Question: What is the expected return and the variance for a portfolio that invests 57% in the stock fund and 43% in the money market fund?

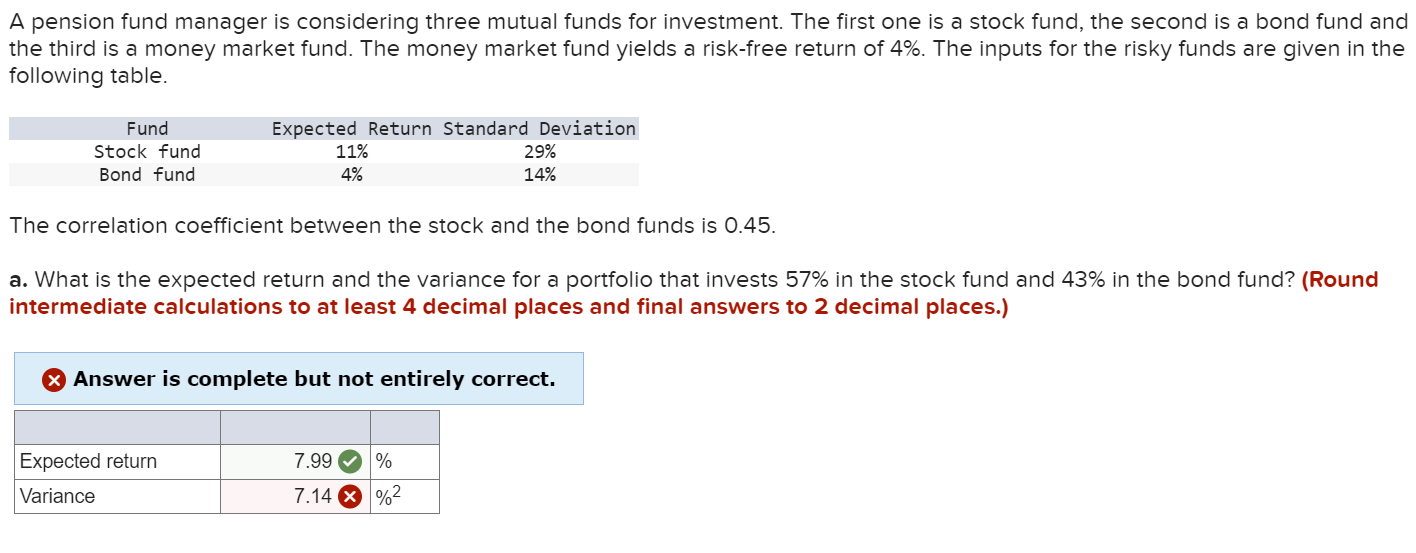

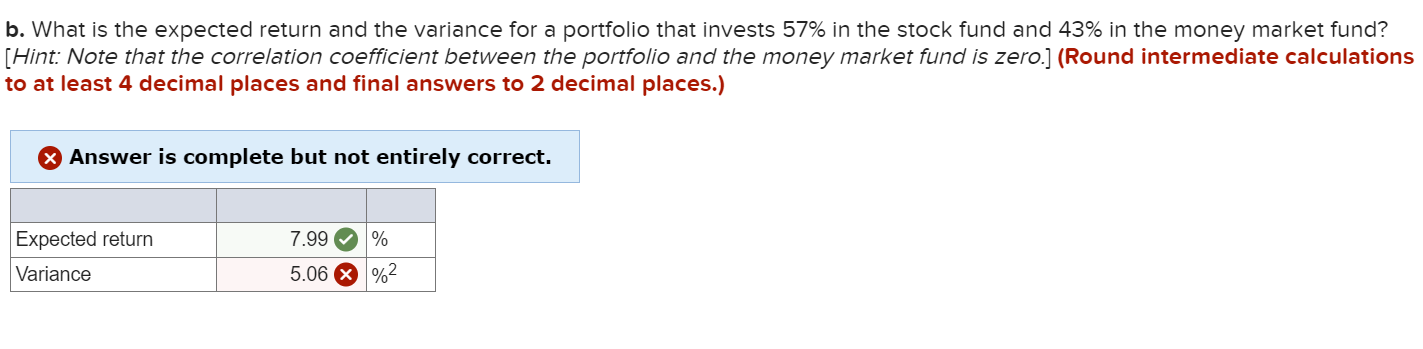

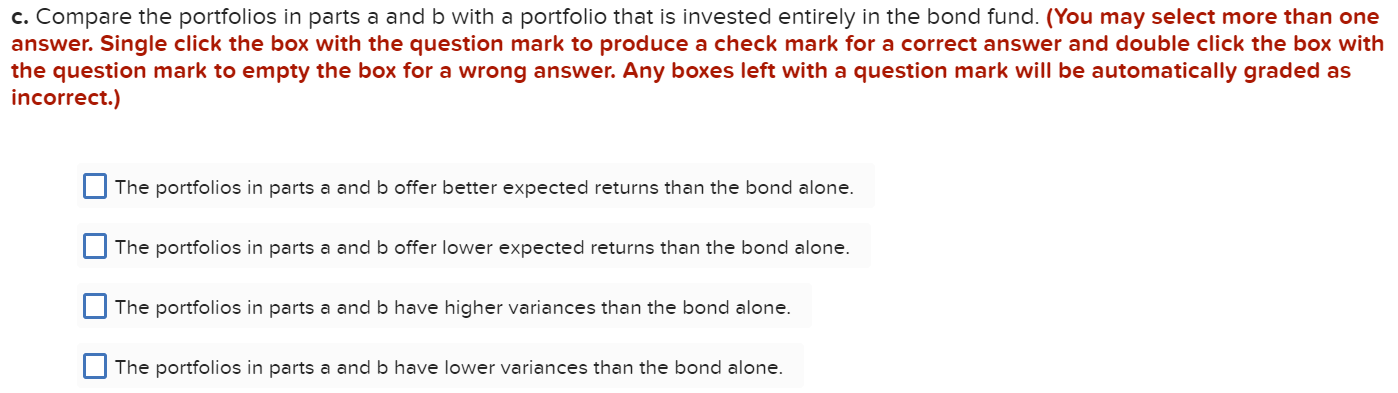

What is the expected return and the variance for a portfolio that invests 57% in the stock fund and 43% in the money market fund? Hint: Note that the correlation coefficient between the portfolio and the money market fund is zero.] (Round intermediate calculations 0 at least 4 decimal places and final answers to 2 decimal places.) Answer is complete but not entirely correct. c. Compare the portfolios in parts a and b with a portfolio that is invested entirely in the bond fund. (You may select more than one answer. Single click the box with the question mark to produce a check mark for a correct answer and double click the box with the question mark to empty the box for a wrong answer. Any boxes left with a question mark will be automatically graded as incorrect.) The portfolios in parts a and b offer better expected returns than the bond alone. The portfolios in parts a and b offer lower expected returns than the bond alone. The portfolios in parts a and b have higher variances than the bond alone. The portfolios in parts a and b have lower variances than the bond alone. A pension fund manager is considering three mutual funds for investment. The first one is a stock fund, the second is a bond fund and the third is a money market fund. The money market fund yields a risk-free return of 4%. The inputs for the risky funds are given in the following table. The correlation coefficient between the stock and the bond funds is 0.45 . a. What is the expected return and the variance for a portfolio that invests 57% in the stock fund and 43% in the bond fund? (Round intermediate calculations to at least 4 decimal places and final answers to 2 decimal places.) Answer is complete but not entirely correct

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts