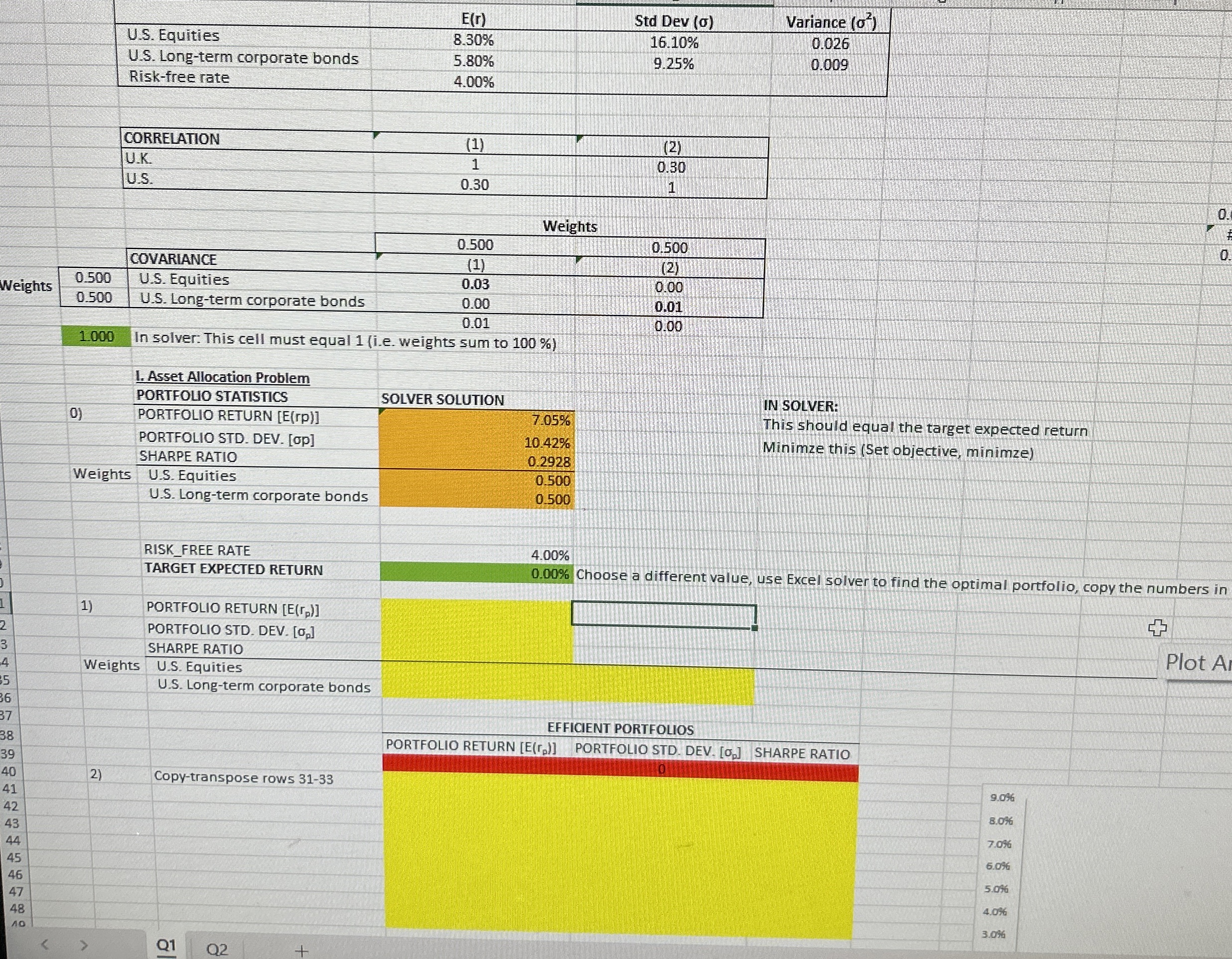

Question: Weights 1 . 0 0 0 In solver: This cell must equal 1 ( i . e . weights sum to 1 0 0 %

Weights

In solver: This cell must equal ie weights sum to

I. Asset Allocation Problem

PORTFOLIO STATISTICS

SOLVER SOLUTION

IN SOLVER:

This should equal the target expected return

Minimze this Set objective, minimze

RISKFREE RATE

TARGET EXPECTED RETURN

Weights

P

Weights

US Equities

US Longterm corporate bonds

PORTFOLIO RETURN E :

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock