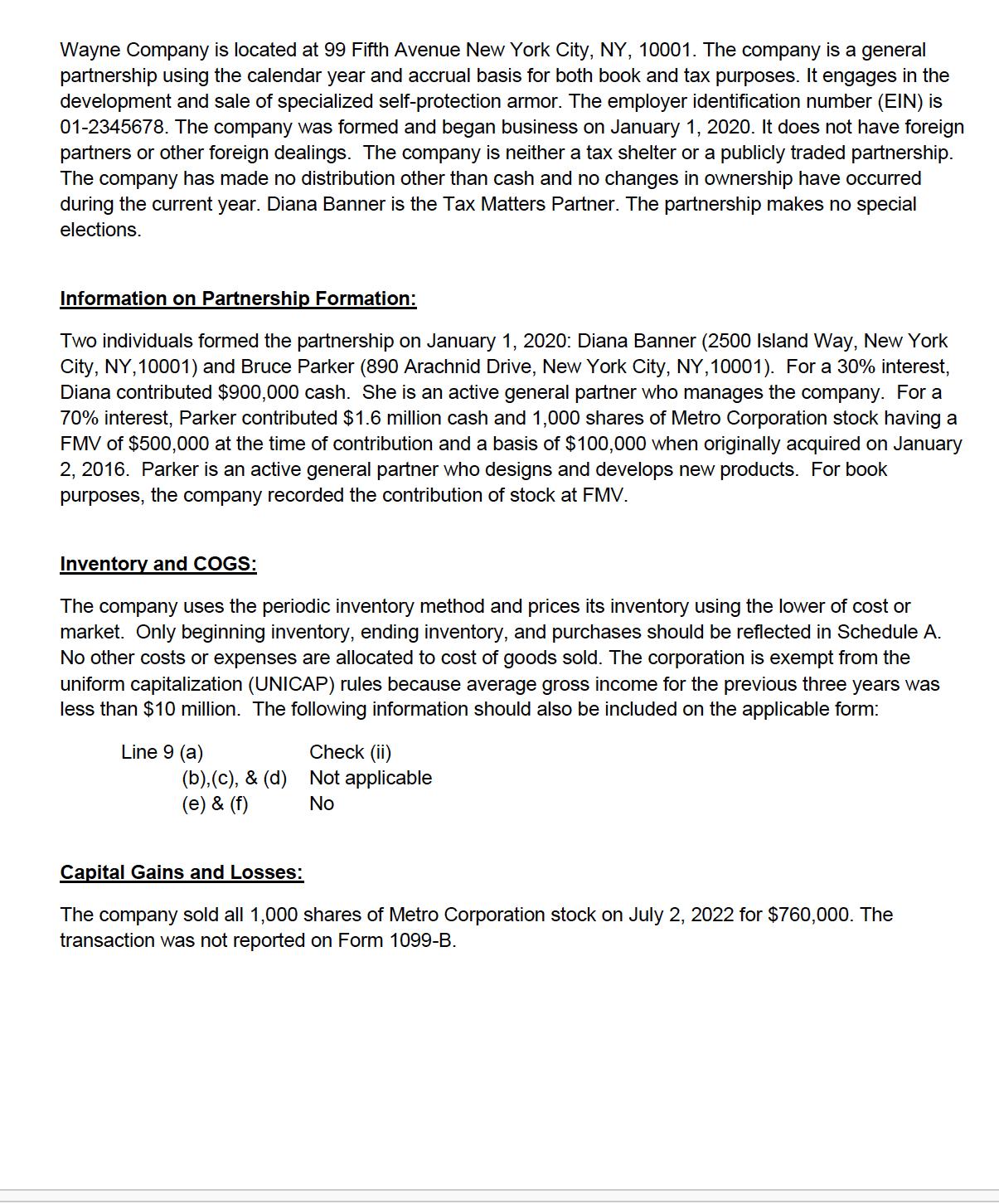

Wayne Company is located at 99 Fifth Avenue New York City, NY, 10001. The company is...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

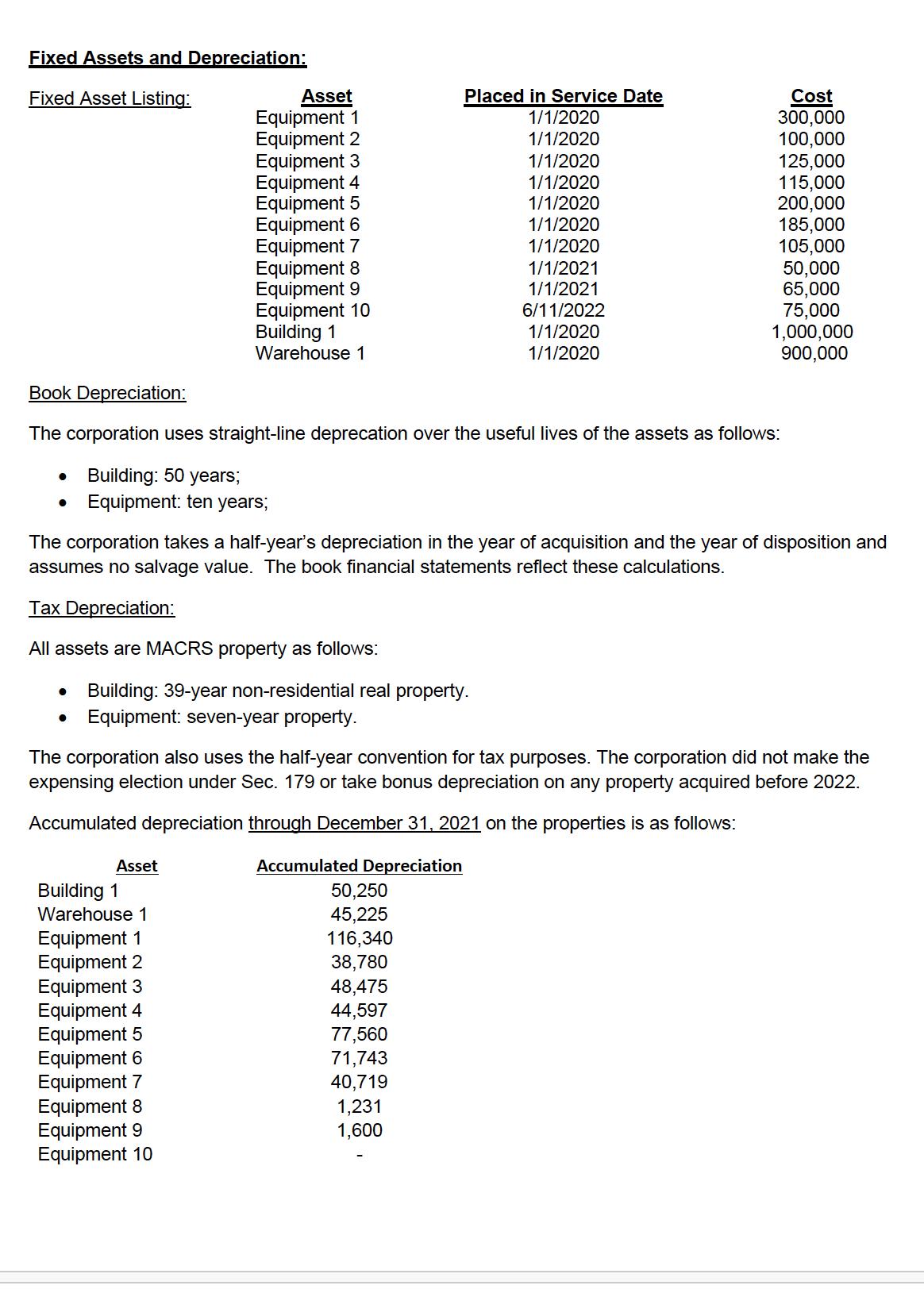

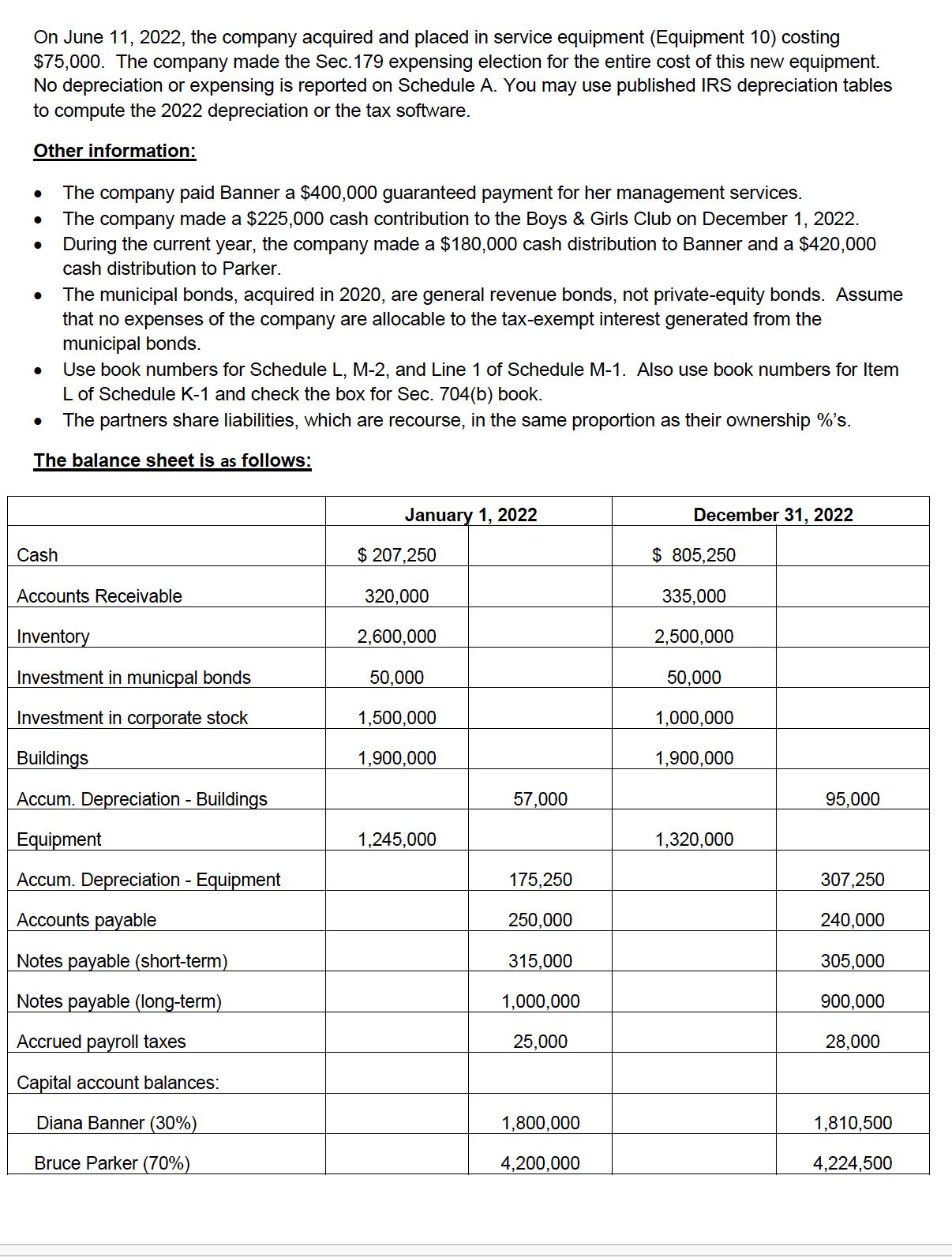

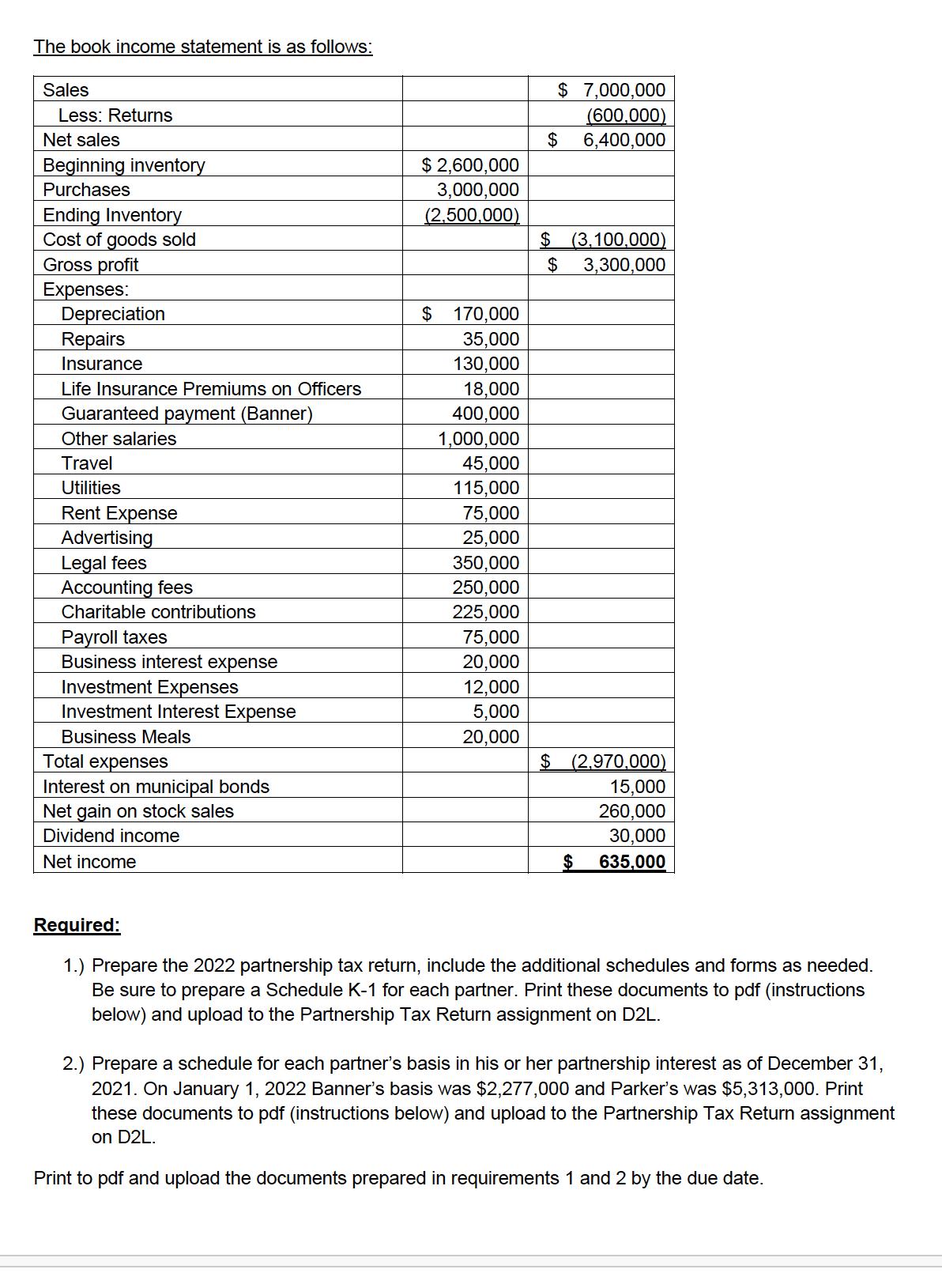

Wayne Company is located at 99 Fifth Avenue New York City, NY, 10001. The company is a general partnership using the calendar year and accrual basis for both book and tax purposes. It engages in the development and sale of specialized self-protection armor. The employer identification number (EIN) is 01-2345678. The company was formed and began business on January 1, 2020. It does not have foreign partners or other foreign dealings. The company is neither a tax shelter or a publicly traded partnership. The company has made no distribution other than cash and no changes in ownership have occurred during the current year. Diana Banner is the Tax Matters Partner. The partnership makes no special elections. Information on Partnership Formation: Two individuals formed the partnership on January 1, 2020: Diana Banner (2500 Island Way, New York City, NY, 10001) and Bruce Parker (890 Arachnid Drive, New York City, NY, 10001). For a 30% interest, Diana contributed $900,000 cash. She is an active general partner who manages the company. For a 70% interest, Parker contributed $1.6 million cash and 1,000 shares of Metro Corporation stock having a FMV of $500,000 at the time of contribution and a basis of $100,000 when originally acquired on January 2, 2016. Parker is an active general partner who designs and develops new products. For book purposes, the company recorded the contribution of stock at FMV. Inventory and COGS: The company uses the periodic inventory method and prices its inventory using the lower of cost or market. Only beginning inventory, ending inventory, and purchases should be reflected in Schedule A. No other costs or expenses are allocated to cost of goods sold. The corporation is exempt from the uniform capitalization (UNICAP) rules because average gross income for the previous three years was less than $10 million. The following information should also be included on the applicable form: Line 9 (a) (b), (c), & (d) (e) & (f) Check (ii) Not applicable No Capital Gains and Losses: The company sold all 1,000 shares of Metro Corporation stock on July 2, 2022 for $760,000. The transaction was not reported on Form 1099-B. Fixed Assets and Depreciation: Fixed Asset Listing: Asset Equipment 1 Placed in Service Date Cost 1/1/2020 300,000 Equipment 2 1/1/2020 100,000 Equipment 3 1/1/2020 125,000 Equipment 4 1/1/2020 115,000 Equipment 5 1/1/2020 200,000 Equipment 6 1/1/2020 185,000 Equipment 7 1/1/2020 105,000 Equipment 8 1/1/2021 50,000 Equipment 9 1/1/2021 65,000 Equipment 10 6/11/2022 Building 1 1/1/2020 Warehouse 1 1/1/2020 75,000 1,000,000 900,000 Book Depreciation: The corporation uses straight-line deprecation over the useful lives of the assets as follows: • Building: 50 years; • Equipment: ten years; The corporation takes a half-year's depreciation in the year of acquisition and the year of disposition and assumes no salvage value. The book financial statements reflect these calculations. Tax Depreciation: All assets are MACRS property as follows: • Building: 39-year non-residential real property. Equipment: seven-year property. The corporation also uses the half-year convention for tax purposes. The corporation did not make the expensing election under Sec. 179 or take bonus depreciation on any property acquired before 2022. Accumulated depreciation through December 31, 2021 on the properties is as follows: Asset Accumulated Depreciation Building 1 50,250 Warehouse 1 45,225 Equipment 1 116,340 Equipment 2 38,780 Equipment 3 48,475 Equipment 4 44,597 Equipment 5 77,560 Equipment 6 71,743 Equipment 7 40,719 Equipment 8 1,231 Equipment 9 1,600 Equipment 10 On June 11, 2022, the company acquired and placed in service equipment (Equipment 10) costing $75,000. The company made the Sec. 179 expensing election for the entire cost of this new equipment. No depreciation or expensing is reported on Schedule A. You may use published IRS depreciation tables to compute the 2022 depreciation or the tax software. Other information: • The company paid Banner a $400,000 guaranteed payment for her management services. • • The company made a $225,000 cash contribution to the Boys & Girls Club on December 1, 2022. During the current year, the company made a $180,000 cash distribution to Banner and a $420,000 cash distribution to Parker. • The municipal bonds, acquired in 2020, are general revenue bonds, not private-equity bonds. Assume that no expenses of the company are allocable to the tax-exempt interest generated from the municipal bonds. • Use book numbers for Schedule L, M-2, and Line 1 of Schedule M-1. Also use book numbers for Item L of Schedule K-1 and check the box for Sec. 704(b) book. · The partners share liabilities, which are recourse, in the same proportion as their ownership %'s. The balance sheet is as follows: January 1, 2022 December 31, 2022 Cash $ 207,250 $ 805,250 Accounts Receivable 320,000 Inventory 2,600,000 Investment in municpal bonds 50,000 335,000 2,500,000 50,000 Investment in corporate stock 1,500,000 1,000,000 Buildings 1,900,000 1,900,000 Accum. Depreciation - Buildings 57,000 95,000 Equipment 1,245,000 1,320,000 Accum. Depreciation - Equipment 175,250 307,250 Accounts payable 250,000 240,000 Notes payable (short-term) 315,000 305,000 Notes payable (long-term) 1,000,000 900,000 Accrued payroll taxes 25,000 28,000 Capital account balances: Diana Banner (30%) 1,800,000 1,810,500 Bruce Parker (70%) 4,200,000 4,224,500 The book income statement is as follows: Sales Less: Returns Net sales Beginning inventory Purchases Ending Inventory Cost of goods sold Gross profit Expenses: Depreciation $ $ 2,600,000 3,000,000 (2,500,000) $ 7,000,000 (600,000) 6,400,000 $ (3,100,000) $ 3,300,000 $ 170,000 Repairs 35,000 Insurance 130,000 Life Insurance Premiums on Officers 18,000 Guaranteed payment (Banner) 400,000 Other salaries 1,000,000 Travel 45,000 Utilities 115,000 Rent Expense 75,000 Advertising Legal fees 25,000 350,000 Accounting fees 250,000 Charitable contributions 225,000 Payroll taxes 75,000 Business interest expense 20,000 Investment Expenses 12,000 Investment Interest Expense 5,000 Business Meals 20,000 Total expenses $ (2,970,000) Interest on municipal bonds 15,000 Net gain on stock sales 260,000 Dividend income Net income Required: 30,000 $ 635,000 1.) Prepare the 2022 partnership tax return, include the additional schedules and forms as needed. Be sure to prepare a Schedule K-1 for each partner. Print these documents to pdf (instructions below) and upload to the Partnership Tax Return assignment on D2L. 2.) Prepare a schedule for each partner's basis in his or her partnership interest as of December 31, 2021. On January 1, 2022 Banner's basis was $2,277,000 and Parker's was $5,313,000. Print these documents to pdf (instructions below) and upload to the Partnership Tax Return assignment on D2L. Print to pdf and upload the documents prepared in requirements 1 and 2 by the due date. Wayne Company is located at 99 Fifth Avenue New York City, NY, 10001. The company is a general partnership using the calendar year and accrual basis for both book and tax purposes. It engages in the development and sale of specialized self-protection armor. The employer identification number (EIN) is 01-2345678. The company was formed and began business on January 1, 2020. It does not have foreign partners or other foreign dealings. The company is neither a tax shelter or a publicly traded partnership. The company has made no distribution other than cash and no changes in ownership have occurred during the current year. Diana Banner is the Tax Matters Partner. The partnership makes no special elections. Information on Partnership Formation: Two individuals formed the partnership on January 1, 2020: Diana Banner (2500 Island Way, New York City, NY, 10001) and Bruce Parker (890 Arachnid Drive, New York City, NY, 10001). For a 30% interest, Diana contributed $900,000 cash. She is an active general partner who manages the company. For a 70% interest, Parker contributed $1.6 million cash and 1,000 shares of Metro Corporation stock having a FMV of $500,000 at the time of contribution and a basis of $100,000 when originally acquired on January 2, 2016. Parker is an active general partner who designs and develops new products. For book purposes, the company recorded the contribution of stock at FMV. Inventory and COGS: The company uses the periodic inventory method and prices its inventory using the lower of cost or market. Only beginning inventory, ending inventory, and purchases should be reflected in Schedule A. No other costs or expenses are allocated to cost of goods sold. The corporation is exempt from the uniform capitalization (UNICAP) rules because average gross income for the previous three years was less than $10 million. The following information should also be included on the applicable form: Line 9 (a) (b), (c), & (d) (e) & (f) Check (ii) Not applicable No Capital Gains and Losses: The company sold all 1,000 shares of Metro Corporation stock on July 2, 2022 for $760,000. The transaction was not reported on Form 1099-B. Fixed Assets and Depreciation: Fixed Asset Listing: Asset Equipment 1 Placed in Service Date Cost 1/1/2020 300,000 Equipment 2 1/1/2020 100,000 Equipment 3 1/1/2020 125,000 Equipment 4 1/1/2020 115,000 Equipment 5 1/1/2020 200,000 Equipment 6 1/1/2020 185,000 Equipment 7 1/1/2020 105,000 Equipment 8 1/1/2021 50,000 Equipment 9 1/1/2021 65,000 Equipment 10 6/11/2022 Building 1 1/1/2020 Warehouse 1 1/1/2020 75,000 1,000,000 900,000 Book Depreciation: The corporation uses straight-line deprecation over the useful lives of the assets as follows: • Building: 50 years; • Equipment: ten years; The corporation takes a half-year's depreciation in the year of acquisition and the year of disposition and assumes no salvage value. The book financial statements reflect these calculations. Tax Depreciation: All assets are MACRS property as follows: • Building: 39-year non-residential real property. Equipment: seven-year property. The corporation also uses the half-year convention for tax purposes. The corporation did not make the expensing election under Sec. 179 or take bonus depreciation on any property acquired before 2022. Accumulated depreciation through December 31, 2021 on the properties is as follows: Asset Accumulated Depreciation Building 1 50,250 Warehouse 1 45,225 Equipment 1 116,340 Equipment 2 38,780 Equipment 3 48,475 Equipment 4 44,597 Equipment 5 77,560 Equipment 6 71,743 Equipment 7 40,719 Equipment 8 1,231 Equipment 9 1,600 Equipment 10 On June 11, 2022, the company acquired and placed in service equipment (Equipment 10) costing $75,000. The company made the Sec. 179 expensing election for the entire cost of this new equipment. No depreciation or expensing is reported on Schedule A. You may use published IRS depreciation tables to compute the 2022 depreciation or the tax software. Other information: • The company paid Banner a $400,000 guaranteed payment for her management services. • • The company made a $225,000 cash contribution to the Boys & Girls Club on December 1, 2022. During the current year, the company made a $180,000 cash distribution to Banner and a $420,000 cash distribution to Parker. • The municipal bonds, acquired in 2020, are general revenue bonds, not private-equity bonds. Assume that no expenses of the company are allocable to the tax-exempt interest generated from the municipal bonds. • Use book numbers for Schedule L, M-2, and Line 1 of Schedule M-1. Also use book numbers for Item L of Schedule K-1 and check the box for Sec. 704(b) book. · The partners share liabilities, which are recourse, in the same proportion as their ownership %'s. The balance sheet is as follows: January 1, 2022 December 31, 2022 Cash $ 207,250 $ 805,250 Accounts Receivable 320,000 Inventory 2,600,000 Investment in municpal bonds 50,000 335,000 2,500,000 50,000 Investment in corporate stock 1,500,000 1,000,000 Buildings 1,900,000 1,900,000 Accum. Depreciation - Buildings 57,000 95,000 Equipment 1,245,000 1,320,000 Accum. Depreciation - Equipment 175,250 307,250 Accounts payable 250,000 240,000 Notes payable (short-term) 315,000 305,000 Notes payable (long-term) 1,000,000 900,000 Accrued payroll taxes 25,000 28,000 Capital account balances: Diana Banner (30%) 1,800,000 1,810,500 Bruce Parker (70%) 4,200,000 4,224,500 The book income statement is as follows: Sales Less: Returns Net sales Beginning inventory Purchases Ending Inventory Cost of goods sold Gross profit Expenses: Depreciation $ $ 2,600,000 3,000,000 (2,500,000) $ 7,000,000 (600,000) 6,400,000 $ (3,100,000) $ 3,300,000 $ 170,000 Repairs 35,000 Insurance 130,000 Life Insurance Premiums on Officers 18,000 Guaranteed payment (Banner) 400,000 Other salaries 1,000,000 Travel 45,000 Utilities 115,000 Rent Expense 75,000 Advertising Legal fees 25,000 350,000 Accounting fees 250,000 Charitable contributions 225,000 Payroll taxes 75,000 Business interest expense 20,000 Investment Expenses 12,000 Investment Interest Expense 5,000 Business Meals 20,000 Total expenses $ (2,970,000) Interest on municipal bonds 15,000 Net gain on stock sales 260,000 Dividend income Net income Required: 30,000 $ 635,000 1.) Prepare the 2022 partnership tax return, include the additional schedules and forms as needed. Be sure to prepare a Schedule K-1 for each partner. Print these documents to pdf (instructions below) and upload to the Partnership Tax Return assignment on D2L. 2.) Prepare a schedule for each partner's basis in his or her partnership interest as of December 31, 2021. On January 1, 2022 Banner's basis was $2,277,000 and Parker's was $5,313,000. Print these documents to pdf (instructions below) and upload to the Partnership Tax Return assignment on D2L. Print to pdf and upload the documents prepared in requirements 1 and 2 by the due date. Wayne Company is located at 99 Fifth Avenue New York City, NY, 10001. The company is a general partnership using the calendar year and accrual basis for both book and tax purposes. It engages in the development and sale of specialized self-protection armor. The employer identification number (EIN) is 01-2345678. The company was formed and began business on January 1, 2020. It does not have foreign partners or other foreign dealings. The company is neither a tax shelter or a publicly traded partnership. The company has made no distribution other than cash and no changes in ownership have occurred during the current year. Diana Banner is the Tax Matters Partner. The partnership makes no special elections. Information on Partnership Formation: Two individuals formed the partnership on January 1, 2020: Diana Banner (2500 Island Way, New York City, NY, 10001) and Bruce Parker (890 Arachnid Drive, New York City, NY, 10001). For a 30% interest, Diana contributed $900,000 cash. She is an active general partner who manages the company. For a 70% interest, Parker contributed $1.6 million cash and 1,000 shares of Metro Corporation stock having a FMV of $500,000 at the time of contribution and a basis of $100,000 when originally acquired on January 2, 2016. Parker is an active general partner who designs and develops new products. For book purposes, the company recorded the contribution of stock at FMV. Inventory and COGS: The company uses the periodic inventory method and prices its inventory using the lower of cost or market. Only beginning inventory, ending inventory, and purchases should be reflected in Schedule A. No other costs or expenses are allocated to cost of goods sold. The corporation is exempt from the uniform capitalization (UNICAP) rules because average gross income for the previous three years was less than $10 million. The following information should also be included on the applicable form: Line 9 (a) (b), (c), & (d) (e) & (f) Check (ii) Not applicable No Capital Gains and Losses: The company sold all 1,000 shares of Metro Corporation stock on July 2, 2022 for $760,000. The transaction was not reported on Form 1099-B. Fixed Assets and Depreciation: Fixed Asset Listing: Asset Equipment 1 Placed in Service Date Cost 1/1/2020 300,000 Equipment 2 1/1/2020 100,000 Equipment 3 1/1/2020 125,000 Equipment 4 1/1/2020 115,000 Equipment 5 1/1/2020 200,000 Equipment 6 1/1/2020 185,000 Equipment 7 1/1/2020 105,000 Equipment 8 1/1/2021 50,000 Equipment 9 1/1/2021 65,000 Equipment 10 6/11/2022 Building 1 1/1/2020 Warehouse 1 1/1/2020 75,000 1,000,000 900,000 Book Depreciation: The corporation uses straight-line deprecation over the useful lives of the assets as follows: • Building: 50 years; • Equipment: ten years; The corporation takes a half-year's depreciation in the year of acquisition and the year of disposition and assumes no salvage value. The book financial statements reflect these calculations. Tax Depreciation: All assets are MACRS property as follows: • Building: 39-year non-residential real property. Equipment: seven-year property. The corporation also uses the half-year convention for tax purposes. The corporation did not make the expensing election under Sec. 179 or take bonus depreciation on any property acquired before 2022. Accumulated depreciation through December 31, 2021 on the properties is as follows: Asset Accumulated Depreciation Building 1 50,250 Warehouse 1 45,225 Equipment 1 116,340 Equipment 2 38,780 Equipment 3 48,475 Equipment 4 44,597 Equipment 5 77,560 Equipment 6 71,743 Equipment 7 40,719 Equipment 8 1,231 Equipment 9 1,600 Equipment 10 On June 11, 2022, the company acquired and placed in service equipment (Equipment 10) costing $75,000. The company made the Sec. 179 expensing election for the entire cost of this new equipment. No depreciation or expensing is reported on Schedule A. You may use published IRS depreciation tables to compute the 2022 depreciation or the tax software. Other information: • The company paid Banner a $400,000 guaranteed payment for her management services. • • The company made a $225,000 cash contribution to the Boys & Girls Club on December 1, 2022. During the current year, the company made a $180,000 cash distribution to Banner and a $420,000 cash distribution to Parker. • The municipal bonds, acquired in 2020, are general revenue bonds, not private-equity bonds. Assume that no expenses of the company are allocable to the tax-exempt interest generated from the municipal bonds. • Use book numbers for Schedule L, M-2, and Line 1 of Schedule M-1. Also use book numbers for Item L of Schedule K-1 and check the box for Sec. 704(b) book. · The partners share liabilities, which are recourse, in the same proportion as their ownership %'s. The balance sheet is as follows: January 1, 2022 December 31, 2022 Cash $ 207,250 $ 805,250 Accounts Receivable 320,000 Inventory 2,600,000 Investment in municpal bonds 50,000 335,000 2,500,000 50,000 Investment in corporate stock 1,500,000 1,000,000 Buildings 1,900,000 1,900,000 Accum. Depreciation - Buildings 57,000 95,000 Equipment 1,245,000 1,320,000 Accum. Depreciation - Equipment 175,250 307,250 Accounts payable 250,000 240,000 Notes payable (short-term) 315,000 305,000 Notes payable (long-term) 1,000,000 900,000 Accrued payroll taxes 25,000 28,000 Capital account balances: Diana Banner (30%) 1,800,000 1,810,500 Bruce Parker (70%) 4,200,000 4,224,500 The book income statement is as follows: Sales Less: Returns Net sales Beginning inventory Purchases Ending Inventory Cost of goods sold Gross profit Expenses: Depreciation $ $ 2,600,000 3,000,000 (2,500,000) $ 7,000,000 (600,000) 6,400,000 $ (3,100,000) $ 3,300,000 $ 170,000 Repairs 35,000 Insurance 130,000 Life Insurance Premiums on Officers 18,000 Guaranteed payment (Banner) 400,000 Other salaries 1,000,000 Travel 45,000 Utilities 115,000 Rent Expense 75,000 Advertising Legal fees 25,000 350,000 Accounting fees 250,000 Charitable contributions 225,000 Payroll taxes 75,000 Business interest expense 20,000 Investment Expenses 12,000 Investment Interest Expense 5,000 Business Meals 20,000 Total expenses $ (2,970,000) Interest on municipal bonds 15,000 Net gain on stock sales 260,000 Dividend income Net income Required: 30,000 $ 635,000 1.) Prepare the 2022 partnership tax return, include the additional schedules and forms as needed. Be sure to prepare a Schedule K-1 for each partner. Print these documents to pdf (instructions below) and upload to the Partnership Tax Return assignment on D2L. 2.) Prepare a schedule for each partner's basis in his or her partnership interest as of December 31, 2021. On January 1, 2022 Banner's basis was $2,277,000 and Parker's was $5,313,000. Print these documents to pdf (instructions below) and upload to the Partnership Tax Return assignment on D2L. Print to pdf and upload the documents prepared in requirements 1 and 2 by the due date. Wayne Company is located at 99 Fifth Avenue New York City, NY, 10001. The company is a general partnership using the calendar year and accrual basis for both book and tax purposes. It engages in the development and sale of specialized self-protection armor. The employer identification number (EIN) is 01-2345678. The company was formed and began business on January 1, 2020. It does not have foreign partners or other foreign dealings. The company is neither a tax shelter or a publicly traded partnership. The company has made no distribution other than cash and no changes in ownership have occurred during the current year. Diana Banner is the Tax Matters Partner. The partnership makes no special elections. Information on Partnership Formation: Two individuals formed the partnership on January 1, 2020: Diana Banner (2500 Island Way, New York City, NY, 10001) and Bruce Parker (890 Arachnid Drive, New York City, NY, 10001). For a 30% interest, Diana contributed $900,000 cash. She is an active general partner who manages the company. For a 70% interest, Parker contributed $1.6 million cash and 1,000 shares of Metro Corporation stock having a FMV of $500,000 at the time of contribution and a basis of $100,000 when originally acquired on January 2, 2016. Parker is an active general partner who designs and develops new products. For book purposes, the company recorded the contribution of stock at FMV. Inventory and COGS: The company uses the periodic inventory method and prices its inventory using the lower of cost or market. Only beginning inventory, ending inventory, and purchases should be reflected in Schedule A. No other costs or expenses are allocated to cost of goods sold. The corporation is exempt from the uniform capitalization (UNICAP) rules because average gross income for the previous three years was less than $10 million. The following information should also be included on the applicable form: Line 9 (a) (b), (c), & (d) (e) & (f) Check (ii) Not applicable No Capital Gains and Losses: The company sold all 1,000 shares of Metro Corporation stock on July 2, 2022 for $760,000. The transaction was not reported on Form 1099-B. Fixed Assets and Depreciation: Fixed Asset Listing: Asset Equipment 1 Placed in Service Date Cost 1/1/2020 300,000 Equipment 2 1/1/2020 100,000 Equipment 3 1/1/2020 125,000 Equipment 4 1/1/2020 115,000 Equipment 5 1/1/2020 200,000 Equipment 6 1/1/2020 185,000 Equipment 7 1/1/2020 105,000 Equipment 8 1/1/2021 50,000 Equipment 9 1/1/2021 65,000 Equipment 10 6/11/2022 Building 1 1/1/2020 Warehouse 1 1/1/2020 75,000 1,000,000 900,000 Book Depreciation: The corporation uses straight-line deprecation over the useful lives of the assets as follows: • Building: 50 years; • Equipment: ten years; The corporation takes a half-year's depreciation in the year of acquisition and the year of disposition and assumes no salvage value. The book financial statements reflect these calculations. Tax Depreciation: All assets are MACRS property as follows: • Building: 39-year non-residential real property. Equipment: seven-year property. The corporation also uses the half-year convention for tax purposes. The corporation did not make the expensing election under Sec. 179 or take bonus depreciation on any property acquired before 2022. Accumulated depreciation through December 31, 2021 on the properties is as follows: Asset Accumulated Depreciation Building 1 50,250 Warehouse 1 45,225 Equipment 1 116,340 Equipment 2 38,780 Equipment 3 48,475 Equipment 4 44,597 Equipment 5 77,560 Equipment 6 71,743 Equipment 7 40,719 Equipment 8 1,231 Equipment 9 1,600 Equipment 10 On June 11, 2022, the company acquired and placed in service equipment (Equipment 10) costing $75,000. The company made the Sec. 179 expensing election for the entire cost of this new equipment. No depreciation or expensing is reported on Schedule A. You may use published IRS depreciation tables to compute the 2022 depreciation or the tax software. Other information: • The company paid Banner a $400,000 guaranteed payment for her management services. • • The company made a $225,000 cash contribution to the Boys & Girls Club on December 1, 2022. During the current year, the company made a $180,000 cash distribution to Banner and a $420,000 cash distribution to Parker. • The municipal bonds, acquired in 2020, are general revenue bonds, not private-equity bonds. Assume that no expenses of the company are allocable to the tax-exempt interest generated from the municipal bonds. • Use book numbers for Schedule L, M-2, and Line 1 of Schedule M-1. Also use book numbers for Item L of Schedule K-1 and check the box for Sec. 704(b) book. · The partners share liabilities, which are recourse, in the same proportion as their ownership %'s. The balance sheet is as follows: January 1, 2022 December 31, 2022 Cash $ 207,250 $ 805,250 Accounts Receivable 320,000 Inventory 2,600,000 Investment in municpal bonds 50,000 335,000 2,500,000 50,000 Investment in corporate stock 1,500,000 1,000,000 Buildings 1,900,000 1,900,000 Accum. Depreciation - Buildings 57,000 95,000 Equipment 1,245,000 1,320,000 Accum. Depreciation - Equipment 175,250 307,250 Accounts payable 250,000 240,000 Notes payable (short-term) 315,000 305,000 Notes payable (long-term) 1,000,000 900,000 Accrued payroll taxes 25,000 28,000 Capital account balances: Diana Banner (30%) 1,800,000 1,810,500 Bruce Parker (70%) 4,200,000 4,224,500 The book income statement is as follows: Sales Less: Returns Net sales Beginning inventory Purchases Ending Inventory Cost of goods sold Gross profit Expenses: Depreciation $ $ 2,600,000 3,000,000 (2,500,000) $ 7,000,000 (600,000) 6,400,000 $ (3,100,000) $ 3,300,000 $ 170,000 Repairs 35,000 Insurance 130,000 Life Insurance Premiums on Officers 18,000 Guaranteed payment (Banner) 400,000 Other salaries 1,000,000 Travel 45,000 Utilities 115,000 Rent Expense 75,000 Advertising Legal fees 25,000 350,000 Accounting fees 250,000 Charitable contributions 225,000 Payroll taxes 75,000 Business interest expense 20,000 Investment Expenses 12,000 Investment Interest Expense 5,000 Business Meals 20,000 Total expenses $ (2,970,000) Interest on municipal bonds 15,000 Net gain on stock sales 260,000 Dividend income Net income Required: 30,000 $ 635,000 1.) Prepare the 2022 partnership tax return, include the additional schedules and forms as needed. Be sure to prepare a Schedule K-1 for each partner. Print these documents to pdf (instructions below) and upload to the Partnership Tax Return assignment on D2L. 2.) Prepare a schedule for each partner's basis in his or her partnership interest as of December 31, 2021. On January 1, 2022 Banner's basis was $2,277,000 and Parker's was $5,313,000. Print these documents to pdf (instructions below) and upload to the Partnership Tax Return assignment on D2L. Print to pdf and upload the documents prepared in requirements 1 and 2 by the due date.

Expert Answer:

Answer rating: 100% (QA)

Certainly Were tasked with preparing the partnership tax return for Wayne Company for the tax year 2... View the full answer

Related Book For

Federal Taxation 2021 Corporations, Partnerships, Estates & Trusts

ISBN: 9780135919460

34th Edition

Authors: Timothy J. Rupert, Kenneth E. Anderson, David S. Hulse

Posted Date:

Students also viewed these accounting questions

-

Health wise Medical Supplies Company is located at 2400 Second Street, City, ST 12345. The company is a general partnership that uses the calendar year and accrual basis for both book and tax...

-

Healthwise Medical Supplies Company is located at 2400 Second Street, City, ST 12345. The company is a general partnership that uses the calendar year and accrual basis for both book and tax...

-

Graph the sets of points whose polar coordinates satisfy the equations and inequalitie. = 2/3, r -2

-

Under normal conditions, humans radiate electromagnetic waves with a wavelength of about 9.0 microns. (a) What is the frequency of these waves? (b) To what portion of the electromagnetic spectrum do...

-

Calculate the net present value (NPV) for the following 15-year projects. Comment on the acceptability of each. Assume that the firm has a cost of capital of 9%. a. Initial investment is $1,000,000;...

-

Referring to Exercise 12.3, use Bonferroni simultaneous confidence intervals with \(\alpha=0.06\) to compare the mean number of electrodes coated by the experiment under the 3 different alternatives....

-

You are a financial analyst for Damon Electronics Company. The director of capital budgeting has asked you to analyze two proposed capital investments, Projects X and Y. Each project has a cost of...

-

KneeFix is a medical device manufactured by KneeKing Pty Ltd. KneeFix was designed to be inserted into the knee joint during knee replacement surgery. KneeFix was sold and used in Australia for a...

-

The Harriet Hotel in downtown Boston has 100 rooms that rent for $150 per night. It costs the hotel $30 per room in variable costs (cleaning, bathroom items, etc.) each night a room is occupied. For...

-

write a paper that discusses how you would effectively manage a team. Be sure to consider the following questions in your paper. How will you select your team members? Describe the methods you will...

-

Harlow has been saving for seven months and has $477.75 saved for accommodations, which is 35% of her total vacation savings. Determine what percent of Harlow's $1,950.00 monthly retirement income...

-

Susan and Tom Houser believe that they will need payments of $4,460 at the beginning of each of their retirement. The payments will be made out of an account that is expected to earn 10% interest...

-

Exhibit 19B.1 Present Value of $1* Periods 2% 4% 6% 8% 10% 12% 14% 16% 18% 20% 22% 24% 26% 28% 30% 32% 40% 1 0.980 0.962 0.943 2 0.961 0.925 0.890 3 0.942 0.889 0.840 0.926 0.857 0.794 4 0.924 0.855...

-

Balance Sheet December 30, 2022 Current assets Cash $26.000 Accounts receivable 35,200 Prepaid insurance 6,000 $ 67,200 Equipment (net) 201,000 Total assets $268,200 Current liabilities Accounts...

-

If Agile teams are self-organizing and autonomous, why is there a daily scrum? 2. How can software development terms such as continuous integration and pair programming be applied to non-software...

-

Why are semiconductor quantum dots not very good for classical microelectronic applications? Give at least two reasons.

-

Refrigerant R-12 at 30C, 0.75 MPa enters a steady flow device and exits at 30C, 100 kPa. Assume the process is isothermal and reversible. Find the change in availability of the refrigerant.

-

Giovanni died in 2020 with a gross estate of $13.9 million and debts of $30,000. He made post-1976 taxable gifts of $100,000, valued at $80,000 when Giovanni died. His estate paid state death taxes...

-

Bioteknic Corporation announced that it had entered into a merger agreement with Zalco Corporation, a research-based pharmaceutical company and a leader in drug delivery technologies. In a nontaxable...

-

Under a divorce agreement executed in 2017, an ex-wife receives from her former husband cash of $25,000 per year for eight years. The agreement does not explicitly state that the payments are...

-

What does the Richter scale measure?

-

Where do earthquakes occur?

-

Why do earthquakes produce seismic waves?

Study smarter with the SolutionInn App