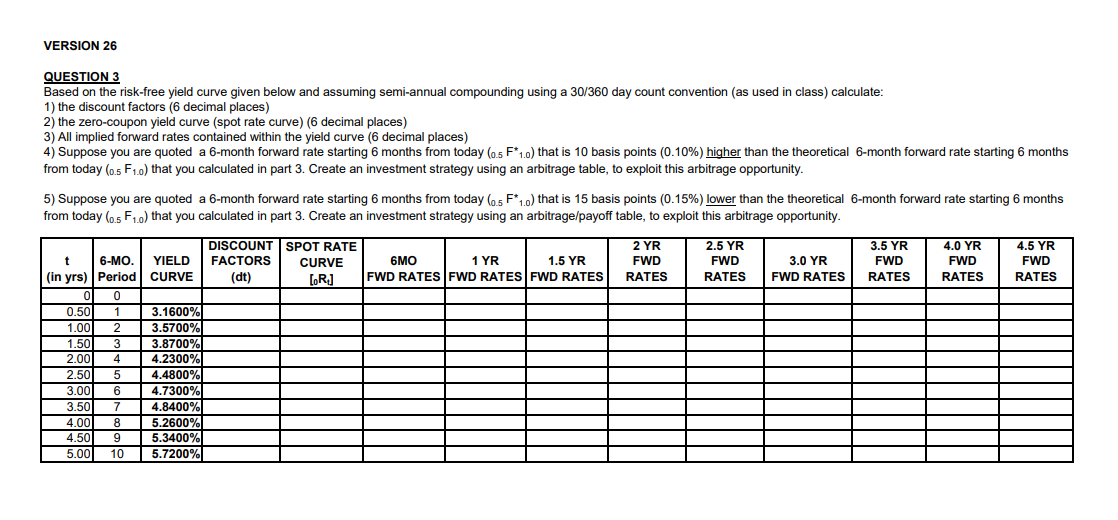

Question: VERSION 26 QUESTION 3 Based on the risk-free yield curve given below and assuming semi-annual compounding using a 30/360 day count convention (as used in

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts