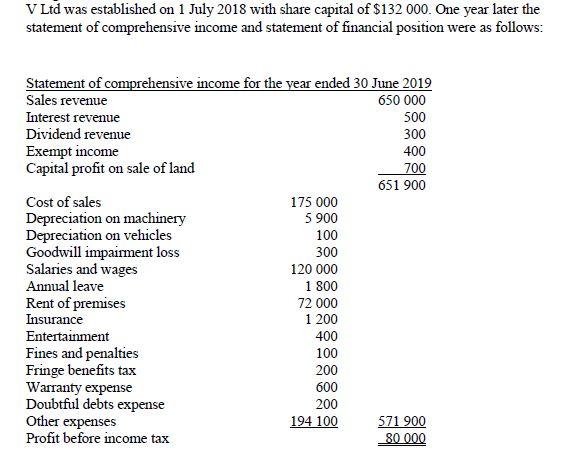

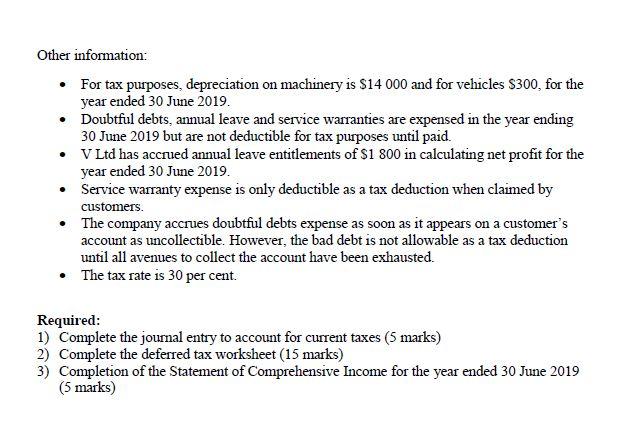

V Ltd was established on 1 July 2018 with share capital of $132 000. One year...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

V Ltd was established on 1 July 2018 with share capital of $132 000. One year later the statement of comprehensive income and statement of financial position were as follows: Statement of comprehensive income for the year ended 30 June 2019 Sales revenue 650 000 Interest revenue Dividend revenue 500 300 Exempt income Capital profit on sale of land 400 700 651 900 Cost of sales Depreciation on machinery Depreciation on vehicles Goodwill impairment loss Salaries and wages Annual leave 175 000 5 900 100 300 120 000 1 800 Rent of premises Insurance 72 000 1 200 Entertainment 400 Fines and penalties Fringe benefits tax Warranty expense Doubtful debts expense Other expenses Profit before income tax 100 200 600 200 194 100 571 900 80 000 Statement of Financial Position as at 30June 2019 Assets Cash 24 000 Accounts Receivable Less: Allowance for doubtful debts 37 500 200 37 300 Interest receivable 100 Inventory Prepaid insurance Machinery (cost) Less: Accumulated depreciation Vehicles 20 000 300 79 000 5 900 73 100 11 000 Less: Accumulated depreciation Goodwill 100 45 000 300 10 900 Less: Accumulated impaiment loss Investments 44 700 25 000 Total assets 235 400 Liabilities Accounts payable Rent payable Provision for annual leave 15 000 6 000 1 800 600 23 400 212 000 Provision for services warranties Total liabilities Net Assets Shareholders' equity Share capital Retained earnings 132 000 80 000 212 000 Other information: • For tax purposes, depreciation on machinery is $14 000 and for vehicles $300, for the year ended 30 June 2019. • Doubtful debts, annual leave and service warranties are expensed in the year ending 30 June 2019 but are not deductible for tax purposes until paid. • V Ltd has accrued annual leave entitlements of $1 800 in calculating net profit for the year ended 30 June 2019. • Service warranty expense is only deductible as a tax deduction when claimed by customers. • The company accrues doubtful debts expense as soon as it appears on a customer's account as uncollectible. However, the bad debt is not allowable as a tax deduction until all avenues to collect the account have been exhausted. The tax rate is 30 per cent. Required: 1) Complete the joumal entry to account for current taxes (5 marks) 2) Complete the deferred tax worksheet (15 marks) 3) Completion of the Statement of Comprehensive Income for the year ended 30 June 2019 (5 marks) V Ltd was established on 1 July 2018 with share capital of $132 000. One year later the statement of comprehensive income and statement of financial position were as follows: Statement of comprehensive income for the year ended 30 June 2019 Sales revenue 650 000 Interest revenue Dividend revenue 500 300 Exempt income Capital profit on sale of land 400 700 651 900 Cost of sales Depreciation on machinery Depreciation on vehicles Goodwill impairment loss Salaries and wages Annual leave 175 000 5 900 100 300 120 000 1 800 Rent of premises Insurance 72 000 1 200 Entertainment 400 Fines and penalties Fringe benefits tax Warranty expense Doubtful debts expense Other expenses Profit before income tax 100 200 600 200 194 100 571 900 80 000 Statement of Financial Position as at 30June 2019 Assets Cash 24 000 Accounts Receivable Less: Allowance for doubtful debts 37 500 200 37 300 Interest receivable 100 Inventory Prepaid insurance Machinery (cost) Less: Accumulated depreciation Vehicles 20 000 300 79 000 5 900 73 100 11 000 Less: Accumulated depreciation Goodwill 100 45 000 300 10 900 Less: Accumulated impaiment loss Investments 44 700 25 000 Total assets 235 400 Liabilities Accounts payable Rent payable Provision for annual leave 15 000 6 000 1 800 600 23 400 212 000 Provision for services warranties Total liabilities Net Assets Shareholders' equity Share capital Retained earnings 132 000 80 000 212 000 Other information: • For tax purposes, depreciation on machinery is $14 000 and for vehicles $300, for the year ended 30 June 2019. • Doubtful debts, annual leave and service warranties are expensed in the year ending 30 June 2019 but are not deductible for tax purposes until paid. • V Ltd has accrued annual leave entitlements of $1 800 in calculating net profit for the year ended 30 June 2019. • Service warranty expense is only deductible as a tax deduction when claimed by customers. • The company accrues doubtful debts expense as soon as it appears on a customer's account as uncollectible. However, the bad debt is not allowable as a tax deduction until all avenues to collect the account have been exhausted. The tax rate is 30 per cent. Required: 1) Complete the joumal entry to account for current taxes (5 marks) 2) Complete the deferred tax worksheet (15 marks) 3) Completion of the Statement of Comprehensive Income for the year ended 30 June 2019 (5 marks) V Ltd was established on 1 July 2018 with share capital of $132 000. One year later the statement of comprehensive income and statement of financial position were as follows: Statement of comprehensive income for the year ended 30 June 2019 Sales revenue 650 000 Interest revenue Dividend revenue 500 300 Exempt income Capital profit on sale of land 400 700 651 900 Cost of sales Depreciation on machinery Depreciation on vehicles Goodwill impairment loss Salaries and wages Annual leave 175 000 5 900 100 300 120 000 1 800 Rent of premises Insurance 72 000 1 200 Entertainment 400 Fines and penalties Fringe benefits tax Warranty expense Doubtful debts expense Other expenses Profit before income tax 100 200 600 200 194 100 571 900 80 000 Statement of Financial Position as at 30June 2019 Assets Cash 24 000 Accounts Receivable Less: Allowance for doubtful debts 37 500 200 37 300 Interest receivable 100 Inventory Prepaid insurance Machinery (cost) Less: Accumulated depreciation Vehicles 20 000 300 79 000 5 900 73 100 11 000 Less: Accumulated depreciation Goodwill 100 45 000 300 10 900 Less: Accumulated impaiment loss Investments 44 700 25 000 Total assets 235 400 Liabilities Accounts payable Rent payable Provision for annual leave 15 000 6 000 1 800 600 23 400 212 000 Provision for services warranties Total liabilities Net Assets Shareholders' equity Share capital Retained earnings 132 000 80 000 212 000 Other information: • For tax purposes, depreciation on machinery is $14 000 and for vehicles $300, for the year ended 30 June 2019. • Doubtful debts, annual leave and service warranties are expensed in the year ending 30 June 2019 but are not deductible for tax purposes until paid. • V Ltd has accrued annual leave entitlements of $1 800 in calculating net profit for the year ended 30 June 2019. • Service warranty expense is only deductible as a tax deduction when claimed by customers. • The company accrues doubtful debts expense as soon as it appears on a customer's account as uncollectible. However, the bad debt is not allowable as a tax deduction until all avenues to collect the account have been exhausted. The tax rate is 30 per cent. Required: 1) Complete the joumal entry to account for current taxes (5 marks) 2) Complete the deferred tax worksheet (15 marks) 3) Completion of the Statement of Comprehensive Income for the year ended 30 June 2019 (5 marks) V Ltd was established on 1 July 2018 with share capital of $132 000. One year later the statement of comprehensive income and statement of financial position were as follows: Statement of comprehensive income for the year ended 30 June 2019 Sales revenue 650 000 Interest revenue Dividend revenue 500 300 Exempt income Capital profit on sale of land 400 700 651 900 Cost of sales Depreciation on machinery Depreciation on vehicles Goodwill impairment loss Salaries and wages Annual leave 175 000 5 900 100 300 120 000 1 800 Rent of premises Insurance 72 000 1 200 Entertainment 400 Fines and penalties Fringe benefits tax Warranty expense Doubtful debts expense Other expenses Profit before income tax 100 200 600 200 194 100 571 900 80 000 Statement of Financial Position as at 30June 2019 Assets Cash 24 000 Accounts Receivable Less: Allowance for doubtful debts 37 500 200 37 300 Interest receivable 100 Inventory Prepaid insurance Machinery (cost) Less: Accumulated depreciation Vehicles 20 000 300 79 000 5 900 73 100 11 000 Less: Accumulated depreciation Goodwill 100 45 000 300 10 900 Less: Accumulated impaiment loss Investments 44 700 25 000 Total assets 235 400 Liabilities Accounts payable Rent payable Provision for annual leave 15 000 6 000 1 800 600 23 400 212 000 Provision for services warranties Total liabilities Net Assets Shareholders' equity Share capital Retained earnings 132 000 80 000 212 000 Other information: • For tax purposes, depreciation on machinery is $14 000 and for vehicles $300, for the year ended 30 June 2019. • Doubtful debts, annual leave and service warranties are expensed in the year ending 30 June 2019 but are not deductible for tax purposes until paid. • V Ltd has accrued annual leave entitlements of $1 800 in calculating net profit for the year ended 30 June 2019. • Service warranty expense is only deductible as a tax deduction when claimed by customers. • The company accrues doubtful debts expense as soon as it appears on a customer's account as uncollectible. However, the bad debt is not allowable as a tax deduction until all avenues to collect the account have been exhausted. The tax rate is 30 per cent. Required: 1) Complete the joumal entry to account for current taxes (5 marks) 2) Complete the deferred tax worksheet (15 marks) 3) Completion of the Statement of Comprehensive Income for the year ended 30 June 2019 (5 marks) V Ltd was established on 1 July 2018 with share capital of $132 000. One year later the statement of comprehensive income and statement of financial position were as follows: Statement of comprehensive income for the year ended 30 June 2019 Sales revenue 650 000 Interest revenue Dividend revenue 500 300 Exempt income Capital profit on sale of land 400 700 651 900 Cost of sales Depreciation on machinery Depreciation on vehicles Goodwill impairment loss Salaries and wages Annual leave 175 000 5 900 100 300 120 000 1 800 Rent of premises Insurance 72 000 1 200 Entertainment 400 Fines and penalties Fringe benefits tax Warranty expense Doubtful debts expense Other expenses Profit before income tax 100 200 600 200 194 100 571 900 80 000 Statement of Financial Position as at 30June 2019 Assets Cash 24 000 Accounts Receivable Less: Allowance for doubtful debts 37 500 200 37 300 Interest receivable 100 Inventory Prepaid insurance Machinery (cost) Less: Accumulated depreciation Vehicles 20 000 300 79 000 5 900 73 100 11 000 Less: Accumulated depreciation Goodwill 100 45 000 300 10 900 Less: Accumulated impaiment loss Investments 44 700 25 000 Total assets 235 400 Liabilities Accounts payable Rent payable Provision for annual leave 15 000 6 000 1 800 600 23 400 212 000 Provision for services warranties Total liabilities Net Assets Shareholders' equity Share capital Retained earnings 132 000 80 000 212 000 Other information: • For tax purposes, depreciation on machinery is $14 000 and for vehicles $300, for the year ended 30 June 2019. • Doubtful debts, annual leave and service warranties are expensed in the year ending 30 June 2019 but are not deductible for tax purposes until paid. • V Ltd has accrued annual leave entitlements of $1 800 in calculating net profit for the year ended 30 June 2019. • Service warranty expense is only deductible as a tax deduction when claimed by customers. • The company accrues doubtful debts expense as soon as it appears on a customer's account as uncollectible. However, the bad debt is not allowable as a tax deduction until all avenues to collect the account have been exhausted. The tax rate is 30 per cent. Required: 1) Complete the joumal entry to account for current taxes (5 marks) 2) Complete the deferred tax worksheet (15 marks) 3) Completion of the Statement of Comprehensive Income for the year ended 30 June 2019 (5 marks) V Ltd was established on 1 July 2018 with share capital of $132 000. One year later the statement of comprehensive income and statement of financial position were as follows: Statement of comprehensive income for the year ended 30 June 2019 Sales revenue 650 000 Interest revenue Dividend revenue 500 300 Exempt income Capital profit on sale of land 400 700 651 900 Cost of sales Depreciation on machinery Depreciation on vehicles Goodwill impairment loss Salaries and wages Annual leave 175 000 5 900 100 300 120 000 1 800 Rent of premises Insurance 72 000 1 200 Entertainment 400 Fines and penalties Fringe benefits tax Warranty expense Doubtful debts expense Other expenses Profit before income tax 100 200 600 200 194 100 571 900 80 000 Statement of Financial Position as at 30June 2019 Assets Cash 24 000 Accounts Receivable Less: Allowance for doubtful debts 37 500 200 37 300 Interest receivable 100 Inventory Prepaid insurance Machinery (cost) Less: Accumulated depreciation Vehicles 20 000 300 79 000 5 900 73 100 11 000 Less: Accumulated depreciation Goodwill 100 45 000 300 10 900 Less: Accumulated impaiment loss Investments 44 700 25 000 Total assets 235 400 Liabilities Accounts payable Rent payable Provision for annual leave 15 000 6 000 1 800 600 23 400 212 000 Provision for services warranties Total liabilities Net Assets Shareholders' equity Share capital Retained earnings 132 000 80 000 212 000 Other information: • For tax purposes, depreciation on machinery is $14 000 and for vehicles $300, for the year ended 30 June 2019. • Doubtful debts, annual leave and service warranties are expensed in the year ending 30 June 2019 but are not deductible for tax purposes until paid. • V Ltd has accrued annual leave entitlements of $1 800 in calculating net profit for the year ended 30 June 2019. • Service warranty expense is only deductible as a tax deduction when claimed by customers. • The company accrues doubtful debts expense as soon as it appears on a customer's account as uncollectible. However, the bad debt is not allowable as a tax deduction until all avenues to collect the account have been exhausted. The tax rate is 30 per cent. Required: 1) Complete the joumal entry to account for current taxes (5 marks) 2) Complete the deferred tax worksheet (15 marks) 3) Completion of the Statement of Comprehensive Income for the year ended 30 June 2019 (5 marks) V Ltd was established on 1 July 2018 with share capital of $132 000. One year later the statement of comprehensive income and statement of financial position were as follows: Statement of comprehensive income for the year ended 30 June 2019 Sales revenue 650 000 Interest revenue Dividend revenue 500 300 Exempt income Capital profit on sale of land 400 700 651 900 Cost of sales Depreciation on machinery Depreciation on vehicles Goodwill impairment loss Salaries and wages Annual leave 175 000 5 900 100 300 120 000 1 800 Rent of premises Insurance 72 000 1 200 Entertainment 400 Fines and penalties Fringe benefits tax Warranty expense Doubtful debts expense Other expenses Profit before income tax 100 200 600 200 194 100 571 900 80 000 Statement of Financial Position as at 30June 2019 Assets Cash 24 000 Accounts Receivable Less: Allowance for doubtful debts 37 500 200 37 300 Interest receivable 100 Inventory Prepaid insurance Machinery (cost) Less: Accumulated depreciation Vehicles 20 000 300 79 000 5 900 73 100 11 000 Less: Accumulated depreciation Goodwill 100 45 000 300 10 900 Less: Accumulated impaiment loss Investments 44 700 25 000 Total assets 235 400 Liabilities Accounts payable Rent payable Provision for annual leave 15 000 6 000 1 800 600 23 400 212 000 Provision for services warranties Total liabilities Net Assets Shareholders' equity Share capital Retained earnings 132 000 80 000 212 000 Other information: • For tax purposes, depreciation on machinery is $14 000 and for vehicles $300, for the year ended 30 June 2019. • Doubtful debts, annual leave and service warranties are expensed in the year ending 30 June 2019 but are not deductible for tax purposes until paid. • V Ltd has accrued annual leave entitlements of $1 800 in calculating net profit for the year ended 30 June 2019. • Service warranty expense is only deductible as a tax deduction when claimed by customers. • The company accrues doubtful debts expense as soon as it appears on a customer's account as uncollectible. However, the bad debt is not allowable as a tax deduction until all avenues to collect the account have been exhausted. The tax rate is 30 per cent. Required: 1) Complete the joumal entry to account for current taxes (5 marks) 2) Complete the deferred tax worksheet (15 marks) 3) Completion of the Statement of Comprehensive Income for the year ended 30 June 2019 (5 marks) V Ltd was established on 1 July 2018 with share capital of $132 000. One year later the statement of comprehensive income and statement of financial position were as follows: Statement of comprehensive income for the year ended 30 June 2019 Sales revenue 650 000 Interest revenue Dividend revenue 500 300 Exempt income Capital profit on sale of land 400 700 651 900 Cost of sales Depreciation on machinery Depreciation on vehicles Goodwill impairment loss Salaries and wages Annual leave 175 000 5 900 100 300 120 000 1 800 Rent of premises Insurance 72 000 1 200 Entertainment 400 Fines and penalties Fringe benefits tax Warranty expense Doubtful debts expense Other expenses Profit before income tax 100 200 600 200 194 100 571 900 80 000 Statement of Financial Position as at 30June 2019 Assets Cash 24 000 Accounts Receivable Less: Allowance for doubtful debts 37 500 200 37 300 Interest receivable 100 Inventory Prepaid insurance Machinery (cost) Less: Accumulated depreciation Vehicles 20 000 300 79 000 5 900 73 100 11 000 Less: Accumulated depreciation Goodwill 100 45 000 300 10 900 Less: Accumulated impaiment loss Investments 44 700 25 000 Total assets 235 400 Liabilities Accounts payable Rent payable Provision for annual leave 15 000 6 000 1 800 600 23 400 212 000 Provision for services warranties Total liabilities Net Assets Shareholders' equity Share capital Retained earnings 132 000 80 000 212 000 Other information: • For tax purposes, depreciation on machinery is $14 000 and for vehicles $300, for the year ended 30 June 2019. • Doubtful debts, annual leave and service warranties are expensed in the year ending 30 June 2019 but are not deductible for tax purposes until paid. • V Ltd has accrued annual leave entitlements of $1 800 in calculating net profit for the year ended 30 June 2019. • Service warranty expense is only deductible as a tax deduction when claimed by customers. • The company accrues doubtful debts expense as soon as it appears on a customer's account as uncollectible. However, the bad debt is not allowable as a tax deduction until all avenues to collect the account have been exhausted. The tax rate is 30 per cent. Required: 1) Complete the joumal entry to account for current taxes (5 marks) 2) Complete the deferred tax worksheet (15 marks) 3) Completion of the Statement of Comprehensive Income for the year ended 30 June 2019 (5 marks)

Expert Answer:

Answer rating: 100% (QA)

Calculation of taxable income and tax liability Particulars Amount Amount Profit before income tax 8... View the full answer

Related Book For

Posted Date:

Students also viewed these accounting questions

-

The Statement of Comprehensive Income was required by FASB in SFAS Statement No. 130; describe the formats that are acceptable to display the information in the statement.

-

On 1 July 2018 Harris Ltd purchased an 80% controlling interest in Shamin Ltd for a consideration of S350,000. On that date the pre-control equity of Shamin consisted of Paid up capital Retained...

-

on 1 july 2018 Grant ltd acquired an item of equipment with an acquisition cost of $590,000. the equipment can be used for 9 years. residual value is $50,000. on 30 june 2019, the end of financial...

-

How did your parents communication with you influence your self-concept?

-

Before starring in Iron Man, Robert Downey Jr. had appeared in 45 movies that grossed an average of $5 million on the opening weekend. In contrast, Iron Man grossed $102 million. a. How do you expect...

-

Suppose when Russia opens to trade, it imports automobiles, a capital-intensive good. a. According to the Heckscher-Ohlin theorem, is Russia capital-abundant or labor-abundant? Briefly explain. b....

-

List ways in which virtual collaboration can be used in business.

-

You are given the following situations: 1. Thomas Petry owes a debt of $7,000 from the purchase of a boat. The debt bears interest of 12% payable annually. Petry will pay the debt and interest in...

-

Consider the following facts and identify those that would be necessary to (1) disclose or (2) include in an antenuptial agreement. 1 Mac is a widower who has three adult children. All the children...

-

A company wants to locate a distribution center that will serve six of its major customers in a 30 30 mi area. The locations of the customers relative to the southwest corner of the area are given...

-

The longest wavelength doublet absorption transition is observed at 589 and 589.6nm Calculate the frequency of each transition and energy difference between two excited states.

-

Both a perfect competitor and a monopolistic competitor choose output where MC = MR, and neither makes a profit in the long run. How is it, then, that the monopolistic competitor produces less than a...

-

The role of sourcing, planning, and analysis is to analyze spending across various suppliers and component categories to identify opportunities for decreasing the total cost. to analyze spending...

-

One of the pitfalls of these forecasting tools is it is difficult to do time-series analysis. relying on them too much, which eliminates the human element in forecasting. they take up too much human...

-

Explain the effects on college education of the development of a teaching machine that you plug into a students brain and that makes the student understand everything. How would your answer differ if...

-

Shannon Jones just received an e-mail message from an angel investor who has agreed to listen to her pitch her business idea. The investor said, Your timing is goodI just happen to be sitting on...

-

2. Darrell spoke with a financial advisor and learns he can afford to make monthly payments of $1000 for the next 5 years in order to start a business. At this point in time, he is able to borrow an...

-

From the choice of simple moving average, exponential smoothing, and linear regression analysis, which forecasting technique would you consider the most accurate? Why? please write it in word...

-

Describe the difference between the economic entity concept and the parent company concept approaches to the reporting of subsidiary assets and liabilities in the consolidated financial statements on...

-

Are International Financial Reporting Standards (IFRS) issued by the International Accounting Standards Board (IASB) considered authoritative by the Codification?

-

On January 1, 2008, Tony and Jon formed T&J Personal Financial Planning with capital investments of $480,000 and $340,000, respectively. The partners wanted to draft a profit and loss agreement that...

-

Speeds of bullet trains. Determine whether the data are qualitative or quantitative. Explain your reasoning.

-

American Standard Code for Information Interchange (ASCII) codes. Determine whether the data are qualitative or quantitative. Explain your reasoning.

-

Colors of fabrics at a clothing store. Determine whether the data are qualitative or quantitative. Explain your reasoning.

Study smarter with the SolutionInn App