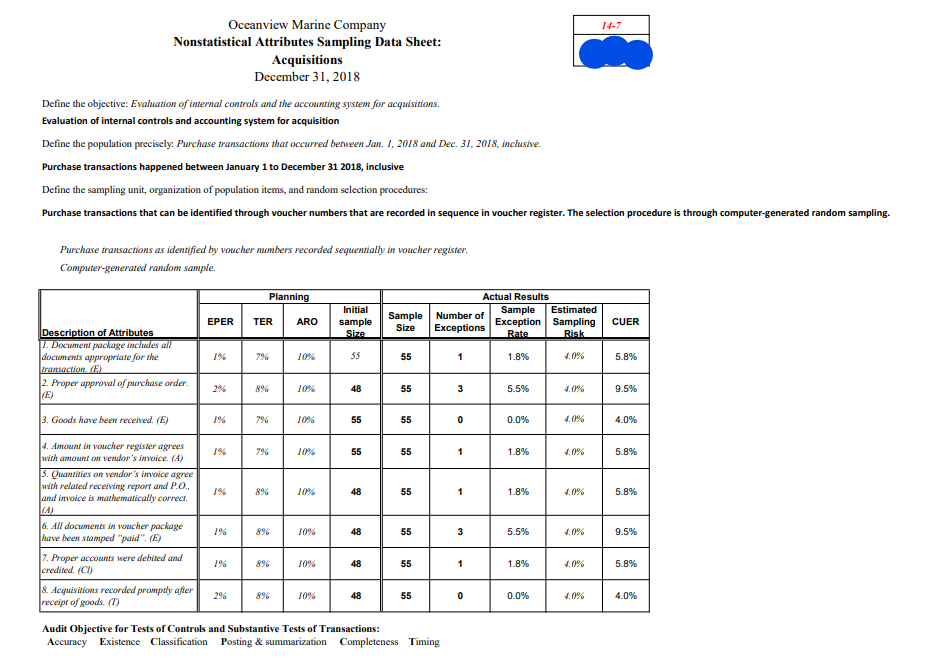

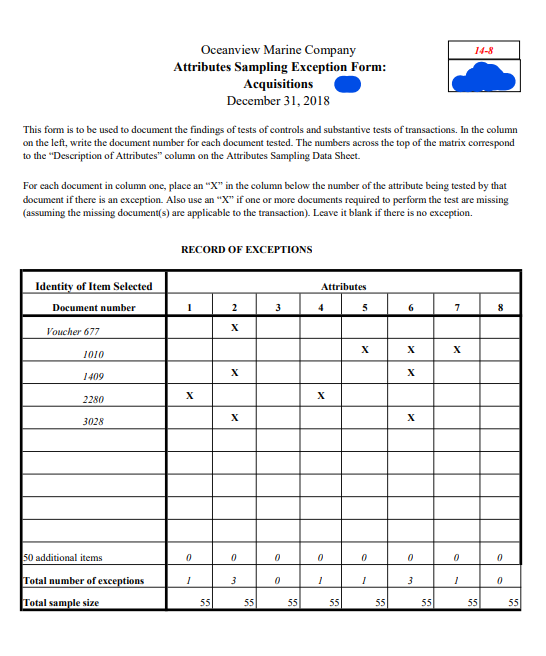

Oceanview Marine Company 14-3 Audit Program (performance format) OBZ Tests of Controls and Substantive Tests of Transactions: Acquisitions December 31, 2018 AUDIT PROCEDURES W/P INIT COMMENTS 1. Select a sample of _55 voucher register (purchases 14-5 OBZ journal) entries and for each entry: review the purchase order for appropriate approval. E 14-7 JOBZ Attribute #2 on W/P 14-7 vouch to the receiving report or other supporting 14-7 OBZ Atribute #3 on W/P 14-7 document to ensure goods or services were received. compare amount recorded in voucher register with A 14-7 JOBZ Attribute #4 on W/P 14-7 otal on vendor's invoice. verify the mathematical accuracy of information on A 14-7 OBZ Attribute #5 on W/P 14-7 he vendor's invoice. compare quantity(ies) on invoice with quantity (ies) A 14-7 OBZ Antribute #5 on W/P 14-7 on receiving report and purchase order. determine that all documents in voucher package are E 14-7 OBZ Antribute #6 on W/P 14-7 canceled (stamped "paid") to prevent re-use. review supporting documents to verify proper CI 14-7 JOBZ Attribute #7 on W/P 14-7 account classification. compare the dates actually recorded with dates on T 14-7 OBZ Attribute #8 on W/P 14-7 supporting receiving reports. 2. Select a sample of _55 receiving reports and: a. trace each to the voucher register (purchases journal). Co 14-10 BC No exceptions found. b. trace posting from voucher register to A/P subsidiary P 14-10 BC No exceptions found. records. 3. Determine by inspection that receiving reports are Co 14-9 BC No exceptions found. prenumbered, and are accounted for. 4. Test the accuracy of the footings in the voucher register, No exceptions found and trace postings of totals to the general ledger. 5. Determine by inspection that an independent P 14-9 BC No exceptions found. reconciliation of the A/P subsidiary records and the G/L is performed regularly. * Audit Objective for Tests of Controls and Substantive Tests of Transactions: Accuracy Existence or occurrence Classification Posting & summarization Completeness TimingOceanview Marine Company 14-4 Audit Program (performance format) DBZ Tests of Controls and Substantive Tests of Transactions: Acquisitions (continued) December 31, 2018 1. CONCLUSIONS: The preliminary assessment of control risk for the classifiction objective was high. Accordingly, controls over classification were not tested. Bases on unfavourable results of tests of attribute #1--approval of customer credit-- control risk for the Existence or occurence objective is increased to medium. (This will also affect the Realizable Value objective for year-end tests of balances ) Results of substantive tests of transactions were favourable and support reduction of year-end substantive tests of balances. 2. EFFECT OF RESULTS ON AUDIT PLAN: Except as noted above, controls over sales and accounts recieveable appear to be operating as documented and may be relied on. A/R write-offs and collections subsequent to year-end should be reviewed to assess whether a decline in credit quality requires an increase in the allowance for doubtful accounts. 3. RECOMMENDATIONS TO MANAGEMENT: Remind client about the importance of purchase order approval Recommed client implement an internal verification policy to check for proper account for classification for sale transactions.Oceanview Marine Company 12-6 Statistical Attributes Sampling Data Sheet: Sales December 31, 2018 Define the objective: Evaluation of internal controls and the accounting system for sales. The term attribute sampling refers to a technique for gauging quality that involves counting the number of units that have a given characteristic (or attribute] and noting its existence (or absence] in each unit being evaluated. Define the population precisely. Sales transactions that occurred between Jan. 1, 2018 and Dec. 31, 2018, inclusive. The method of attribute testing can also be used to evaluate internal controls over financial reporting (ICoFR). The characteristic being tested for in the population is an attribute by definition. The auditor's audit processes serve as the direct source of the attributes of interest and exception requirements for audit sampling Define the sampling unit, organization of population items, and random selection procedures: The binary and inflexible nature of attribute sampling means that either an attribute is present in your test or it isn't. For instance, cat food sample tests should never reveal any levels of melamine or poison. Even a small amount would indicate a serious quality issue that requires prompt attention, according to a test. Sales transactions as identified by sales invoice number, recorded sequentially in the sales journal. Computer-generated random sample. Computer generated random sample. Planning Actual Results EPER TER ARO Sample Sample Number of CUER Description of Attributes Size Exceptions I. Proper approval of customer credit 1.50 50 10.3 information. (E) Goods have been shipped to Awowme recorded in journal agrees 4.8 with Mvoice Total MA 4. Footings and extensions on the sales 0.30 invoice are correct. () 5. Prices) per unit on invoice agree 1.00 4 8 with approved price Mat. (A) a. (wantingies of sakes invoice agree with quaminvies) on bill of lading and 1 30 50 7. Proper accounts have denied and 2.00 48 50 1 7.8 credited. (!) &. Sales transaction recorded promptly 150 7.8 after shipment. (12 Audit Objective for Tests of Controls and Substantive Tests of Transactions: Accuracy Existence Classification Posting & summarization Completeness TimingOceanview Marine Company 14-7 Nonstatistical Attributes Sampling Data Sheet: Acquisitions December 31, 2018 Define the objective: Evaluation of internal controls and the accounting system for acquisitions. Evaluation of internal controls and accounting system for acquisition Define the population precisely. Purchase transactions that occurred between Jan. 1, 2018 and Dec. 31, 2018, inclusive. Purchase transactions happened between January 1 to December 31 2018, inclusive Define the sampling unit, organization of population items, and random selection procedures: Purchase transactions that can be identified through voucher numbers that are recorded in sequence in voucher register. The selection procedure is through computer-generated random sampling. Purchase transactions as identified by voucher numbers recorded sequentially in voucher register. Computer-generated random sample. Planning Actual Results Initial Sample Estimated EPER TER ARO sample Sample Number of Exceptions Exception CUER Size Sampling Description of Attributes Size Rate Risk J. Document package includes all documents appropriate for the 19% 79% 109% 55 1.8% 4.09% 5.8% transaction. (E) 2. Proper approval of purchase order. 10%% E 5.5% 4.0% 9.5% 3. Goods have been received. (E) 19% 79% 55 0.0% 4.09% 4.0% 4. Amount in voucher register agrees 79% 55 1.8% 4.0% 5.8% with amount on vendor's invoice. (A) 3. Ownlilies on vendor's invoice agree with related receiving report and P.O., 10% 55 1.8% 4.0%% 5.8% and invoice is mathematically correct. (4) 6. All documents in voucher package 3 5.5% 4.0% 9.5% have been stamped "paid". (E) 7. Proper accounts were debited and 19% 8% 10% 1.8% 1.0%% 5.8% credited. (CI) 8. Acquisitions recorded promptly after 29% 10% 55 0.0% 4.09% 4.0% receipt of goods. (T) Audit Objective for Tests of Controls and Substantive Tests of Transactions: Accuracy Existence Classification Posting & summarization Completeness TimingOceanview Marine Company 14-8 Attributes Sampling Exception Form: Acquisitions December 31, 2018 This form is to be used to document the findings of tests of controls and substantive tests of transactions. In the column on the left, write the document number for each document tested. The numbers across the top of the matrix correspond to the "Description of Attributes" column on the Attributes Sampling Data Sheet. For each document in column one, place an "X" in the column below the number of the attribute being tested by that document if there is an exception. Also use an "X" if one or more documents required to perform the test are missing (assuming the missing document(s) are applicable to the transaction). Leave it blank if there is no exception. RECORD OF EXCEPTIONS Identity of Item Selected Attributes Document number 2 3 S 6 7 8 Voucher 677 X 1010 X X X 1409 X X 2280 x 3028 X X 50 additional items Total number of exceptions 3 Total sample size 55 55 55 55 55 55 55 55

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts