Question: We have discussed binomial option pricing model for a call option expiring in one year. How will you expand this model to price options expiring

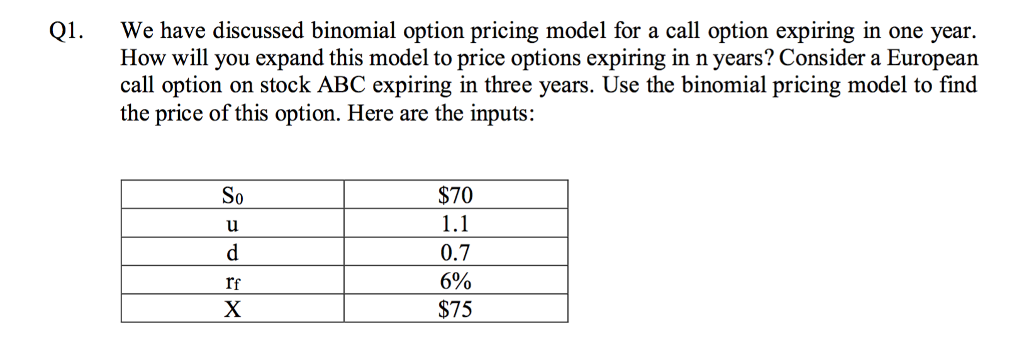

We have discussed binomial option pricing model for a call option expiring in one year. How will you expand this model to price options expiring in n years? Consider a European call option on stock ABC expiring in three years. Use the binomial pricing model to find the price of this option. Here are the inputs: Q1. $70 1.1 0.7 6% $75 003 rf

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock