Question: VI Investment U =[ e Bt_[c(t) 1-0/1-0] dt ( t= 0 tot = infinity.) VI Investment U 1-6/1-01 dt ( t= 0 to t =

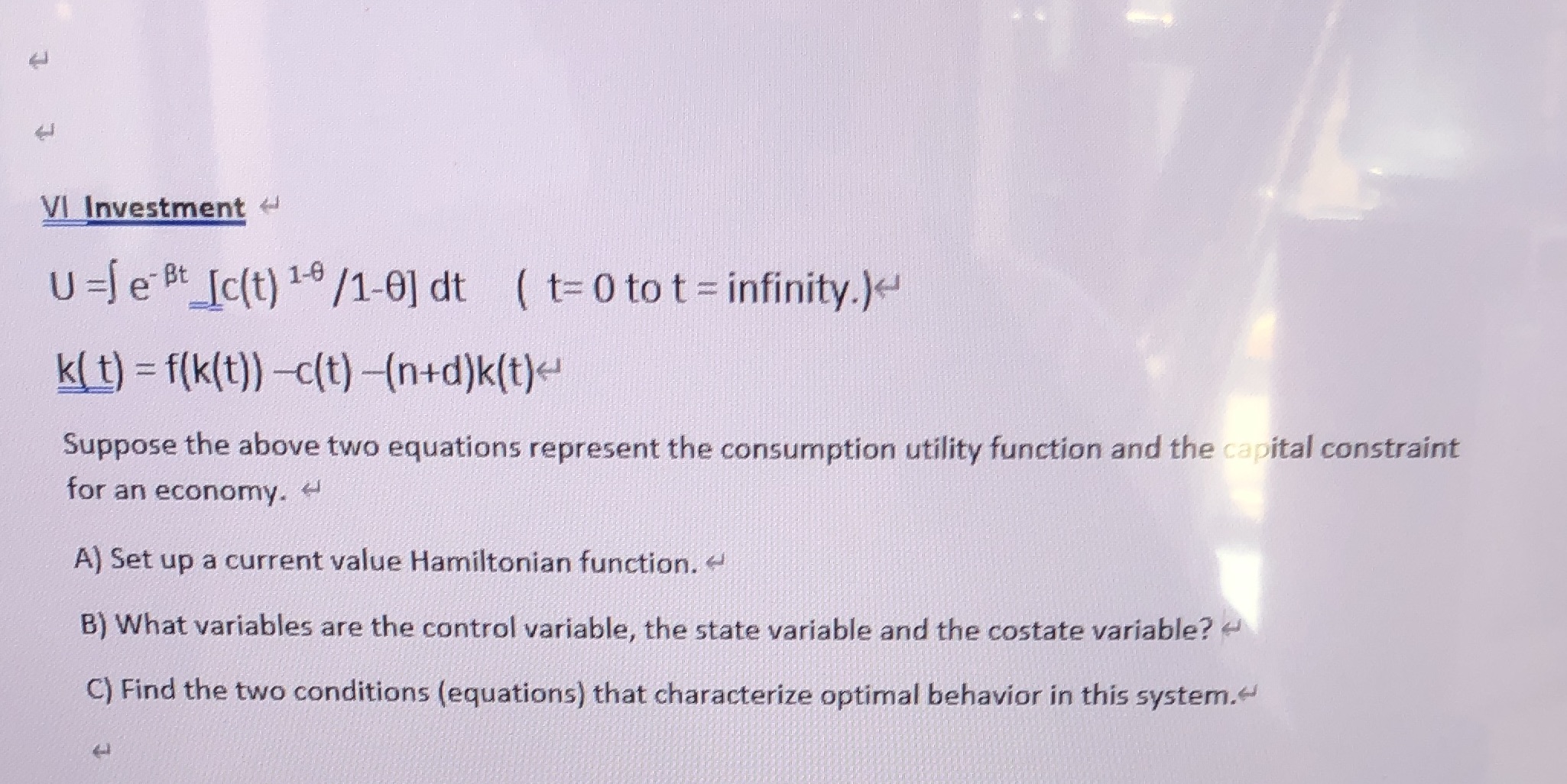

VI Investment U =[ e Bt_[c(t) 1-0/1-0] dt ( t= 0 tot = infinity.)

VI Investment U 1-6/1-01 dt ( t= 0 to t = infinity.)e Suppose the above two equations represent the consumption utility function and the for an economy. e A) Set up a current value Hamiltonian function. B) What variables are the control variable, the state variable and the costate variable? C) Find the two conditions (equations) that characterize optimal behavior in this system.e ital constraint

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock