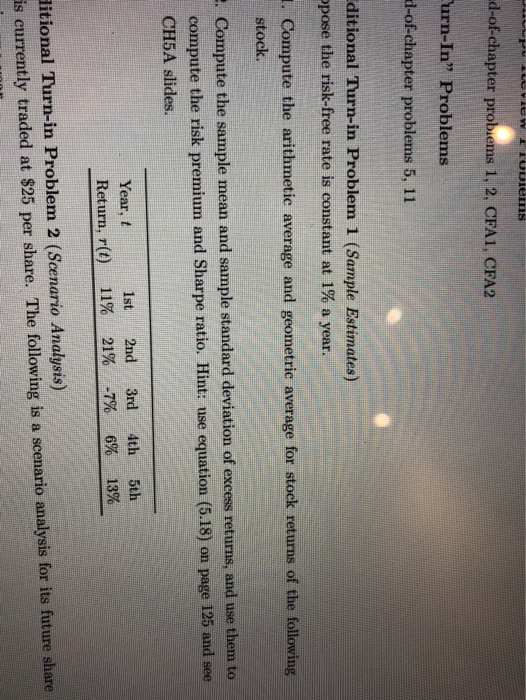

Question: VW TODiens d-of-chapter problems 1, 2, CFA1, CFA2 urn-In Problems d-of-chapter problems 5, 11 ditional Turn-in Problem 1 (Sample Estimates) pose the risk-free rate is

VW TODiens d-of-chapter problems 1, 2, CFA1, CFA2 urn-In Problems d-of-chapter problems 5, 11 ditional Turn-in Problem 1 (Sample Estimates) pose the risk-free rate is constant at 1% a year. 1. Compute the arithmetic average and geometrie average for stock returns of the following stock. . Compute the sample mean and sample standard deviation of excess returns, and use them to compute the risk premium and Sharpe ratio. Hint: use equation (5.18) on page 125 and see CH5A slides. Year, t Return, r(t) 1st 11% 2nd 21% 3rd -7% 4th 6% 5th 13% ditional Turn-in Problem 2 (Scenario Analysis) is currently traded at $25 per share. The following is a scenario analysis for its future share

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts