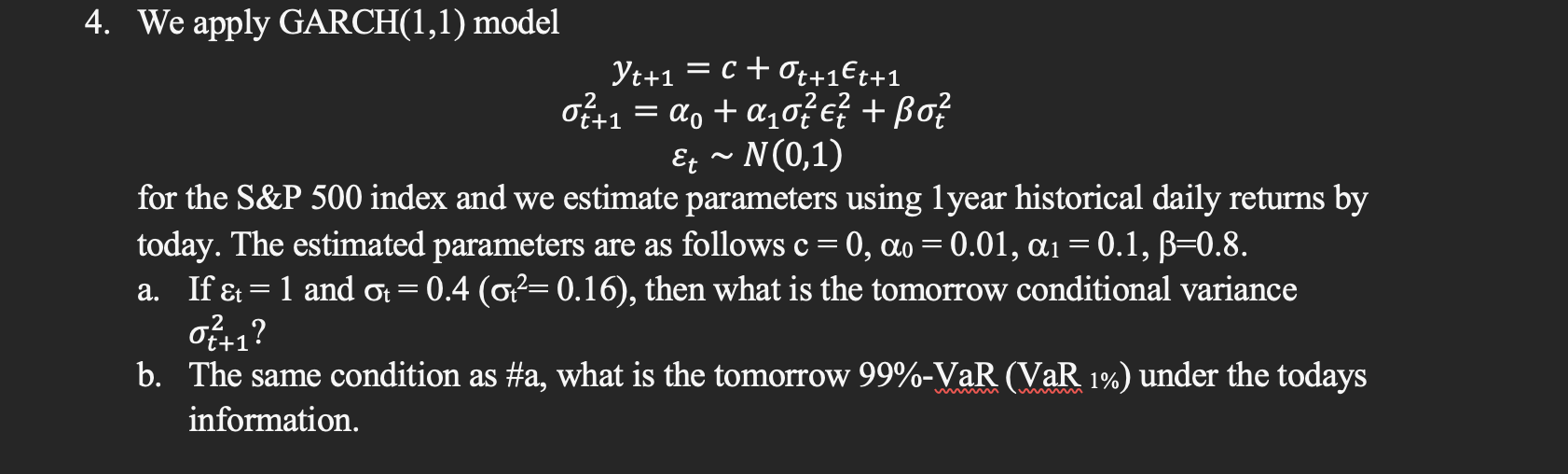

Question: We apply GARCH ( 1 , 1 ) model y t + 1 = c + t + 1 l o n t + 1

We apply GARCH model

for the S&P index and we estimate parameters using year historical daily returns by

today. The estimated parameters are as follows

a If and then what is the tomorrow conditional variance

b The same condition as # a what is the tomorrow VaR under the todays

information.

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock