Question: uu 14.43) The variance for Wis or = ar + 2 + 2Col X,Y or, using the correlation, is 44 =reba + 2ab-Corr X, Y)oxy

uu

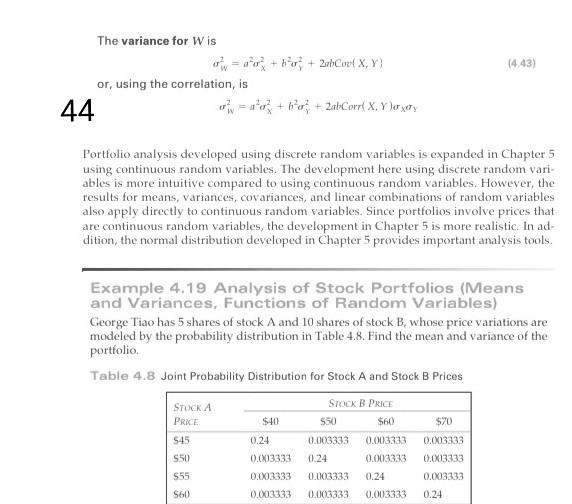

14.43) The variance for Wis or = ar + 2 + 2Col X,Y or, using the correlation, is 44 =reba + 2ab-Corr X, Y)oxy Portfolio analysis developed using discrete random variables is expanded in Chapter 5 using continuous random variables. The development here using discrete random vari- ables is more intuitive compared to using continuous random variables. However, the results for means, variances, covariances, and linear combinations of random variables also apply directly to continuous random variables. Since portfolios involve prices that are continuous random variables, the development in Chapter 5 is more realistic. In ad- dition, the normal distribution developed in Chapter 5 provides important analysis tools. Example 4.19 Analysis of Stock Portfolios (Means and Variances, Functions of Random Variables) George Tiao has 5 shares of stock A and 10 shares of stock B, whose price variations are modeled by the probability distribution in Table 4.8. Find the mean and variance of the portfolio Table 4.8 Joint Probability Distribution for Stock A and Stock B Prices STOCKB PRICE 550 $60 $40 $70 STOCKA PRICE 545 S50 0.24 0.13333 0.0083333 0.24 0.003333 0.003333 0.24 0.003333 0.0X13333 0.0x13333 0.0833333 0.24 555 0.083333 0.003333 0.003333 0.003333 S60Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock