Vhembe Engineering Ltd is a company based in Thohoyandou. It tenders for various size contracts in most

Question:

Vhembe Engineering Ltd is a company based in Thohoyandou. It tenders for various size contracts in most parts of South Africa.

It has recently successfully tendered for a Local Authority contract in Makhado in the Limpopo province. Work is due to begin in January next year. The price that the company submitted with which it won its bid was R432 000 000.

The company has also been requested to undertake another contract in Bela Bela in the Limpopo province. The price that has been offered for this work is R528 000 000. However, due to staffing problems, the two contracts cannot both be carried out at the same time. Vhembe Engineering has to choose which is the most financially rewarding to the company.

Phumelela is able to withdraw from the contract in Mangaung, thanks to a clause that was written into the contract before it was signed. However, if this is done the company would have to notify the Local Authority of its intention by October this year and pay a penalty clause of R42 000 000.

Currently, Vhembe Engineering Ltd has an existing contract in Mangaung from which it receives a rental income of R9 000 000. If it chooses the Makhado contract, the company it will keep the Mangaung contract; however, the Mangaung and Bela Bela contracts are mutually exclusive. Vhembe Engineering Ltd is able to withdraw from the contract in Mangaung, thanks to a clause that was written into the contract before it was signed. However, if this is done the company would have to notify the Local Authority of its intention by October this year and pay a penalty clause of R42 000 000.

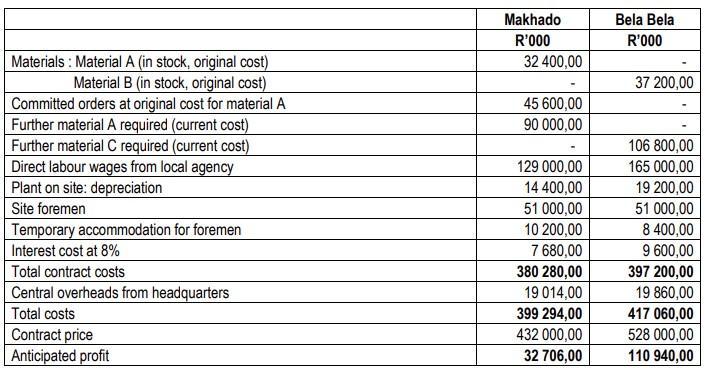

The following estimates relating to the costs and revenue of each contract have been compiled:

Additional information is as follows:

1. Material A does not have a resale value outside of the company, as it is not used commonly in the engineering industry. It could be used as a substitute for another material which currently costs 10% less than the original cost of material A.

2. The price for material B has increased to twice the amount at which it was first purchased. Material B can be resold at its current market price, in which case the costs of disposal are 12% of the selling price. If not sold, any material B could be used on any future contracts as it does not deteriorate.

3. The plant that would be required is common to both contracts. If it were used on the Bela Bela contract, all of the plant would be required due to the nature of the work to be undertaken. However, if the Makhado contract goes ahead, less plant will be required. The plant that is not used will be rented to a neighbouring business for a total rental of R9 000 000 during the period of the contract.

4. The interest charge of 8% relates to a notional charge for working capital that may be required during the period of the contract. The customer would pay the company progress payments according to the work completed.

5. Both contracts would run for a 12-month period.

6. Site foremen are paid an annual salary. This does not vary according to the amount of work undertaken. They will, however, be expected to stay in temporary accommodation near the contract site. The accommodation costs have been estimated based on past experience.

7. The costs of the central headquarters consist of the salaries of the personnel who work in the administration and payroll departments, which amount to R162 000 000 in total. The headquarters supervise approximately 15 contracts at any one time.

8. It is not expected that labor will be in short supply.

Required:

Making use of the principles of relevant costing, prepare a statement that compares the relevant net benefits of the two contracts in Rand terms and concludes

Expert Answer:

Applying International Financial Reporting Standards

ISBN: 978-0730302124

3rd edition

Authors: Keith Alfredson, Ken Leo, Ruth Picker, Paul Pacter, Jennie Radford Victoria Wise