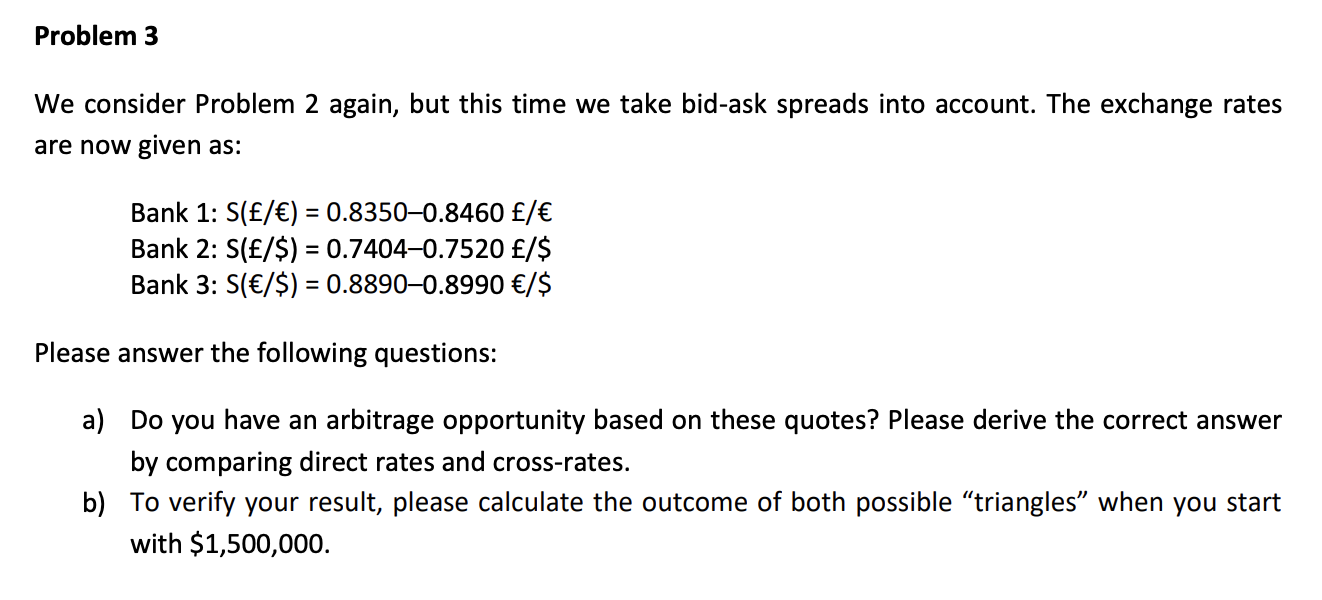

Question: We consider Problem 2 again, but this time we take bid-ask spreads into account. The exchange rates are now given as: Bank 1: S(/)=0.83500.8460/ Bank

We consider Problem 2 again, but this time we take bid-ask spreads into account. The exchange rates are now given as: Bank 1: S(/)=0.83500.8460/ Bank 2: S(/$)=0.74040.7520f/$ Bank 3: S(/$)=0.88900.8990/$ Please answer the following questions: a) Do you have an arbitrage opportunity based on these quotes? Please derive the correct answer by comparing direct rates and cross-rates. b) To verify your result, please calculate the outcome of both possible "triangles" when you start with $1,500,000. We consider Problem 2 again, but this time we take bid-ask spreads into account. The exchange rates are now given as: Bank 1: S(/)=0.83500.8460/ Bank 2: S(/$)=0.74040.7520f/$ Bank 3: S(/$)=0.88900.8990/$ Please answer the following questions: a) Do you have an arbitrage opportunity based on these quotes? Please derive the correct answer by comparing direct rates and cross-rates. b) To verify your result, please calculate the outcome of both possible "triangles" when you start with $1,500,000

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts