Question: Value options Inventory conversion period: 56.77 days 43.26 days 45.96 days 131.70 days Average collection period: 34.20 days 23.32 days 86.55 days 29.54 days Payables

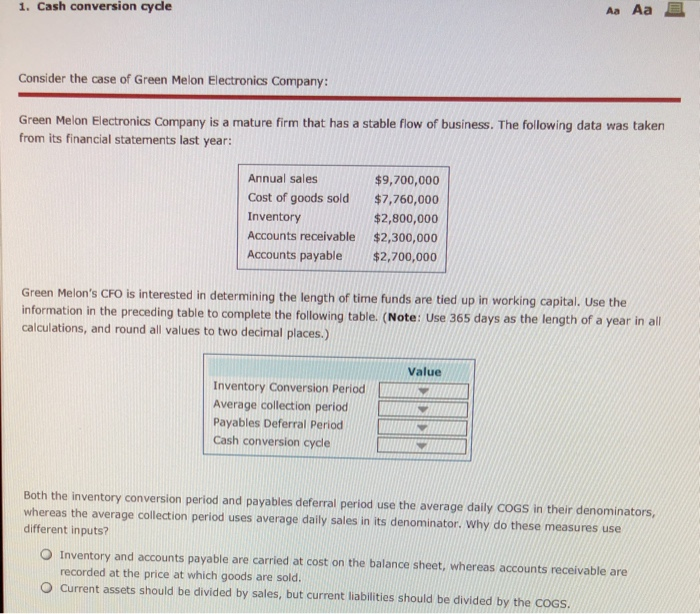

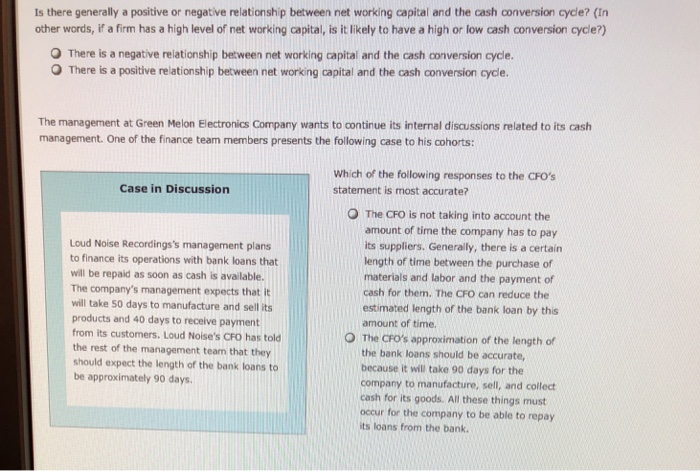

1. Cash conversion cydle AaAa Consider the case of Green Melon Electronics Company: Green Melon Electronics Company is a mature firm that has a stable flow of business. The following data was taken from its financial statements last year: Annual sales Cost of goods sold $7,760,000 Inventory Accounts receivable $2,300,000 Accounts payable$2,700,000 $9,700,000 $2,800,000 Green Melon's CFO is interested in determining the length of time funds are tied up in working capital. Use the information in the preceding table to complete the following table. (Note: Use 365 days as the length of a year in all calculations, and round all values to two decimal places.) Value Inventory Conversion Period Average collection periodO Payables Deferral Period Cash conversion cycle Both the inventory conversion period and payables deferral period use the average daily CoGS in their denominators, whereas the average collection period uses average daily sales in its denominator. Why do these measures use different inputs? O Inventory and accounts payable are carried at cost on the balance sheet, whereas accounts receivable are recorded at the price at which goods are sold. O Current assets should be divided by sales, but current liabilities should be divided by the CoGS

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts