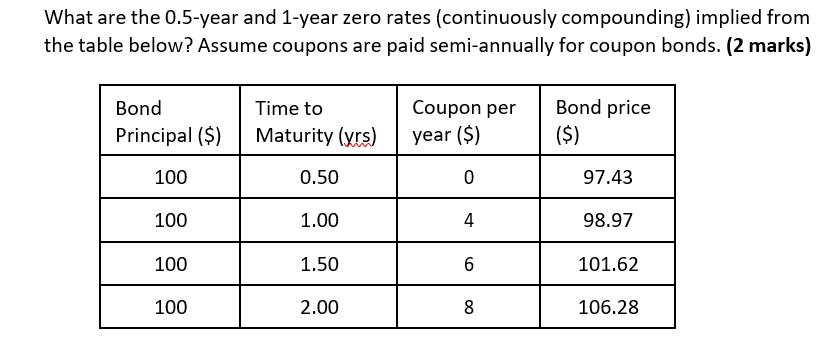

Question: What are the 0.5-year and 1-year zero rates (continuously compounding) implied from the table below? Assume coupons are paid semi-annually for coupon bonds. (2

What are the 0.5-year and 1-year zero rates (continuously compounding) implied from the table below? Assume coupons are paid semi-annually for coupon bonds. (2 marks) Bond Principal ($) 100 100 100 100 Time to Maturity (yrs) 0.50 1.00 1.50 2.00 Coupon per year ($) 0 4 6 8 Bond price ($) 97.43 98.97 101.62 106.28

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

To calculate the zero rates from the given bond prices we can use the formula ... View full answer

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock