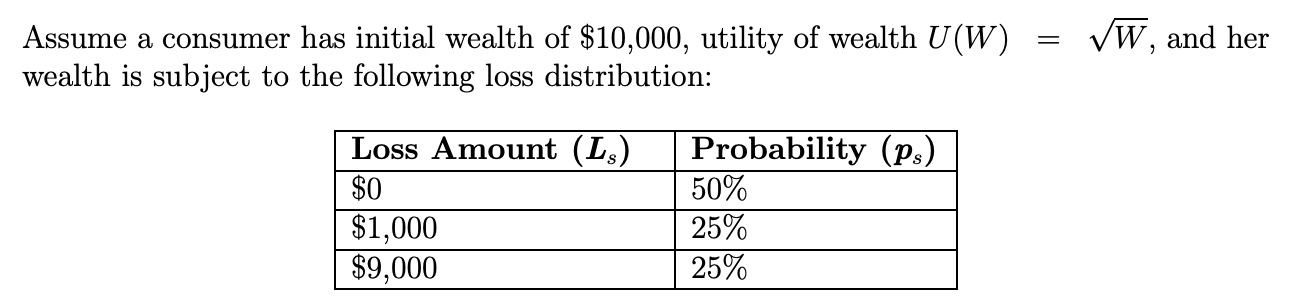

Question: VW , and her Assume a consumer has initial wealth of $10,000, utility of wealth U(W) wealth is subject to the following loss distribution: Loss

VW , and her Assume a consumer has initial wealth of $10,000, utility of wealth U(W) wealth is subject to the following loss distribution: Loss Amount (L5) $0 $1,000 $9,000 Probability (ps) 50% 25% 25% Determine the expected utility of wealth, assuming the consumer is uninsured. Calculate the actuarially fair price for a full (100%) coverage insurance policy. VW , and her Assume a consumer has initial wealth of $10,000, utility of wealth U(W) wealth is subject to the following loss distribution: Loss Amount (L5) $0 $1,000 $9,000 Probability (ps) 50% 25% 25% Determine the expected utility of wealth, assuming the consumer is uninsured. Calculate the actuarially fair price for a full (100%) coverage insurance policy

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts