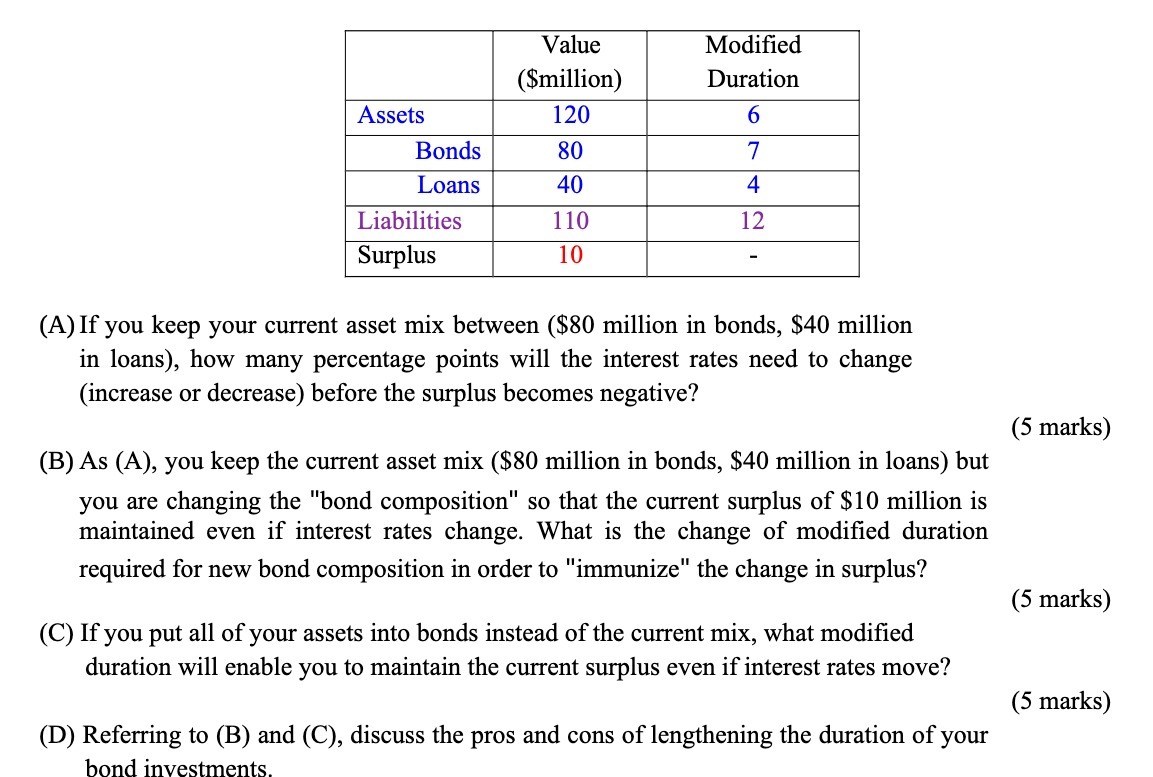

Question: Value Modified ($million) Duration Assets 120 6 Bonds 80 7 Loans 40 4 Liabilities 110 12 Surplus 10 (A) If you keep your current asset

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock