Question: What are the formulas needed to solve this problem? (the dotted a) and the (Ia) with the lines. Are these functions on a financial calculator?

What are the formulas needed to solve this problem? (the dotted a) and the (Ia) with the lines. Are these functions on a financial calculator?

Can you please write out the shortcut completely? thank you.

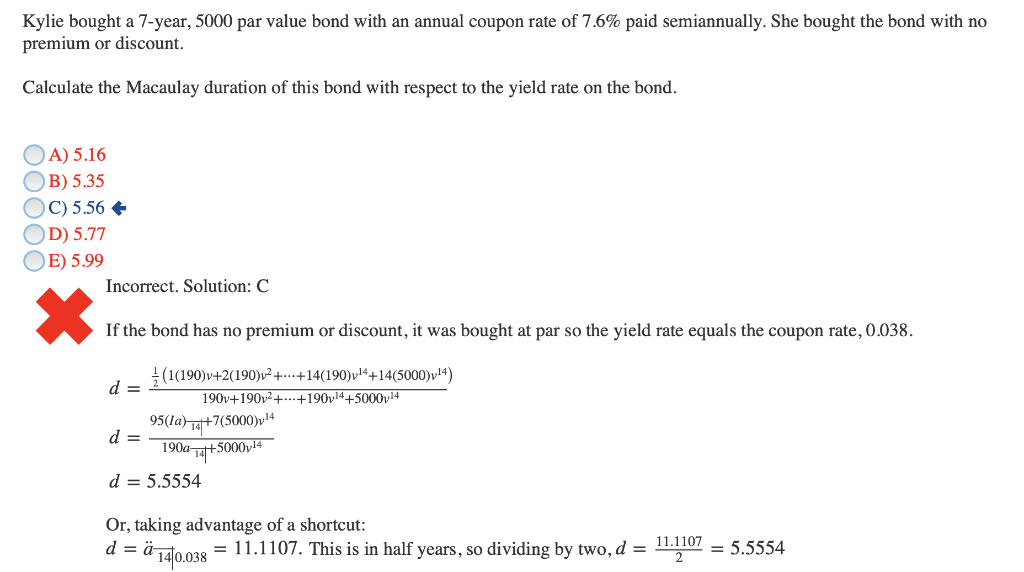

Kylie bought a 7-year, 5000 par value bond with an annual coupon rate of 7.6% paid semiannually. She bought the bond with no premium or discount. Calculate the Macaulay duration of this bond with respect to the yield rate on the bond. A) 5.16 B) 5.35 C) 5.56 + D) 5.77 E) 5.99 Incorrect. Solution: C If the bond has no premium or discount, it was bought at par so the yield rate equals the coupon rate, 0.038. (1(190)v+2(190)+...+14(190)4+14(5000)4) d = 190v+190v+ +190v4+50004 95(la) 14+7(5000)v4 d = 190a-14+5000v4 d = 5.5554 Or, taking advantage of a shortcut: d = 14/0.038 11.1107 = 11.1107. This is in half years, so dividing by two, d = = 5.5554

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts