Positive Ltd (Positive) acquired an 80% stake in Strong Ltd (Strong) on 1 January 20x1. The...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

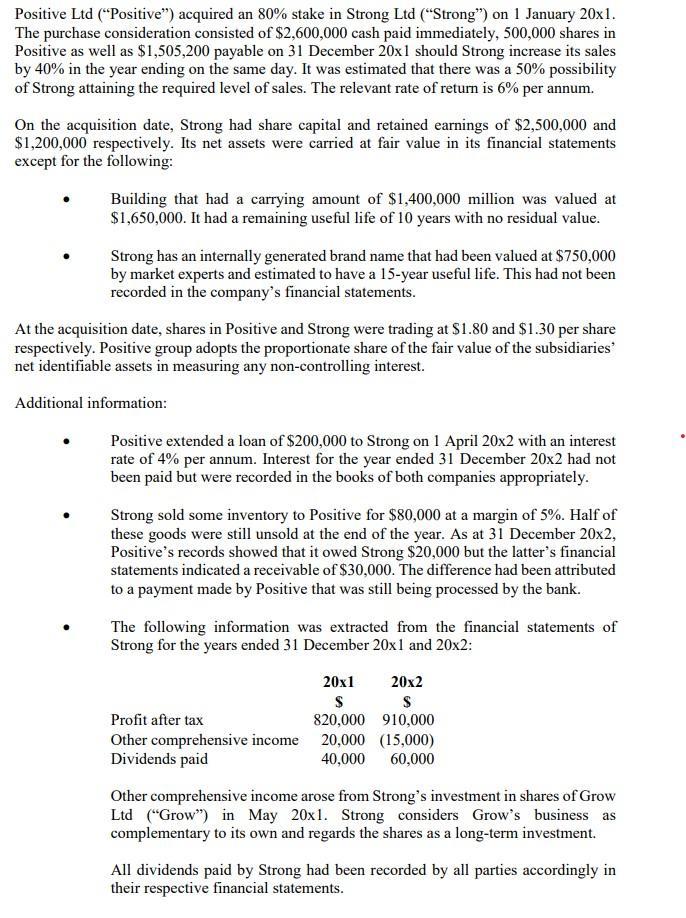

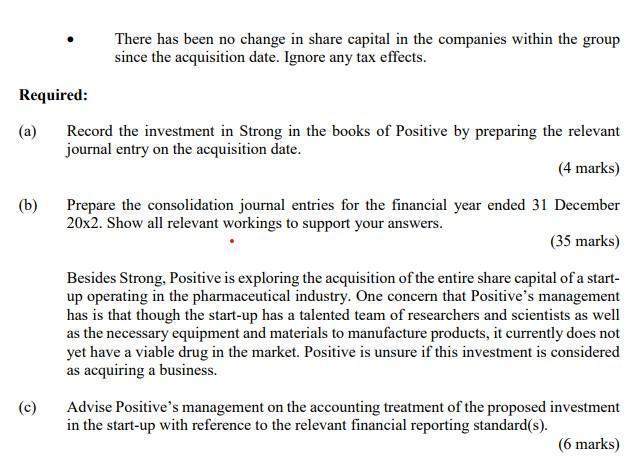

Positive Ltd ("Positive") acquired an 80% stake in Strong Ltd ("Strong") on 1 January 20x1. The purchase consideration consisted of $2,600,000 cash paid immediately, 500,000 shares in Positive as well as $1,505,200 payable on 31 December 20x1 should Strong increase its sales by 40% in the year ending on the same day. It was estimated that there was a 50% possibility of Strong attaining the required level of sales. The relevant rate of return is 6% per annum. On the acquisition date, Strong had share capital and retained earnings of $2,500,000 and $1,200,000 respectively. Its net assets were carried at fair value in its financial statements except for the following: Building that had a carrying amount of $1,400,000 million was valued at $1,650,000. It had a remaining useful life of 10 years with no residual value. Strong has an internally generated brand name that had been valued at $750,000 by market experts and estimated to have a 15-year useful life. This had not been recorded in the company's financial statements. At the acquisition date, shares in Positive and Strong were trading at $1.80 and $1.30 per share respectively. Positive group adopts the proportionate share of the fair value of the subsidiaries' net identifiable assets in measuring any non-controlling interest. Additional information: Positive extended a loan of $200,000 to Strong on 1 April 20x2 with an interest rate of 4% per annum. Interest for the year ended 31 December 20x2 had not been paid but were recorded in the books of both companies appropriately. Strong sold some inventory to Positive for $80,000 at a margin of 5%. Half of these goods were still unsold at the end of the year. As at 31 December 20x2, Positive's records showed that it owed Strong $20,000 but the latter's financial statements indicated a receivable of $30,000. The difference had been attributed to a payment made by Positive that was still being processed by the bank. The following information was extracted from the financial statements of Strong for the years ended 31 December 20x1 and 20x2: 20x1 S 820,000 Profit after tax Other comprehensive income 20,000 Dividends paid 20x2 S 910,000 (15,000) 40,000 60,000 Other comprehensive income arose from Strong's investment in shares of Grow Ltd ("Grow") in May 20x1. Strong considers Grow's business as complementary to its own and regards the shares as a long-term investment. All dividends paid by Strong had been recorded by all parties accordingly in their respective financial statements. Required: (a) (b) There has been no change in share capital in the companies within the group since the acquisition date. Ignore any tax effects. Record the investment in Strong in the books of Positive by preparing the relevant journal entry on the acquisition date. (4 marks) Prepare the consolidation journal entries for the financial year ended 31 December 20x2. Show all relevant workings to support your answers. (35 marks) Besides Strong, Positive is exploring the acquisition of the entire share capital of a start- up operating in the pharmaceutical industry. One concern that Positive's management has is that though the start-up has a talented team of researchers and scientists as well as the necessary equipment and materials to manufacture products, it currently does not yet have a viable drug in the market. Positive is unsure if this investment is considered as acquiring a business. Advise Positive's management on the accounting treatment of the proposed investment in the start-up with reference to the relevant financial reporting standard(s). (6 marks) Positive Ltd ("Positive") acquired an 80% stake in Strong Ltd ("Strong") on 1 January 20x1. The purchase consideration consisted of $2,600,000 cash paid immediately, 500,000 shares in Positive as well as $1,505,200 payable on 31 December 20x1 should Strong increase its sales by 40% in the year ending on the same day. It was estimated that there was a 50% possibility of Strong attaining the required level of sales. The relevant rate of return is 6% per annum. On the acquisition date, Strong had share capital and retained earnings of $2,500,000 and $1,200,000 respectively. Its net assets were carried at fair value in its financial statements except for the following: Building that had a carrying amount of $1,400,000 million was valued at $1,650,000. It had a remaining useful life of 10 years with no residual value. Strong has an internally generated brand name that had been valued at $750,000 by market experts and estimated to have a 15-year useful life. This had not been recorded in the company's financial statements. At the acquisition date, shares in Positive and Strong were trading at $1.80 and $1.30 per share respectively. Positive group adopts the proportionate share of the fair value of the subsidiaries' net identifiable assets in measuring any non-controlling interest. Additional information: Positive extended a loan of $200,000 to Strong on 1 April 20x2 with an interest rate of 4% per annum. Interest for the year ended 31 December 20x2 had not been paid but were recorded in the books of both companies appropriately. Strong sold some inventory to Positive for $80,000 at a margin of 5%. Half of these goods were still unsold at the end of the year. As at 31 December 20x2, Positive's records showed that it owed Strong $20,000 but the latter's financial statements indicated a receivable of $30,000. The difference had been attributed to a payment made by Positive that was still being processed by the bank. The following information was extracted from the financial statements of Strong for the years ended 31 December 20x1 and 20x2: 20x1 S 820,000 Profit after tax Other comprehensive income 20,000 Dividends paid 20x2 S 910,000 (15,000) 40,000 60,000 Other comprehensive income arose from Strong's investment in shares of Grow Ltd ("Grow") in May 20x1. Strong considers Grow's business as complementary to its own and regards the shares as a long-term investment. All dividends paid by Strong had been recorded by all parties accordingly in their respective financial statements. Required: (a) (b) There has been no change in share capital in the companies within the group since the acquisition date. Ignore any tax effects. Record the investment in Strong in the books of Positive by preparing the relevant journal entry on the acquisition date. (4 marks) Prepare the consolidation journal entries for the financial year ended 31 December 20x2. Show all relevant workings to support your answers. (35 marks) Besides Strong, Positive is exploring the acquisition of the entire share capital of a start- up operating in the pharmaceutical industry. One concern that Positive's management has is that though the start-up has a talented team of researchers and scientists as well as the necessary equipment and materials to manufacture products, it currently does not yet have a viable drug in the market. Positive is unsure if this investment is considered as acquiring a business. Advise Positive's management on the accounting treatment of the proposed investment in the start-up with reference to the relevant financial reporting standard(s). (6 marks)

Expert Answer:

Answer rating: 100% (QA)

a Positives Investment in Strong Particulars Amount Dr Amount Cr Cash at bank 2600000 Share capital 500000 Retained earnings 1200000 Brand name 750000 ... View the full answer

Related Book For

Essentials of Business Statistics Communicating With Numbers

ISBN: 978-0078020544

1st edition

Authors: Sanjiv Jaggia, Alison Kelly

Posted Date:

Students also viewed these accounting questions

-

Students who graduated from college in 2010 owed an average of $25,250 in student loans (New York Times, November 2, 2011). An economist wants to determine if average debt has changed. She takes a...

-

Suppose you would like to take an SRS of size n from a list of N units, but do not know the population size N in advance. Consider the following procedure: 1. Set S0 = {1, 2. . . n}, so that the...

-

Suppose you would like to take an SRS of size n from a list of N units, but do not know the population size N in advance. Consider the following procedure: a. Set S 0 = {1, 2. . . n}, so that the...

-

Use the data given in Table to construct a frequency distribution with a first class (in millions) of 50-99. Novel Copies Sold (millions) Don Quixote . . . . . . . . . . . . . . . . . . . . . . . . ....

-

Let X have the negative binomial distribution with parameters n and 0.2, where n is a large integer. a. Explain why one can use the central limit theorem to approximate the distribution of X by a...

-

Raiders Ltd is a private limited company financed entirely by ordinary shares. Its effective cost of capital, net of tax, is 10 per cent p.a. The directors are considering the company's capital...

-

The activity of component \(i\) can be written as (a) \(a_{i}=\frac{f_{i}^{0}}{f_{i}}\) (b) \(a_{i}=\frac{f_{i}}{f_{i}^{0}}\) (c) \(a_{i}=\ln \left(\frac{f_{i}}{f_{i}^{0}} ight)\) (d) \(a_{i}=\ln...

-

A fuel gas containing 86% methane, 8% ethane, and 6% propane by volume flows to a furnace at a rate of 1450 m 3 /h at 15C and 150 kPa (gauge), where it is burned with 8% excess air. Calculate the...

-

Compute the EPS and ROE Equity: Issue 85,000 common shares with a current market price of $15 each. Debt: Take on $1,275,000 of debt with a 4.5% interest and $181,000 principle payments annually...

-

Your company is considering investing in its own transport fleet. The present position is that carriage is contracted to an outside organization. The life of the transport fleet would be five years,...

-

In Fig. 6-14, a mass of 30 kg Is supported by a compression member CD and two tension members AC and BC. CD makes an angle of 400 with the wall. A, B, and Care in a horizontal .plane. AEEB-1000 mm....

-

You have had some time to organize your management team and make decisions for your firm, it is time to report to the board of directors. All members of the team should contribute to the report's...

-

In regard to section 32 of the Sale of Land Act 1962 (VIC), which part of it will apply for a scenario when a purchaser found out the property he's bought and awaiting settlement is smaller than...

-

dz where c is Evaluate J The circle C 22 (2-1)(2-2) 121=0.5.

-

Why was the rate of inflation in the uk relatively low in the 1950's? Explain 4 policies that occurred in the UK that helped inflation to be low.

-

UNIFOR service collective agreement UNIFOR tech collective agreement Take this two collective agreement and review the articles under scheduling, hours of work and vacation scheduling. Identify the...

-

Overview Take a minute to reflect on the process of creating an operating budget for a large early childhood program. This is also a good opportunity to ask your peer's questions to seek clarity on...

-

Distinguish among total-moisture content, free-moisture content, equilibrium-moisture content, unbound moisture, and bound moisture.

-

Go to www.finance.yahoo.com/ to get a current stock quote for Google, Inc. (ticker symbol 5 GOOG). Then, click on historical prices to record the monthly adjusted close price of Google stock in 2010....

-

Find the following probabilities based on the standard normal variable Z. a. P(-0.67 Z 20.23) b. P (0 Z 1.96) c. P(-1.28 Z 0) d. P (Z <4.2)

-

A recent survey asked 5,324 individuals: Whats most important to you when choosing where to live? The responses are shown in the following relative frequency distribution. Response .....Relative...

-

What are the different methods of conducting marketing research?

-

What are some of the reasons for the increased need for marketing research?

-

Discuss an ethical issue in marketing research that relates to each of the following stakeholders: (1) client, (2) the supplier, and (3) the respondent.

Study smarter with the SolutionInn App